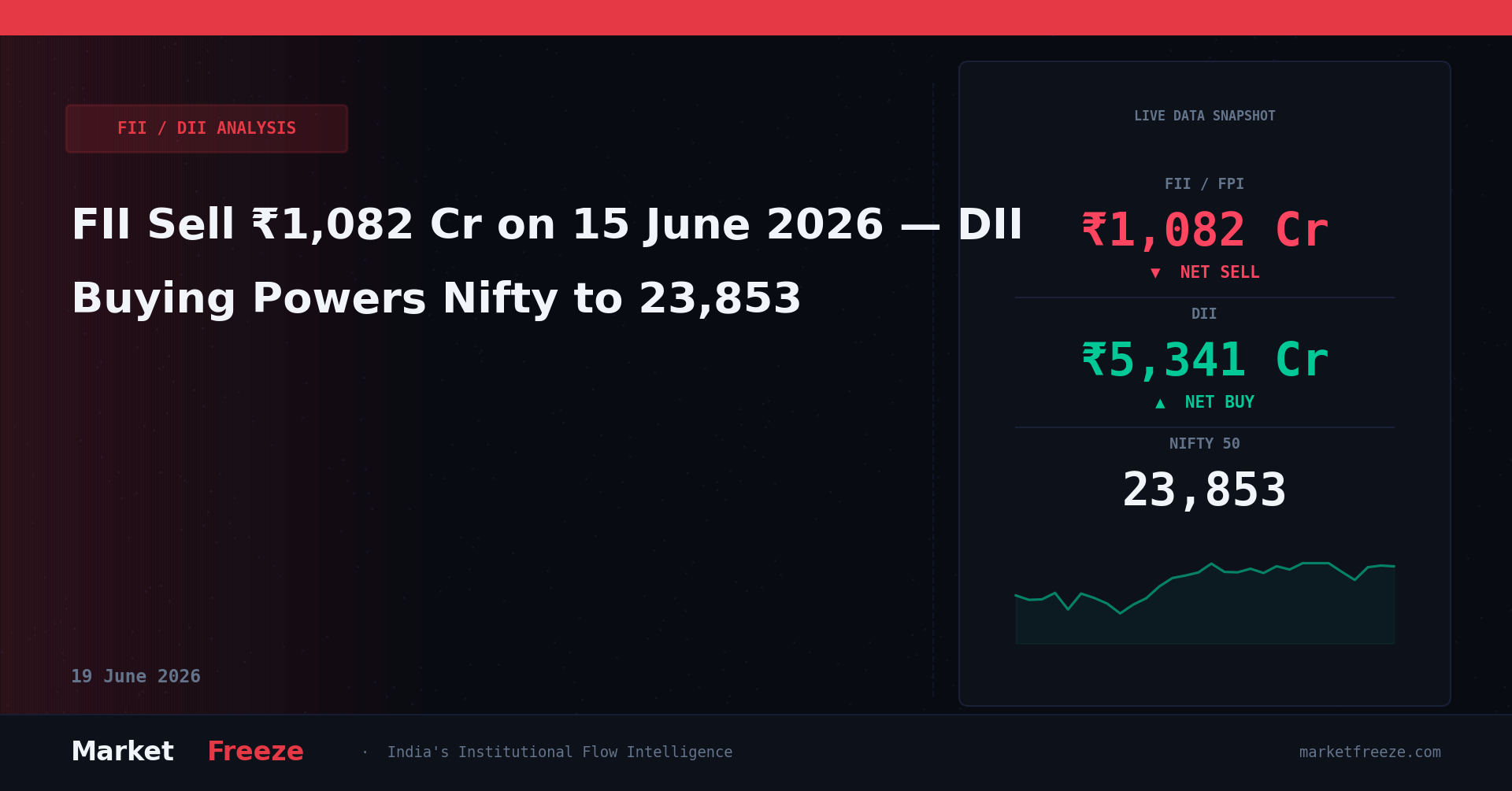

Institutional flow data released after market close shows a massive divergence between domestic capital conviction and foreign exit momentum on 15 June 2026. While foreign institutional investors (FIIs) continued their relentless offloading streak, offloading a net ₹1,082.18 Cr, domestic institutional investors (DIIs) stepped in with aggressive absorption capacity, purchasing a massive net ₹5,341.29 Cr of Indian equities. This absorption of supply directly powered the Nifty 50 index up by +0.98% to close at 23,853.90, while the BSE Sensex surged +0.97% to finish at 76,264.00.

