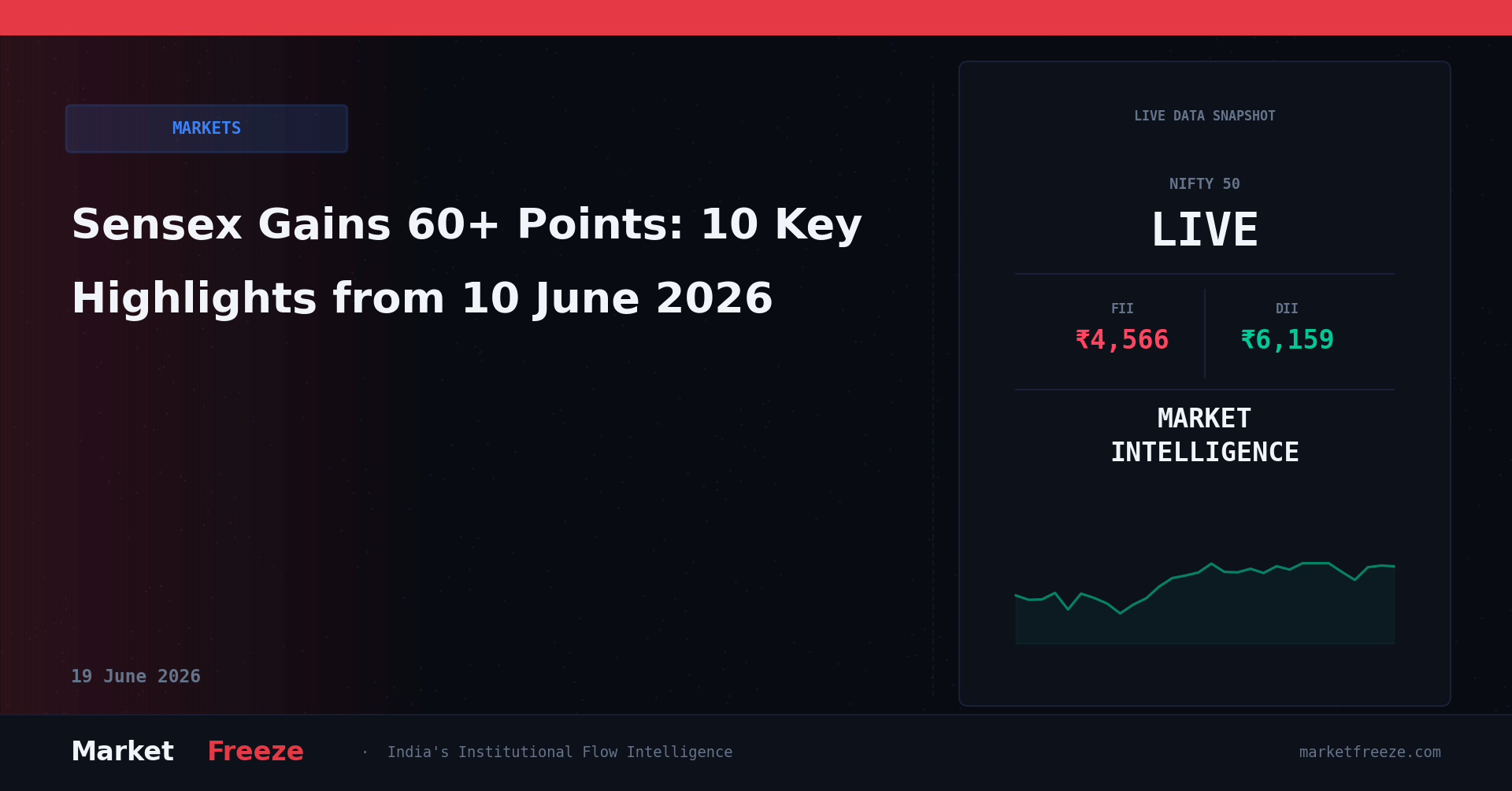

As geopolitical tensions escalated, the Indian benchmarks closed mixed on 10 June 2026, with the Nifty 50 settling at 23,214.95 (+0.40%) and the Sensex at 73,983.00 (+0.62%), while FIIs continued their significant selling spree, offloading ₹4,566.03 Cr net, directly counteracted by DIIs who absorbed ₹6,159.48 Cr net, indicating a persistent domestic institutional bid beneath the surface of global headwinds.

