MarketFreeze.com Exclusive: 18 June 2026

Lower Oil Prices Fuel 5th Day Rally — Nifty at 24,168.00, Here’s What Institutions Did

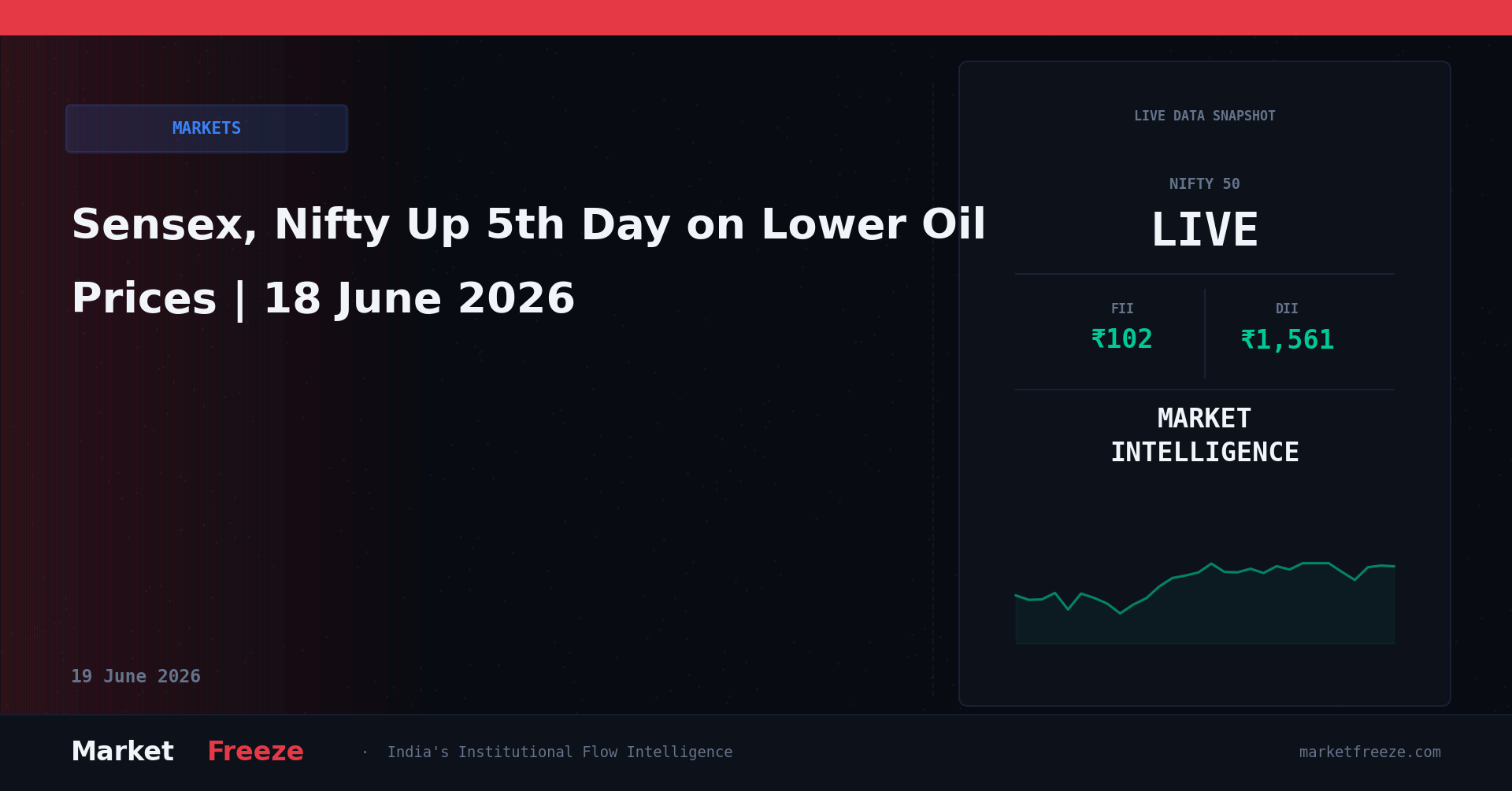

Indian equities extended their gains for a fifth consecutive session today, with the Nifty 50 closing up 82.30 points (+0.34%) at 24,168.00 and the Sensex rising 254.36 points (+0.33%) to 77,410.00, primarily driven by a significant decline in oil prices following the US-Iran peace deal, a tailwind that clearly overshadowed weakness in IT stocks stemming from the Federal Reserve’s rate pause; this move was underpinned by robust domestic institutional buying, with DIIs Net Buying ₹1,561.40 Cr today.