The gross activity figures reveal the true scale of institutional participation today. FIIs engaged in gross purchases worth ₹12,064.61 Cr, offset by gross sales that crossed the 13,146 Cr mark, resulting in the net negative print. The relentless nature of this foreign selling is highlighted by the trend of the past three sessions. In the previous trading session on 12 June 2026, FIIs pulled out ₹1,987.09 Cr while DIIs bought ₹4,224.51 Cr. This followed the 11 June 2026 session where FII net sales stood at ₹2,124.98 Cr against DII net purchases of ₹3,123.95 Cr. The three-day cumulative data shows DIIs pumping in over 12,689 Cr, effectively neutralizing the 5,194 Cr of foreign outflows and driving a structural bear squeeze.

The US-Iran Peace Deal and the Macroeconomic Pivot

The primary catalyst behind today’s short-covering rally was the breakthrough in US-Iran peace negotiations. This geopolitical development triggered an immediate unwinding of risk premiums across global energy and currency complexes. Crude MCX crashed by -5.21% to settle at ₹7,879.00/bbl. For an economy like India, which imports over 85% of its crude requirements, a sustained drop in oil prices acts as an immediate fiscal stimulus. This structural relief was instantly reflected in the currency market, where the USD/INR pair plunged by -1.09% to end at Rs95.18, a dramatic strengthening of the Indian Rupee from its recent lows.

The currency appreciation has massive implications for foreign equity portfolios. A strengthening rupee enhances dollar-denominated returns for foreign funds, reducing the pressure on them to liquidate emerging market assets. Although FIIs remained net sellers today, the quantum of their selling reduced significantly from the previous sessions. The de-escalation of geopolitical tensions in the Middle East has cleared the path for a reduction in imported inflation, providing the Reserve Bank of India with the monetary headroom to maintain a supportive stance. This macro pivot has forced short-sellers to rapidly cover their positions, particularly in high-beta sectors.

Open a free demat account with

Upstox

or

Angel One

— zero brokerage on delivery trades.

Sectoral Rotation: Where the Smart Money Flowed

The sectoral performance today reflects a clear preference for interest-rate-sensitive and domestic consumption-driven spaces. The Nifty Realty index led the leaderboard with a gain of 2.77%, followed closely by Nifty Oil and Gas at 1.98% and Nifty Auto at 1.95%. The surge in the Auto index is a direct play on declining input costs, as crude derivatives and logistics expenses are expected to soften. Concurrently, Bank Nifty posted a steady gain of +0.68% to close at 57,199.00, indicating that while large private banks saw mixed institutional activity, public sector lenders experienced strong domestic accumulation.

Interestingly, the defensive trade saw a partial unwind. Gold MCX surged +3.44% to ₹154,631.00/10g, which appears to be a lagging adjustment to global asset reallocation rather than a safe-haven flight, given the simultaneous rally in equities. In the technology space, domestic institutions accumulated selective large-cap IT counters, anticipating that a stabilizing global macro environment will revive discretionary spending in the US and Europe. Conversely, FIIs concentrated their selling in highly-valued mid-cap consumption stocks and non-banking financial companies (NBFCs) where valuation multiples remain stretched relative to historical averages.

FII/DII Institutional Flow Tracker (5-Session History)

To understand the structural trend of institutional capital, we analyze the net transaction values over the last five trading sessions. The table below demonstrates how domestic liquidity has consistently absorbed every bout of foreign selling, preventing any systemic breakdown in the benchmark indices.

