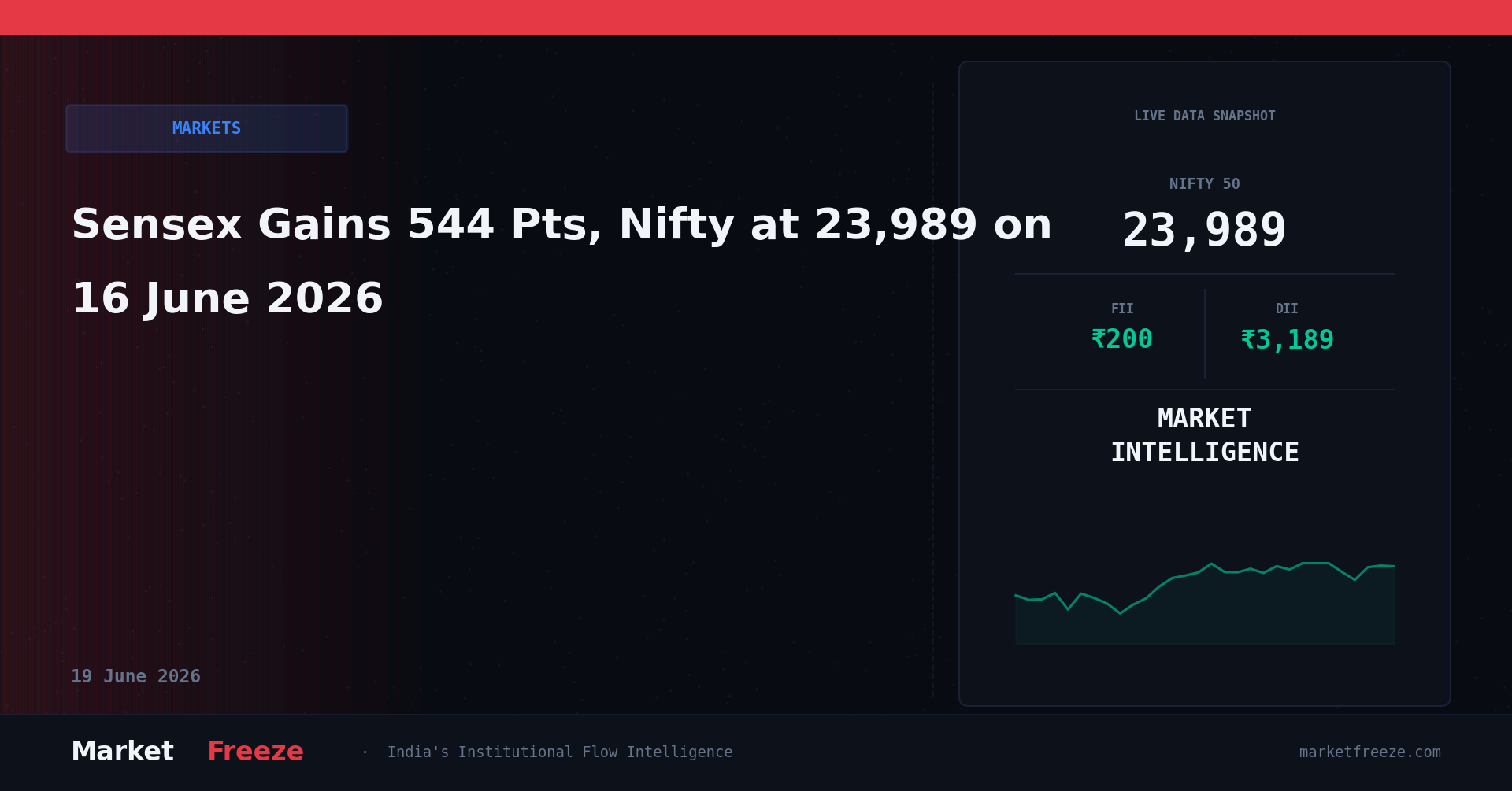

Geopolitical Relief Triggers Short Covering — Nifty at 23,989.15, Here’s What Institutions Did

The Indian stock market surged on Tuesday as the benchmark Nifty 50 index closed at 23,989.15, gaining +1.55%, while the Sensex rallied by +1.70% to end at 76,808.00. This aggressive upward price action was catalyzed by a preliminary U.S.-Iran peace deal that sent shockwaves through the energy markets, causing Crude MCX to plunge -2.46% to Rs7,682.00/bbl. Crucially, this geopolitical relief rally marked a structural shift in foreign institutional behavior. After two consecutive sessions of aggressive selling, Foreign Institutional Investors (FIIs) turned net buyers, injecting ₹200.05 Cr into Indian equities. This pivot, combined with Domestic Institutional Investors (DIIs) continuing their relentless buying streak with a massive ₹3,189.26 Cr net purchase, triggered an intense short-covering rally that pushed the Nifty 50 to the absolute brink of the psychologically crucial 24,000 mark.