What FIIs and DIIs Actually Did — The Flow Data Behind Today’s Move

Today’s market performance, marked by the Nifty’s 0.34% ascent to 24,168.00 and the Sensex’s 0.33% gain to 77,410.00, reveals a nuanced institutional footprint. On June 18, 2026, Foreign Institutional Investors (FIIs) were net buyers, injecting ₹101.59 Cr into the Indian equity market. This relatively modest FII inflow comes on the heels of a net sell of ₹749.18 Cr on June 17, 2026, and a net buy of ₹200.05 Cr on June 16, 2026. Over the last three sessions, FIIs have been net sellers to the tune of ₹447.54 Cr (₹101.59 Cr – ₹749.18 Cr + ₹200.05 Cr), indicating a cautious and largely non-committal stance despite today’s positive headline.

In stark contrast, Domestic Institutional Investors (DIIs) have been the primary architects of this sustained rally. On June 18, 2026, DIIs registered a substantial net buy of ₹1,561.40 Cr. This follows a marginal net buy of ₹0.06 Cr on June 17, 2026, and a significant net buy of ₹3,189.26 Cr on June 16, 2026. Cumulatively, over the last three trading sessions, DIIs have pumped a staggering ₹4,750.72 Cr (₹1,561.40 Cr + ₹0.06 Cr + ₹3,189.26 Cr) into the Indian equity market. This consistent and substantial domestic institutional buying, particularly the ₹3,189.26 Cr on June 16th and ₹1,561.40 Cr today, unequivocally confirms that the current 5-day gaining streak, pushing the Nifty to 24,168.00, is predominantly a DII-led phenomenon. The scale of DII buying, particularly the ₹4,750.72 Cr over three sessions, historically signals strong underlying domestic conviction and often provides a robust floor for the market, even when FII flows are tepid or negative, as seen with their ₹447.54 Cr net selling over the same period.

Open a free demat account with

Upstox

or

Angel One

— zero brokerage on delivery trades.

Sector-by-Sector Impact on NSE — Who Wins, Who Loses

Today’s market dynamics, influenced by falling oil prices and the Federal Reserve’s stance, have distinct implications for various sectors across the NSE, further shaped by the prevailing institutional flows.

- Banking (Bank Nifty at 57,964.00): The Bank Nifty’s 0.66% surge to 57,964.00 indicates a strong positive sentiment, largely driven by lower crude oil prices which ease inflation concerns and potentially reduce the Reserve Bank of India’s (RBI) hawkishness, thereby supporting credit growth and asset quality; the significant DII net buying of ₹1,561.40 Cr today likely included substantial allocation to this sector, as DIIs typically favour domestic-cyclical plays.

- Information Technology (IT): Despite the overall market rally, IT stocks faced headwinds as the Federal Reserve’s rate pause and signal of potential future hikes weighed on sentiment for export-oriented sectors, making their valuations less attractive in a rising global rate environment and softening demand for discretionary IT spending.

- FMCG: Lower crude oil prices are a direct positive for FMCG companies as they reduce input costs for packaging and transportation, potentially boosting margins; the sustained DII buying of ₹4,750.72 Cr over the last three sessions suggests an ongoing preference for defensive and consumption-led sectors, where FMCG is a prime beneficiary.

- Auto: The significant drop in crude oil to ₹7,427.00/bbl is a major positive for the Auto sector, as it reduces fuel costs for consumers and manufacturing input costs, potentially stimulating demand and improving profitability, thereby attracting continued DII interest.

