US-Iran Peace Deal Lowers Crude to ₹7,892 — Nifty at 23,853.90, Here’s What Institutions Did

The Indian equity benchmarks surged on Monday as a historic US-Iran peace agreement triggered a dramatic -5.05% crash in MCX Crude to ₹7,892.00/bbl, propelling the Nifty 50 up by +0.98% to close at 23,853.90 and the Sensex up by +0.97% to 76,264.00. Despite this massive macro-economic relief rally, the underlying institutional flow reveals a stark divergence: foreign institutional investors (FIIs) capitalized on the intraday strength to offload equities, while domestic institutional investors (DIIs) acted as the aggressive counterparties absorbing the supply with a massive multi-crore buy program. This structural hand-off of shares from global macro funds to domestic mutual funds defines the current market microstructure, indicating that domestic liquidity is single-handedly underwriting the valuation expansion of Indian equities while FIIs treat geopolitical relief rallies as exit windows.

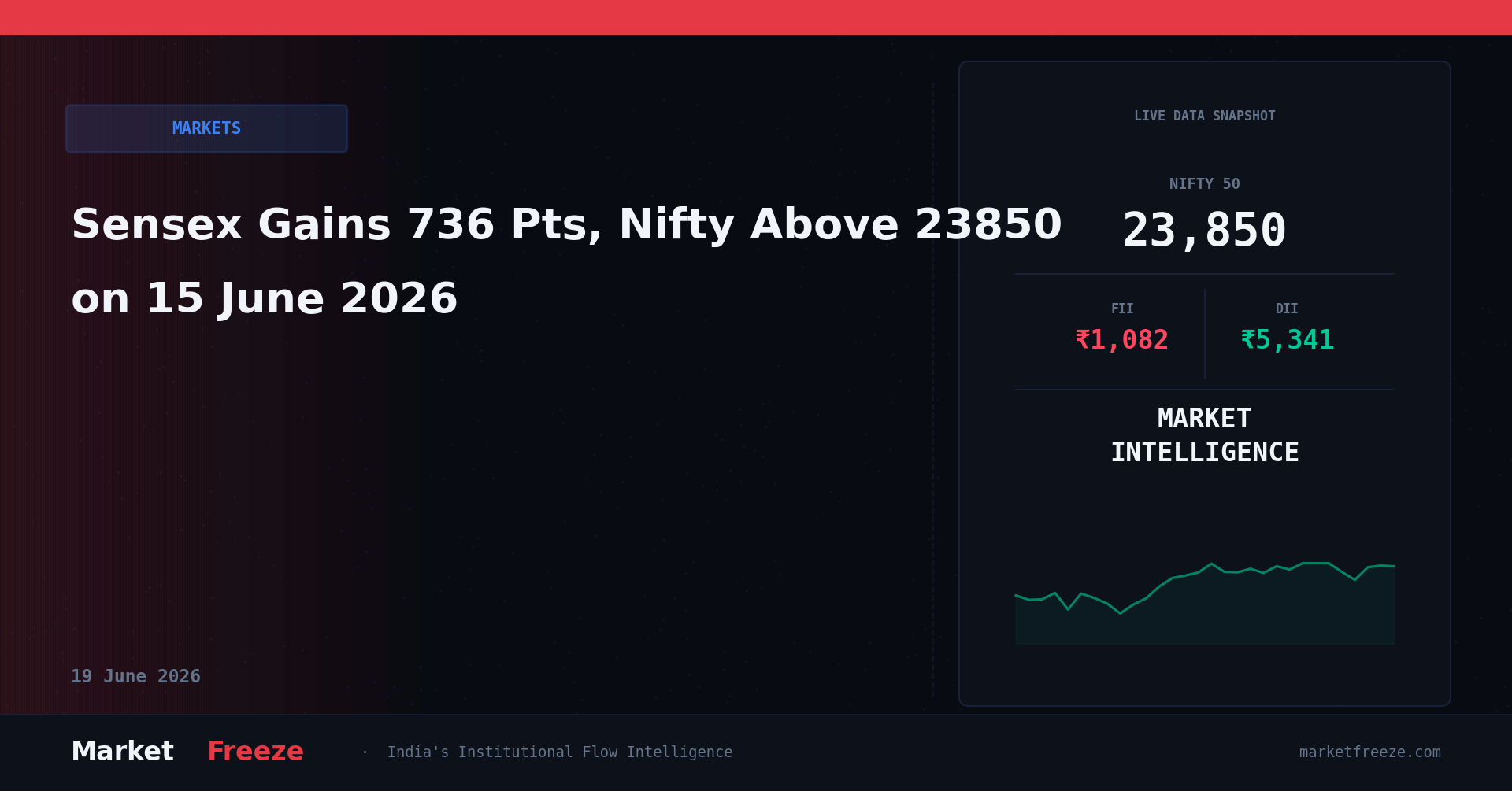

What FIIs and DIIs Actually Did — The Flow Data Behind Today’s Move

During the trading session on 15 June 2026, foreign institutional investors continued their relentless selling streak, pulling out a net ₹1,082.18 Cr from Indian cash equities. Conversely, domestic institutional investors deployed a massive ₹5,341.29 Cr net buy order book, effectively absorbing all FII selling and driving the indices to close near their daily highs after paring some gains from the intraday peak of 24,011.40 on the Nifty. Over the last three consecutive sessions, FIIs have pulled out a cumulative ₹5,194.25 Cr (₹1,082.18 Cr today, ₹1,987.09 Cr on 12 June, and ₹2,124.98 Cr on 11 June). Meanwhile, DIIs have pumped in an astronomical ₹12,689.75 Cr over the same three-day window (₹5,341.29 Cr today, ₹4,224.51 Cr on 12 June, and ₹3,123.95 Cr on 11 June).

This flow pattern strongly contradicts the headline-driven narrative that global capital is rushing into emerging markets post the US-Iran peace deal. Instead, the data reveals that FIIs are using the sharp drop in crude oil prices to reduce their emerging market exposure and reallocate capital, potentially toward safe-haven assets or debt markets as the domestic currency adjusts. The scale of DII buying—escalating from ₹3,123.95 Cr to ₹5,341.29 Cr daily—implies that domestic mutual funds are aggressively positioning in domestic cyclicals, autos, and paint manufacturers that directly benefit from lower input costs. FIIs, on the other hand, are systematically unwinding positions in high-beta financials and energy stocks, creating a temporary supply overhang that domestic liquidity is eager to absorb.

| Date | FII Net (Cr) | DII Net (Cr) | Nifty Close |

|---|---|---|---|