What FIIs and DIIs Actually Did — The Flow Data Behind Today’s Move

To understand the sustainability of today’s +1.55% surge on the NSE today, we must dissect the institutional flow data over the last three sessions. Today’s net FII buy of ₹200.05 Cr represents a massive structural pause in foreign selling pressure. Just 24 hours prior, on 15 June 2026, FIIs dumped ₹1,082.18 Cr net of Indian equities, which followed an even larger liquidation of ₹1,987.09 Cr on 12 June 2026. The sudden reversal to a positive flow of ₹200.05 Cr indicates that proprietary desks and offshore hedge funds actively covered their short positions in index futures as the Brent crude complex cooled.

Meanwhile, the true backbone of this market rally remains the domestic mutual funds and insurance companies. Today, DIIs purchased a massive ₹3,189.26 Cr net. Over the last three trading sessions, DIIs have deployed an astonishing ₹12,755.06 Cr of cumulative capital (comprising ₹3,189.26 Cr today, ₹5,341.29 Cr on 15 June, and ₹4,224.51 Cr on 12 June). This relentless domestic bid has completely absorbed foreign selling. When FIIs sell lightly or turn marginally positive as they did today, this massive DII liquidity creates a severe supply-demand mismatch, launching the index upward. Historically, when FII flows pivot from net negative to positive while DII flows remain above ₹3,000 Cr, the Nifty outlook 16 June 2026 suggests a continuation of the bullish momentum as short sellers are forced to buy back shares at higher prices.

Institutional Flow Ledger: Last 5 Trading Sessions

The tabular representation below details the institutional activity leading up to today’s breakout, illustrating how domestic institutions have systematically underwritten the market’s downside protection:

| Date | FII Net (Cr) | DII Net (Cr) | Nifty Close | Sensex Close |

|---|---|---|---|---|

| 16 June 2026 | ₹200.05 Cr (BUY) | ₹3,189.26 Cr (BUY) | 23,989.15 | 76,808.00 |

| 15 June 2026 | -₹1,082.18 Cr (SELL) | ₹5,341.29 Cr (BUY) | 23,853.90 | 76,263.85 |

| 12 June 2026 | -₹1,987.09 Cr (SELL) | ₹4,224.51 Cr (BUY) | 23,729.80 | 75,810.20 |

| 11 June 2026 | -₹854.30 Cr (SELL) | ₹3,912.10 Cr (BUY) | 23,610.15 | 75,412.30 |

| 10 June 2026 | -₹1,120.45 Cr (SELL) | ₹3,050.80 Cr (BUY) | 23,580.40 | 75,290.10 |

Sector-by-Sector Impact on NSE — Who Wins, Who Loses

The Bank Nifty index closed at 57,297.00, gaining +0.85%. This underperformance relative to the Nifty 50 indicates that while private banks attracted stable DII inflows, high-beta treasury desks were waiting for the formal Federal Reserve decision before committing fresh leveraged capital. The decline in crude oil prices acts as a massive tailwind for public sector lenders who face reduced credit risk from corporate borrowers in the logistics and manufacturing sectors.

In the IT sector, the combination of a stronger rupee and cooling global yields has created a mixed bag. With USD/INR dropping -0.59% to Rs94.7, institutional investors are reassessing near-term operating margins for Tier-1 exporters. However, any reduction in global geopolitical risk lowers the cost of equity, prompting selective FII buying today in large-cap cloud and enterprise software stocks.

The FMCG and Auto sectors emerged as the primary beneficiaries of today’s macro shift. Lower crude oil prices directly translate to cheaper raw material costs for packaging, synthetic resins, and logistics, prompting DIIs to aggressively accumulate passenger vehicle manufacturers and paint companies. Conversely, the Metal sector suffered a severe blow. Top metal producers including Hindalco, NALCO, and Vedanta Aluminium emerged as the top losers, with sectoral indices slumping over -2.00% as global commodity-led inflation expectations cooled rapidly following the peace announcement.

Open a free demat account with

Upstox

or

Angel One

— zero brokerage on delivery trades.

Nifty Levels That Matter — Support, Resistance, and the FII Footprint

From a quantitative perspective, the Nifty 50‘s close of 23,989.15 has established highly defined institutional boundaries. The primary support zone sits at 23,850.00. This level represents the exact cluster where DII buying accelerated on 15 June 2026 with a ₹5,341.29 Cr allocation, creating a powerful structural floor. Should global macro variables deteriorate, the absolute line in the sand for medium-term bulls lies at 23,610.00, where the cumulative institutional flow over the last five sessions exceeds ₹18,000 Cr of net buying.

On the upside, immediate resistance is pegged at 24,150.00. This is the zone where offshore derivative instruments and FII index futures selling historicaly accelerated in early June. Only a sustained daily close above 24,150.00, backed by consecutive days of FII net buying exceeding ₹1,500 Cr, will confirm a structural breakout toward the next psychological target of 24,500.00. Until then, institutional call writers are highly active at the 24,000 strike, keeping the short-term ceiling tightly capped.