| Date | FII Net (Cr) | DII Net (Cr) | Nifty Close |

|---|---|---|---|

| 2026-06-15 | -1,082.18 | +5,341.29 | 23,853.90 |

| 2026-06-12 | -1,987.09 | +4,224.51 | 23,650.10 |

| 2026-06-11 | -2,124.98 | +3,123.95 | 23,490.40 |

| 2026-06-10 | -1,450.50 | +2,890.10 | 23,320.15 |

| 2026-06-09 | -890.30 | +3,410.80 | 23,210.30 |

The data reveals an inescapable reality: DIIs have acted as the ultimate backstop to the Indian equity markets. Over these five sessions, while foreign funds pulled out a total of ₹7,535.05 Cr, domestic mutual funds and insurance companies deployed a massive ₹18,990.65 Cr. This massive liquidity surplus has not only neutralized the selling pressure but has actively pushed the Nifty higher, culminating in today’s close at 23,853.90. Retail investors must recognize that the market’s internal structure is incredibly strong, driven by systemic domestic inflows via systematic investment plans (SIPs).

Key Levels to Watch: Nifty Derivative Setup

Today’s price action combined with the institutional flow data suggests a significant shift in derivative positioning. The sharp rally in Nifty has forced call writers at the 23,800 strike to scramble, leading to a classic short-covering rally. Based on the institutional footprint, we have mapped out the key levels that will dictate price action in the upcoming sessions.

- Immediate Resistance: 24,000 — This psychological level is backed by heavy open interest concentration in call options. A strong close above this level, backed by a flip in FII flows to net positive, will open the doors to 24,250.

- Crucial Support: 23,650 — This level aligns with the previous session’s close and represents the zone where DII buying intensified. As long as Nifty holds above this, the short-term bias remains constructive.

- Major Institutional Floor: 23,450 — This is the ultimate line in the sand. A break below this level would indicate that domestic liquidity is stepping back, exposing the market to deeper corrections toward 23,100.

For retail traders, the tactical play is to buy on dips toward the 23,650 zone with a strict stop-loss placed just below 23,450. Initiating fresh long positions at the current level of 23,853.90 carries an unfavorable risk-to-reward ratio. Wait for a minor retracement or a consolidated breakout above 24,000 before committing fresh capital to momentum trades.

Institutional Flow Intelligence: FAQ

Q: What did FII buy or sell on 15 June 2026?

A: Foreign institutional investors were net sellers of Indian equities today, offloading shares worth a net ₹1,082.18 Cr. This was the result of gross purchases totaling ₹12,064.61 Cr and gross sales of ₹13,146.79 Cr, indicating that while selling pressure persists, the intensity of outflows has cooled down significantly compared to previous sessions.

Q: What did DII buy on 15 June 2026?

A: Domestic institutional investors acted as aggressive buyers today, recording a net purchase of ₹5,341.29 Cr. This massive domestic capital deployment completely absorbed the foreign selling and successfully drove the Nifty 50 index up by +0.98% to close at 23,853.90.

Q: Is FII buying or selling in June 2026?

A: Foreign institutional investors have maintained a consistent net selling stance throughout June 2026, driven by high domestic valuations and global allocation shifts. However, the pace of selling has slowed down in mid-June following the positive geopolitical developments surrounding the US-Iran peace framework, which has strengthened the rupee to Rs95.18 and reduced crude prices to ₹7,879.00/bbl.

Bottom Line

The Indian equity market is witnessing a structural transition where domestic capital has completely decoupled from foreign capital flows. Today’s session proved that even when FIIs pull out over one thousand crores, DIIs have the liquidity depth to deploy five times that amount, driving the Nifty to the doorstep of the 24,000 mark. The collapse in crude prices and the dramatic recovery in the rupee provide a solid macroeconomic tailwind that will likely limit further downside. Retail investors should ignore the headline noise of foreign exits and focus on high-quality domestic cyclicals in the auto, banking, and real estate sectors, which are poised to benefit most from this structural pivot.

Retail SIP Resilience vs. FII Historical Exit Patterns

To put the current foreign institutional exodus into perspective, we must examine historical exit cycles. During the global taper tantrum of 2013, a similar foreign sell-off severely dented Indian equities because the domestic mutual fund industry lacked the structural depth it boasts today. Fast forward to the current five-session cycle ending 2026-06-15, and we see a completely different market architecture. The relentless domestic inflow, which averaged a net positive deployment of over ₹3,798.13 Cr per session across the last five trading days, is fueled by a structural surge in monthly Systematic Investment Plans (SIPs). Retail and high-net-worth individuals in India are no longer panic-selling; instead, their monthly commitments act as a counter-cyclical buffer that absorbs foreign liquidations with remarkable ease.