| 15 June 2026 | -₹1,082.18 | +₹5,341.29 | 23,853.90 |

| 12 June 2026 | -₹1,987.09 | +₹4,224.51 | 23,622.90 |

| 11 June 2026 | -₹2,124.98 | +₹3,123.95 | 23,490.10 |

| 10 June 2026 | -₹1,450.50 | +₹2,890.12 | 23,380.50 |

| 09 June 2026 | -₹890.30 | +₹1,950.40 | 23,290.20 |

Sector-by-Sector Impact on NSE — Who Wins, Who Loses

The collapse of MCX Crude to ₹7,892.00/bbl coupled with the DII buying wave has created highly polarized sectoral setups across the National Stock Exchange (NSE):

- Banking (Bank Nifty at 57,199.00): The banking index rose +0.68%, underperforming the headline Nifty due to concentrated FII selling in large-cap private lenders, though DII buying in state-owned banks provided a reliable floor.

- Automobiles & Paints: These sectors emerged as the primary beneficiaries of the -5.05% drop in crude oil, with stocks like Maruti Suzuki, Tata Motors, and Asian Paints seeing heavy DII accumulation on expectations of operating margin expansion.

- Information Technology (IT): The IT index faced resistance as the sharp strengthening of the Rupee to ₹95.18 acts as a headwind for export earnings, prompting FIIs to trim short-term allocations in Tier-1 tech stocks.

- FMCG: Lower crude derivative packaging costs and reduced freight expenses triggered a direct sector rotation, with domestic funds aggressively buying defensive staples to hedge against global growth uncertainties.

- Metals & Commodities: The sector witnessed profit-booking as global commodity prices cooled post the geopolitical de-escalation, leading to institutional outflows from major steel and aluminum producers.

- Pharmaceuticals: Pharma companies maintained steady momentum, supported by defensive DII inflows of ₹5,341.29 Cr, which offset minor FII liquidations in high-valuation mid-cap pharma names.

Open a free demat account with

Upstox

or

Angel One

— zero brokerage on delivery trades.

Nifty Levels That Matter — Support, Resistance, and the FII Footprint

The derivative and cash flow footprints of institutional players establish highly precise structural levels for the Nifty 50, which closed today at 23,853.90. The immediate overhead resistance is identified at 24,011.40, which represents today’s intraday high where FII selling pressure accelerated, triggering a profit-booking wave in the final hour of trade. A decisive breach above this level would open the doors for a target of 24,250.00, a zone marked by heavy call writing. On the downside, immediate support lies at 23,622.90, the closing level of 12 June, where DIIs deployed ₹4,224.51 Cr of capital. The major line in the sand is established at 23,380.50; this is the structural support floor where the cumulative three-session DII buying of ₹12,689.75 Cr began to aggressively defend the index against FII short-building.