What FIIs and DIIs Actually Did — The Flow Data Behind Today’s Move

Today, 10 June 2026, FIIs were net sellers for the third consecutive session, offloading a substantial ₹4,566.03 Cr from the Indian equity markets. This figure, while significant, represents a slight moderation from yesterday’s ₹5,555.67 Cr net sell and Monday’s even higher ₹8,776.25 Cr net sell. Over the last three trading sessions, FIIs have cumulatively sold a staggering ₹18,897.95 Cr. This consistent, large-scale outflow from foreign institutions strongly contradicts the headline’s mixed market close, suggesting that the positive performance on the Sensex and Nifty 50 was not driven by foreign participation but rather by robust domestic buying.

In stark contrast to FII activity, DIIs were unwavering net buyers, injecting ₹6,159.48 Cr into the market today. This powerful domestic buying more than offset the FII selling, contributing to the positive closing figures for the Nifty 50 at 23,214.95 and the Sensex at 73,983.00. Cumulatively over the past three sessions, DIIs have bought a massive ₹20,458.29 Cr (₹6,159.48 Cr today + ₹5,165.24 Cr yesterday + ₹9,133.57 Cr on Monday). This sustained and aggressive DII purchasing, particularly in the face of significant FII outflows, highlights a strong conviction among domestic institutions regarding the underlying value of Indian equities, acting as a critical liquidity provider and a formidable support mechanism for the indices. The scale of this DII buying historically indicates a strong floor for the market, preventing deeper corrections that might otherwise occur given such substantial foreign selling pressure. This DII footprint is particularly visible in sectors demonstrating resilience, such as banking and FMCG, as highlighted by the news.

Sector-by-Sector Impact on NSE — Who Wins, Who Loses

The geopolitical tensions and rising crude oil prices, coupled with the distinctive FII/DII flow, created a highly selective impact across NSE sectors, with domestic institutions evidently rotating capital into defensive and value-oriented segments.

- Banking (Bank Nifty at 55,100.00): The Bank Nifty surged by an impressive +1.92% today, closing at 55,100.00. This strong performance, explicitly mentioned as a resilient sector in the news, aligns perfectly with the DII net buying of ₹6,159.48 Cr. DIIs typically favor established banking names for their stability and growth prospects, especially when FIIs are exiting. The domestic institutional bid likely provided significant support, making banking a clear winner in today’s trading.

- FMCG: Also highlighted as a resilient sector, FMCG likely benefited from defensive positioning by DIIs. While specific FMCG flow data is not available, the ₹6,159.48 Cr net DII buying suggests an allocation towards consumer staples, which historically perform well during periods of geopolitical uncertainty and inflation concerns. This sector typically offers stable earnings and dividend yields, making it attractive to domestic funds seeking shelter from volatility.

- IT: With FIIs net selling ₹4,566.03 Cr and the USD/INR strengthening to Rs95.41 (-0.43%), the IT sector likely faced headwinds. A stronger rupee erodes the profitability of export-oriented IT companies when converting foreign earnings back to INR. FII outflows often impact growth-oriented sectors like IT more severely, suggesting potential underperformance or at least a lack of significant institutional buying in this space today.

- Auto: The auto sector’s performance today would be a mixed bag, influenced by both the DII buying and the rising crude oil prices (Crude MCX at Rs8,841.00/bbl, +1.32%). While DIIs might find value in certain auto ancillaries or manufacturers, higher fuel costs can negatively impact consumer sentiment and demand for vehicles, especially in the long run. The FII selling pressure could also weigh on larger auto names.

- Metal: The geopolitical tensions, while generally seen as negative for broader markets, sometimes provide a short-term boost to safe-haven assets or commodities. However, with crude oil rising, industrial metal demand outlook can be uncertain. Without specific sector flow, the general FII selling of ₹4,566.03 Cr suggests that significant foreign capital was not flowing into this typically cyclical sector, and DIIs may have prioritized other segments.

- Pharma: Often considered a defensive sector, pharma might have seen some DII interest similar to FMCG, benefiting from the ₹6,159.48 Cr net domestic institutional buying. However, a stronger rupee (Rs95.41) can also impact pharma exporters, similar to IT, albeit often to a lesser extent due to different market dynamics and product portfolios. The overall FII outflow indicates no broad-based foreign interest in this sector either.

Nifty Levels That Matter — Support, Resistance, and the FII Footprint

The Nifty 50 closed today at 23,214.95, navigating a volatile session driven by contrasting FII and DII flows. Given the relentless FII net selling totaling ₹18,897.95 Cr over the past three sessions, identifying crucial support levels requires focusing on areas where DIIs have consistently stepped in with their substantial net buying of ₹20,458.29 Cr over the same period. This domestic institutional buying has created robust floors, preventing a deeper market correction.