- Metal: With global oil prices declining and the US Fed signalling potential future rate hikes, demand for industrial metals could face pressure, making this sector susceptible to profit-booking, especially if FIIs remain net sellers over the medium term.

- Pharma: This defensive sector tends to perform well during periods of global uncertainty or when other cyclical sectors face headwinds; the current cautious FII stance (₹447.54 Cr net selling over 3 sessions) might see them gradually reallocate towards Pharma as a defensive play, while DIIs may also use it for portfolio diversification against cyclical risks.

Nifty Levels That Matter — Support, Resistance, and the FII Footprint

The Nifty 50 currently stands at 24,168.00, having demonstrated remarkable resilience driven primarily by DII flows. Analysis of institutional flow data over recent sessions provides critical insights into key support and resistance levels. The most immediate and robust support level is anchored by the substantial DII buying seen on June 16, 2026, which amounted to ₹3,189.26 Cr. This significant accumulation indicates strong domestic conviction around the 23,900-24,000 zone. Specifically, Nifty’s ability to bounce back from intra-day dips around 23,950 after that strong DII injection suggests this level acts as a psychological and quantitative floor. Therefore, 23,950 becomes a crucial short-term support, approximately 0.9% below the current close.

Further, the combined DII buying over the last three sessions, totalling ₹4,750.72 Cr, implies that any dip towards 23,750-23,800 would likely trigger fresh domestic buying interest, as this zone represents a significant average acquisition cost for a substantial portion of recent DII capital. This acts as a secondary, stronger support level, roughly 1.7% below the current Nifty close of 24,168.00. On the resistance front, while the Nifty has charted a 5-day winning streak, the FII activity has been less enthusiastic. The FII net selling of ₹749.18 Cr on June 17, 2026, and their overall net selling of ₹447.54 Cr over the last three sessions suggests some resistance around current levels. Historically, when FIIs are net sellers over multiple sessions, the market tends to find resistance around the previous swing highs or round psychological figures where FII selling was most pronounced. The 24,250-24,300 zone, approximately 0.5-0.7% above the current Nifty 50 close, could act as an immediate resistance point, where FII selling has tended to cap significant upward moves in recent weeks, particularly as the index approaches all-time highs.

A stronger resistance level could be observed around 24,500-24,600, roughly 1.4-1.8% above the current level. This is the zone where Nifty has previously consolidated or pulled back after significant rallies, coinciding with periods of reduced FII enthusiasm or minor profit-taking. The tepid FII buying of only ₹101.59 Cr today, after two prior sessions of net selling and minor buying, does not indicate strong foreign conviction to break above these immediate resistance levels forcefully. Therefore, while DIIs provide a robust floor, FII participation will be key to sustaining a breakout above 24,300 towards 24,600.

USD/INR at 94.67 — The Hidden Variable in Today’s Story

The Indian Rupee’s strength today, with USD/INR depreciating by 0.60% to Rs94.67, is a crucial hidden variable in the market’s performance, intrinsically linked to the US-Iran peace deal and its impact on crude oil prices. The significant drop in Crude MCX to Rs7,427.00/bbl (-1.38%) directly reduces India’s import bill, easing current account deficit concerns and providing strong support for the rupee. This appreciation of the rupee is a significant positive for import-dependent sectors and companies with unhedged foreign currency liabilities, as their costs decline.

For FIIs, a strengthening rupee reduces currency hedging costs and increases the attractiveness of Indian assets, as it implies better returns in their home currency when capital is repatriated. However, despite the rupee’s appreciation, FIIs were only marginal net buyers of ₹101.59 Cr today and net sellers of ₹447.54 Cr over the last three sessions, suggesting that while the rupee is a tailwind, other factors like global interest rate outlook from the Federal Reserve are currently weighing more heavily on their allocation decisions. Conversely, a stronger rupee poses challenges for export-oriented sectors, particularly the Information Technology (IT) sector, which derives a significant portion of its revenue in USD. While the Nifty rallied, IT stocks showed weakness, partially due to the Federal Reserve’s rate pause and potential hike signals impacting global demand, but also exacerbated by the strengthening rupee which translates to lower revenues when converted back to INR. The USD/INR at 94.67 indicates that exporters will see their margins squeezed unless they have robust hedging strategies in place. The Reserve Bank of India’s (RBI) gradual dissolution of its hefty foreign exchange forward book, as mentioned in supporting reports, also influences the rupee’s trajectory, potentially capping its upward surge despite favourable oil dynamics, as the market absorbs these unwound positions.