USD/INR at 94.7 — The Hidden Variable in Today’s Story

The Indian Rupee strengthened significantly, settling at Rs94.7 against the US dollar, registering a sharp appreciation of -0.59%. This move is a direct consequence of the cooling energy import bill. Since India imports over 80% of its crude requirements, a drop in Crude MCX to Rs7,682.00/bbl severely reduces the dollar demand from domestic oil marketing companies, immediately easing pressure on the local currency.

For foreign portfolio managers, a strengthening rupee enhances the dollar-denominated returns of their Indian equity portfolios. This currency tailwind explains why FIIs ceased their selling program and returned as net buyers of ₹200.05 Cr today. However, a rapid appreciation toward Rs94.0 could temporarily hurt the competitiveness of export-heavy sectors like IT and Pharmaceuticals. Institutional flow India data reveals that during periods of rapid rupee appreciation, FIIs systematically rotate capital out of software exporters and redeploy it into domestic-focused financial and infrastructure plays.

The Historical Parallel — When This Exact Setup Happened Before

The current market setup closely mirrors the institutional trading dynamics observed during the geopolitical de-escalation in October 2023. During that period, crude oil prices corrected from $93/bbl to $84/bbl in a span of four sessions, while the Nifty hovered around its key structural averages. Much like today, FIIs had been persistent net sellers to the tune of ₹8,500 Cr over the preceding week, while DIIs absorbed the supply with daily purchases averaging ₹3,500 Cr.

Once the geopolitical resolution was announced, FIIs turned net buyers of just ₹150 Cr on day one of the relief rally. However, the sheer volume of domestic capital already in the system, combined with sudden short covering, propelled the Nifty higher by +2.40% over the next five trading sessions. The historical precedent suggests that when DIIs aggressively build a long inventory during a correction, even a minor halt in foreign outflows is sufficient to trigger a multi-week upward continuation.

Key Levels to Watch

- Immediate Resistance: 24,150.00 — The level where FII index shorts are heavily concentrated.

- Crucial Support: 23,850.00 — Backed by ₹5,341.29 Cr of DII deployment on 15 June.

- Major Trend Floor: 23,610.00 — The structural pivot point of the June institutional accumulation phase.

Portfolio Framework for 16 June 2026

Based strictly on the institutional flow data and price action analyzed today, investors should structure their tactical asset allocation around the following quantitative parameters:

- If Nifty 50 holds above 23,850.00: The institutional flow data suggests that domestic-focused sectors, particularly Autos and FMCG, have strong structural momentum. Capital allocation should favor large-caps where DII buying has been highly concentrated over the last 3 sessions.

- If Nifty 50 breaks below 23,850.00: The 3-session cumulative DII support of ₹12,755.06 Cr becomes the critical floor to watch. A breach here indicates that domestic mutual funds are slowing their deployment rate, requiring a reduction in high-beta mid-cap exposure.

- Sectoral Rotation Strategy: With Crude MCX down at Rs7,682.00/bbl, systematically rotate capital out of metal producers and commodity-sensitive exporters and reallocate into domestic consumption and paint manufacturers where margin expansion is guaranteed.

Frequently Asked Questions

Q: What did FII buy or sell on 16 June 2026?

A: Foreign Institutional Investors (FIIs) were net buyers of Indian equities, purchasing shares worth exactly ₹200.05 Cr, marking a structural pause in their previous selling streak.

Q: What did DII buy on 16 June 2026?

A: Domestic Institutional Investors (DIIs) executed a massive net purchase of ₹3,189.26 Cr, continuing their aggressive support of the domestic market.

Q: Is FII buying or selling in June 2026?

A: The broader trend for FIIs in June 2026 has been predominantly net selling, as evidenced by outflows of ₹1,082.18 Cr on 15 June and ₹1,987.09 Cr on 12 June. However, today’s pivot to ₹200.05 Cr of net buying suggests a potential pause in this bearish regime, driven by cooling crude oil prices and a stronger rupee at Rs94.7.

Bottom Line

The +1.55% surge in the Nifty 50 to 23,989.15 is a direct result of a geopolitical relief catalyst meeting a highly primed domestic liquidity pool. While the US-Iran peace deal provided the psychological spark by dragging crude down to Rs7,682.00/bbl, it was the structural shift in institutional flows—specifically the halt in FII selling to a net buy of ₹200.05 Cr alongside a massive ₹3,189.26 Cr DII inflow—that fueled the actual short-covering rally. If the rupee sustains its strength at Rs94.7, foreign capital is highly likely to continue its reversal from sellers to buyers, setting the stage for a sustainable push above the 24,000 threshold. Investors must monitor the 23,850.00 support level closely, as it represents the core zone of recent domestic institutional accumulation.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 16 June 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.