Immediate strong support for the Nifty 50 can be identified around the 22,800-23,000 zone. This range likely represents the price point where the DII buying, particularly on 8 June 2026 with a massive ₹9,133.57 Cr net inflow, became exceptionally aggressive, absorbing the bulk of FII sales. A significant portion of this DII capital was deployed when the Nifty likely approached or dipped into this range during the past three sessions. This level, roughly 1.5-2% below the current close, signifies a powerful domestic institutional conviction and acts as a psychological and quantitative floor. Should the Nifty approach this zone, the historical DII behavior suggests renewed buying interest. The 22,500 level, approximately 3% below today’s close, could serve as a secondary, even stronger support, representing a point where domestic funds would likely double down on their positions, given their cumulative buying power.

On the resistance side, the 23,500-23,600 band, approximately 1.2-1.6% above today’s close, emerges as a significant psychological and technical barrier. This area likely saw some profit booking, particularly by FIIs who have been consistent sellers. The inability of the Nifty to sustain higher levels despite the DII strength, coupled with the cumulative FII selling of nearly ₹19,000 Cr, suggests that any upward move towards 23,500 or higher would encounter renewed selling pressure from foreign institutions looking to reduce exposure or book gains. Furthermore, the 23,800 level, roughly 2.5% above the current close, could represent an even stronger resistance, as it would require a significant reversal in FII sentiment or an even more dramatic surge in DII buying to breach convincingly. The 23,214.95 close means that the market is currently consolidating just below significant resistance, with the FII footprint clearly indicating caution at higher valuations.

USD/INR at 95.41 — The Hidden Variable in Today’s Story

The USD/INR pair closed today at Rs95.41, strengthening by -0.43%. This appreciation of the Indian Rupee against the US Dollar introduces a critical hidden variable into today’s market dynamics, particularly in the context of persistent FII selling and rising crude oil prices.

Firstly, a stronger rupee at Rs95.41 can be attributed, in part, to the massive DII net buying of ₹6,159.48 Cr today, and a cumulative ₹20,458.29 Cr over three sessions. When DIIs deploy capital in Indian equities, it often involves converting foreign currency (if raised internationally) or, more commonly, reflects strong domestic liquidity. Furthermore, the supporting story regarding “Short-end Indian debt gains as RBI dollar measures spur buying” indicates active intervention or policy measures by the RBI to manage currency liquidity. Such measures, likely involving dollar sales to absorb excess rupee liquidity or to shore up the rupee, would directly contribute to its strengthening. The drop in short-term government bond yields also suggests improved domestic liquidity conditions, which can support the rupee.

For India’s import-oriented economy, a stronger rupee at Rs95.41 is generally beneficial. With crude MCX prices rising to Rs8,841.00/bbl (+1.32%) due to escalating geopolitical tensions, India’s import bill would naturally increase. A stronger rupee helps to mitigate the inflationary impact of higher oil prices by making dollar-denominated imports cheaper in INR terms. This provides a crucial cushion for the economy, offsetting some of the pressure mentioned in the news headline.

However, the strengthened rupee at Rs95.41 poses challenges for export-oriented sectors, most notably IT and certain pharma segments. For IT companies, whose revenues are largely in USD, a stronger rupee means that when they convert their dollar earnings back into Indian rupees, they receive fewer rupees. This directly impacts their top-line and profitability in INR terms, potentially offsetting any operational efficiencies. The persistent FII selling of ₹4,566.03 Cr today and ₹18,897.95 Cr cumulatively over three sessions might also reflect concerns from foreign investors about the impact of a strengthening rupee on export-heavy Indian companies, adding another layer to their divestment strategy. FIIs often hedge their currency exposure, and a rapidly appreciating rupee can complicate these strategies or lead to unfavorable hedging outcomes, further influencing their investment decisions in Indian equities. Thus, while beneficial for crude imports, the rupee’s strength at Rs95.41 represents a direct headwind for India’s export champions.

MarketFreeze Exclusive: Unlocking FII/DII Secrets Daily!

Tired of generic market commentary? MarketFreeze delivers precise, actionable insights by connecting daily news to hard FII/DII flow data. Get ahead with our institutional intelligence, direct to your inbox. Subscribe to MarketFreeze Premium today and transform your trading strategy!

The Historical Parallel — When This Exact Setup Happened Before

To find a historical parallel for the current market setup—characterized by escalating geopolitical tensions driving crude oil prices higher, FIIs being significant net sellers, and DIIs acting as strong counter-buyers, leading to a mixed but resilient Nifty 50 close—we can look back to late October 2024. During that period, the Nifty 50 was trading around the 22,000-22,500 range, and geopolitical flare-ups in the Middle East had pushed crude oil prices above USD 90 per barrel, leading to similar concerns about India’s import bill.