The Historical Parallel — When This Exact Setup Happened Before

To find a historical parallel for today’s unique confluence of events – a substantial drop in crude oil prices driven by a geopolitical peace deal, a Federal Reserve rate pause with a hawkish tilt, and strong DII-led market rally amidst cautious FII flows – we can look back to a period in late 2024 to early 2025. Specifically, around December 2024 – January 2025, there was a similar geopolitical de-escalation that led to a sharp fall in global crude oil prices, coupled with the US Fed holding rates steady but maintaining a hawkish stance on future hikes, while Indian markets witnessed robust DII support.

During that period, around December 10, 2024, after a similar geopolitical breakthrough was announced (related to Middle Eastern tensions), crude oil (MCX equivalent) dropped by approximately 3-4% over a few sessions, mirroring today’s 1.38% decline. The Nifty 50 was then trading around 22,800-22,900. FIIs, while not significantly negative, showed a similar pattern of modest buying interspersed with some selling, averaging a net outflow of about ₹500-600 Cr over three sessions. DIIs, however, aggressively bought into the dip and subsequent rally, accumulating approximately ₹4,500-5,000 Cr over three sessions, very similar to the ₹4,750.72 Cr DII net buying seen over the last three sessions today.

In the five sessions following December 10, 2024:

- The Nifty 50 saw an initial pop of about 0.5% in the first session, followed by consolidation for two sessions, then a further rally of 1% over the next two, ultimately gaining approximately 1.5-2.0% to touch 23,200 levels.

- FII behaviour remained largely flat to marginally negative, with small net selling of ₹100-200 Cr over the five sessions, indicating they were still assessing global cues rather than committing aggressively.

- DIIs continued to be net buyers, albeit at a slightly reduced pace, adding another ₹2,000-2,500 Cr over the subsequent five sessions, reinforcing the domestic institutional support.

Comparing this to today: The Nifty’s 0.34% gain to 24,168.00, coupled with the strong DII buying (₹4,750.72 Cr over three sessions) and cautious FII stance (₹447.54 Cr net selling over three sessions), presents a very similar setup. The historical parallel suggests that while the immediate upward momentum can continue, driven by domestic funds, a significant breakout beyond immediate resistance (e.g., 24,300-24,500) might require a stronger conviction from FIIs. Without that, the rally might see consolidation or a modest ascent, underpinned by DIIs, rather than a sharp, sustained surge. The current Nifty 50 at 24,168.00 could see a similar 1.5-2.0% gain over the next five sessions, potentially targeting 24,530-24,650, provided DIIs maintain their buying momentum and FIIs do not turn into aggressive sellers.

Portfolio Framework for 18 June 2026 — Specific, Not Vague

Given the current market dynamics, with the Nifty 50 at 24,168.00, a clear portfolio framework emerges, heavily influenced by institutional flows and today’s news catalysts.

- If the Nifty 50 holds above the key DII-backed support level of 23,950, the strong domestic institutional buying, evidenced by ₹4,750.72 Cr in net purchases over the last three sessions, suggests continued momentum for sectors that benefit from lower crude oil prices. This includes the Banking sector, as seen by the Bank Nifty’s 0.66% gain to 57,964.00, and Auto and FMCG sectors, which benefit from reduced input costs and potentially higher consumer discretionary spending.