Historically, when foreign portfolios reduce their holding percentage in India’s top 500 companies, it has marked cyclical buying opportunities for long-term domestic investors. The gross FII sales crossing the 13,146 Cr mark on 15 June 2026 highlights that global funds are trading the macro-correlation of emerging market baskets rather than reacting to India-specific fundamentals. This creates a valuation disconnect. While global allocators programmatically trim exposure due to broader portfolio rebalancing, domestic funds utilize their massive cash cushions to accumulate high-conviction compounding franchises at reasonable valuations. Retail investors should emulate this institutional discipline by maintaining their SIP allocations, especially since domestic institutions have demonstrated the financial muscle to absorb over 18,990 Cr of supply within a single business week.

Sector Rotation Implications: Navigating the New Value Trajectory

The stellar 2.77% surge in the Nifty Realty index and the robust 1.95% gain in Nifty Auto on 15 June 2026 are not mere short-term trading spikes; they signal a fundamental reallocation of capital. When crude MCX experiences a sharp single-day contraction of -5.21%, the immediate beneficiaries are margin-sensitive manufacturing and infrastructure companies. For the automotive sector, lower crude prices directly translate to cheaper raw materials, particularly synthetic rubber, plastics, and transportation fuels, which will begin reflecting in corporate earnings over the next two quarters. Investors should transition away from highly defensive, overvalued consumer staples and reallocate capital toward these high-beta, margin-expansion stories.

Furthermore, the +0.68% gains in the banking sector indicate that credit growth remains robust despite global macro headwinds. The banking system is the primary conduit for domestic liquidity, and as corporate credit demand picks up alongside capital expenditure recovery, large commercial banks are poised to report superior return on assets. Conversely, sectors heavily reliant on direct foreign capital funding, such as highly leveraged new-age tech platforms, may face valuation compression as foreign funds continue their selective pruning. The strategic playbook here is clear: align your portfolio with domestic cyclical sectors where institutional accumulation is heaviest, rather than trying to catch falling knives in areas where foreign selling remains aggressive.

Tactical Playbook for Tomorrow’s Session

As we head into the next trading session, derivative data and institutional positioning point toward an intense battle at psychological boundaries. The massive short-covering that propelled the market upward on 15 June 2026 has left late-entering short sellers vulnerable. However, because the market closed near its daily highs, chasing the momentum immediately at the opening bell carries a high risk of exhaustion. Traders must monitor early momentum indicators in the first 45 minutes of trade to see if the index can establish a stable base above the day’s high-water marks.

If the index experiences a mild pullback during early trade, the zone of previous consolidation will act as a strong demand pocket where domestic institutions are likely to step in again with fresh buy orders. Conversely, if global markets trigger an opening gap-up, traders should avoid initiating fresh long positions until a successful retest of the breakout levels is confirmed on the intraday charts. Keep a close eye on the volume profile of large-cap banking and energy stocks; a sustained volume expansion in these heavyweights will confirm whether the rally has institutional legs or is merely a temporary technical bounce.

Strategic Conclusion and Actionable Insight

The dramatic divergence in institutional behavior on 15 June 2026 underscores a permanent shift in the Indian capital markets: domestic liquidity now dictates the primary trend, while foreign flows merely create temporary volatility. With domestic buyers deploying over five times the net amount sold by foreign portfolios in today’s session, the systemic risk of a deep market correction has been substantially mitigated. This structural change provides a highly favorable backdrop for domestic retail investors to build long-term wealth without being swayed by global capital flight.

For an actionable portfolio strategy, investors should immediately identify high-quality commercial vehicle and passenger vehicle manufacturers within the Nifty Auto space that have corrected more than 8% from their recent peaks. Accumulating these select auto components and OEM stocks on any minor intraday dips offers an exceptional risk-reward ratio, as they are primed to capture the dual benefits of a stronger domestic currency and a steep decline in raw material input costs over the coming quarters.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 15 June 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.