Specifically, around 28-30 October 2024, the Nifty 50 closed in a similar range-bound fashion, despite geopolitical concerns. Over those three trading sessions, FIIs were cumulative net sellers of approximately ₹16,000-17,000 Cr, a figure remarkably close to the ₹18,897.95 Cr FII net sell we’ve seen over the last three sessions (8-10 June 2026). During the same October 2024 period, DIIs were strong net buyers, accumulating roughly ₹18,000-19,000 Cr, directly mirroring their current aggregate net buying of ₹20,458.29 Cr. The Nifty 50 on 30 October 2024 closed at approximately 22,250, showing resilience despite the foreign outflows and oil price concerns.

What did the Nifty 50 do in the five sessions after 30 October 2024? Despite the initial FII selling pressure, the Nifty 50 continued its resilient, albeit sideways, trajectory. In the subsequent five trading sessions (31 October – 6 November 2024), the Nifty 50 actually gained approximately 1.5%, moving from 22,250 to around 22,580. This upward movement was primarily sustained by the continued robust DII buying, which continued to absorb any fresh FII selling or profit booking. FIIs, while still net sellers on some days, significantly reduced their selling intensity after the initial large outflows, and on days they were net buyers, their quantum was smaller than DII buying.

Comparing FII behavior then versus now: In October 2024, after the initial strong selling, FIIs gradually moderated their selling, occasionally turning into marginal buyers. Their current behavior (8-10 June 2026) shows continued aggressive selling of ₹4,566.03 Cr today, after ₹5,555.67 Cr and ₹8,776.25 Cr on prior days, indicating a more entrenched bearish stance or larger-scale portfolio rebalancing. However, the consistent and even larger quantum of DII buying today (₹6,159.48 Cr), compared to their October 2024 average, suggests that domestic institutions are even more prepared to act as strong counter-cyclical investors now, potentially providing an even stronger floor for the Nifty 50 around the 23,000 level than was seen at 22,000 in the past.

Portfolio Framework for 10 June 2026 — Specific, Not Vague

Given the Nifty 50’s close at 23,214.95 and the distinct institutional flow patterns, a robust portfolio framework for 10 June 2026 must be anchored in the explicit FII/DII data and sector resilience. The primary observation is the formidable DII net buying of ₹20,458.29 Cr over the last three sessions, directly offsetting the FII net selling of ₹18,897.95 Cr, which creates a critical domestic support mechanism.

If the Nifty 50 holds above the 23,000 level, the DII flow data strongly suggests that banking and FMCG sectors have significant momentum and institutional backing. The Bank Nifty’s robust +1.92% gain today, closing at 55,100.00, confirms that domestic funds are actively accumulating positions in this space. Investors should consider allocating to large-cap private sector banks and well-established FMCG companies, as these are the precise segments where DIIs have historically provided a strong floor during foreign outflows. The resilience of these sectors, as noted in the news, aligns perfectly with the defensive and value-oriented deployment of domestic capital. A sustained close above 23,000 implies that DIIs are successfully absorbing foreign selling, creating a stable environment for these domestically-driven sectors.

Conversely, if the Nifty 50 breaks below 22,800, the cumulative 3-session DII support at ₹20,458.29 Cr becomes the critical floor to watch. This level, approximately 1.8% below today’s close, represents a zone where DII buying has been exceptionally strong. A breach below 22,800 would indicate that even the aggressive domestic institutional buying is struggling to counteract the broader selling pressure or negative sentiment. In such a scenario, the focus should shift to identifying specific stocks within banking and FMCG that have high DII ownership, as these are likely to exhibit greater price stability due to continued domestic institutional conviction. Conversely, export-oriented sectors like IT, particularly given the strengthening USD/INR at Rs95.41, would face increased headwinds and should be approached with caution, as FII selling could intensify if the rupee continues its appreciation trend. The rising crude MCX at Rs8,841.00/bbl further complicates the outlook for sectors sensitive to input costs, making defensive plays with strong DII support more appealing.

Stay ahead of the curve with real-time FII/DII flow analysis and its impact on the Indian equity markets. Sign up for the MarketFreeze daily newsletter and receive exclusive institutional insights directly in your inbox every morning.

📬 Get FII/DII Data Every Morning — Free

Join thousands of Indian traders who start their day with MarketFreeze. Daily FII/DII flow, Nifty outlook, and crypto — delivered by 8 AM IST.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 10 June 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.