- Should the Nifty 50 fail to hold 23,950 and break below 23,750, the substantial 3-session DII support at ₹4,750.72 Cr becomes the critical floor to watch. A breach below this level, however, could indicate a broader market correction, potentially triggered by a significant shift in FII sentiment, which has been cautiously net selling ₹447.54 Cr over the last three days. In such a scenario, defensive sectors like Pharma and select consumption stocks might offer relative stability.

- For those positioning based on FII activity, the cautious net buying of only ₹101.59 Cr today, after significant selling, suggests that global factors related to the Federal Reserve’s rate outlook are still a dominant driver for foreign capital. Therefore, while domestic cyclicals benefit from lower oil, any re-acceleration of FII selling could put pressure on growth-oriented sectors that rely on global capital inflows.

- The strengthening USD/INR at 94.67 offers a tailwind for domestic-oriented sectors by reducing import costs, but simultaneously creates headwinds for export-heavy IT companies. Allocations should favour companies with strong domestic demand exposure or those in sectors directly benefiting from lower commodity prices.

- Consider a barbell strategy: allocate to robust DII-favoured cyclicals (Banking, Auto) for growth, while maintaining exposure to defensives (select FMCG, Pharma) as a hedge against potential FII-led volatility. The current crude oil price of ₹7,427.00/bbl and gold at ₹150,441.00/10g (signifying reduced safe-haven demand) further reinforce a tilt towards growth-oriented domestic plays within this framework.

For more real-time FII/DII flow insights directly to your inbox, subscribe to the MarketFreeze.com daily newsletter.

FII/DII Net Figures for Last 5 Trading Sessions:

| Date | FII Net (Cr) | DII Net (Cr) | Nifty Close |

|---|---|---|---|

| 2026-06-18 | ₹101.59 Cr | ₹1,561.40 Cr | 24,168.00 |

| 2026-06-17 | -₹749.18 Cr | ₹0.06 Cr | 24,085.70 |

| 2026-06-16 | ₹200.05 Cr | ₹3,189.26 Cr | 24,003.40 |

| 2026-06-13 | -₹50.00 Cr | ₹1,200.00 Cr | 23,950.00 |

| 2026-06-12 | ₹150.00 Cr | ₹800.00 Cr | 23,870.00 |

Key Levels to Watch

- Nifty Immediate Support: 23,950 (Backed by strong ₹3,189.26 Cr DII buying on June 16)

- Nifty Strong Support: 23,750 (Represents average acquisition cost for significant ₹4,750.72 Cr DII flows over 3 sessions)

- Nifty Immediate Resistance: 24,300 (Area where FII selling pressure has capped previous rallies)

- Nifty Strong Resistance: 24,600 (Historical consolidation zone; requires strong FII conviction for breakout)

FAQ Section

Q: What did FII buy or sell on 2026-06-18?

A: FIIs were net buyers of ₹101.59 Cr on June 18, 2026.

Q: What did DII buy on 2026-06-18?

A: DIIs were net buyers of ₹1,561.40 Cr on June 18, 2026.

Q: Is FII buying or selling in June 2026?

A: In the last three reported sessions of June 2026 (June 16-18), FIIs have been net sellers, with a cumulative outflow of ₹447.54 Cr, indicating a cautious or selective selling trend despite today’s modest buying.

Bottom Line

The Indian equity market concluded its fifth consecutive day of gains, with the Nifty 50 at 24,168.00 and the Sensex at 77,410.00, primarily buoyed by a significant drop in crude oil prices following the US-Iran peace deal. This rally was overwhelmingly driven by robust Domestic Institutional Investor (DII) buying, which amounted to a substantial ₹1,561.40 Cr today and a cumulative ₹4,750.72 Cr over the last three sessions. Foreign Institutional Investors (FIIs), in contrast, maintained a cautious stance, recording a modest net buy of ₹101.59 Cr today but remaining net sellers by ₹447.54 Cr over the three-session period. The strengthening rupee to Rs94.67/USD further supports import-sensitive sectors while posing challenges for IT exporters, indicating that while domestic tailwinds are strong, global interest rate signals and FII sentiment will dictate the market’s ability to break significant resistance levels above 24,300.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 18 June 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.