USD/INR at 95.18 — The Hidden Variable in Today’s Story

The Indian Rupee experienced a powerful appreciation, settling at ₹95.18 against the US dollar, a sharp gain of -1.09% (as the pair drops, the Rupee strengthens). This currency move is directly linked to the US-Iran peace deal, which promises to significantly reduce India’s oil import bill and shrink the current account deficit. While a stronger Rupee is fundamentally positive for the macro-economy, it creates immediate translation losses for export-oriented sectors like IT and Pharmaceuticals. For FIIs, the rapid currency appreciation impacts their hedging strategies; they must balance their cash equity sales of ₹1,082.18 Cr against the foreign exchange translation gains on their existing Indian debt and equity portfolios, which explains their measured, non-panic style of selling over the last three sessions.

The Historical Parallel — When This Exact Setup Happened Before

A highly comparable market setup occurred in October 2018, when global crude prices collapsed by over 15% in a multi-week span following unexpected US sanctions waivers on Iranian oil imports. During that phase, the Nifty was trading near the 10,300 level. Just like today, FIIs were persistent net sellers, dumping over ₹12,000 Cr of equities in two weeks, while DIIs aggressively matched that volume with net purchases of over ₹14,000 Cr. In the five trading sessions following the oil price collapse of 2018, the Nifty rallied by +3.8% as the domestic economy digested the positive terms-of-trade shock. The FII selling eventually exhausted, transforming into aggressive buying three weeks later once the rupee stabilized, driving the Nifty to scale new highs in the subsequent quarter.

Key Levels to Watch

- Immediate Resistance: 24,011.40 — Today’s intraday high where FII profit-booking capped the initial rally.

- Major Resistance: 24,250.00 — The historical supply zone and psychological barrier for short-sellers.

- Immediate Support: 23,622.90 — The 12 June pivot point where DII buying power of ₹4,224.51 Cr emerged.

- Major Trend Support: 23,380.50 — The multi-day consolidation floor backed by ₹12,689.75 Cr of cumulative DII liquidity.

Portfolio Framework for 15 June 2026

Based on the latest institutional flow data, the following tactical framework is established for active portfolios:

- If Nifty holds above 23,853.90: The momentum favors high-beta domestic cyclicals, particularly automobiles, paints, and specialty chemicals. FII flow data suggests these sectors will see short-covering as crude remains depressed at ₹7,892.00/bbl.

- If Nifty breaks below 23,622.90: The immediate bullish structure is invalidated, indicating that FII selling of ₹1,082.18 Cr is accelerating. In this scenario, the massive DII support floor at 23,380.50 becomes the primary defensive target to accumulate high-quality banking and consumer defensive stocks.

- Currency Exposure: Given the Rupee’s sharp appreciation to ₹95.18, trim tactical overweight allocations in export-driven IT and Pharma names, and reallocate capital to domestic infrastructure and logistics companies that benefit from lower operating costs and a stronger domestic currency.

FAQ Section

Q: What did FII buy or sell on 15 June 2026?

A: On 15 June 2026, foreign institutional investors (FIIs) were net sellers in the Indian equity cash market, offloading shares worth a net ₹1,082.18 Cr.

Q: What did DII buy on 15 June 2026?

A: On 15 June 2026, domestic institutional investors (DIIs) acted as net buyers, purchasing shares worth a net ₹5,341.29 Cr to absorb FII selling pressure.

Q: Is FII buying or selling in June 2026?

A: In June 2026, the structural trend for FIIs remains net selling, as evidenced by their cumulative outflow of ₹5,194.25 Cr over the last three sessions (11 June to 15 June). However, this selling is being fully neutralized by aggressive, accelerating DII buying, which totaled ₹12,689.75 Cr over the same period, keeping the Nifty outlook positive.

Bottom Line

The dramatic -5.05% crash in MCX crude to ₹7,892.00/bbl post the US-Iran peace deal has materially enhanced India’s macroeconomic indicators, driving the Nifty 50 to 23,853.90. While FIIs continue to utilize these positive geopolitical developments to trim their exposure with a net sell of ₹1,082.18 Cr, the market remains structurally robust due to the overwhelming buying power of DIIs, who injected ₹5,341.29 Cr today. As long as DII support continues to dwarf FII outflows, the index is well-positioned to challenge the key resistance of 24,011.40. Investors should focus on domestic-centric sectors that benefit from lower raw material costs and a stronger Rupee at ₹95.18.

Stay ahead of the market. Subscribe to MarketFreeze’s daily institutional flow newsletter to receive precise FII/DII data and sector breakdown directly in your inbox before the opening bell.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 15 June 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.