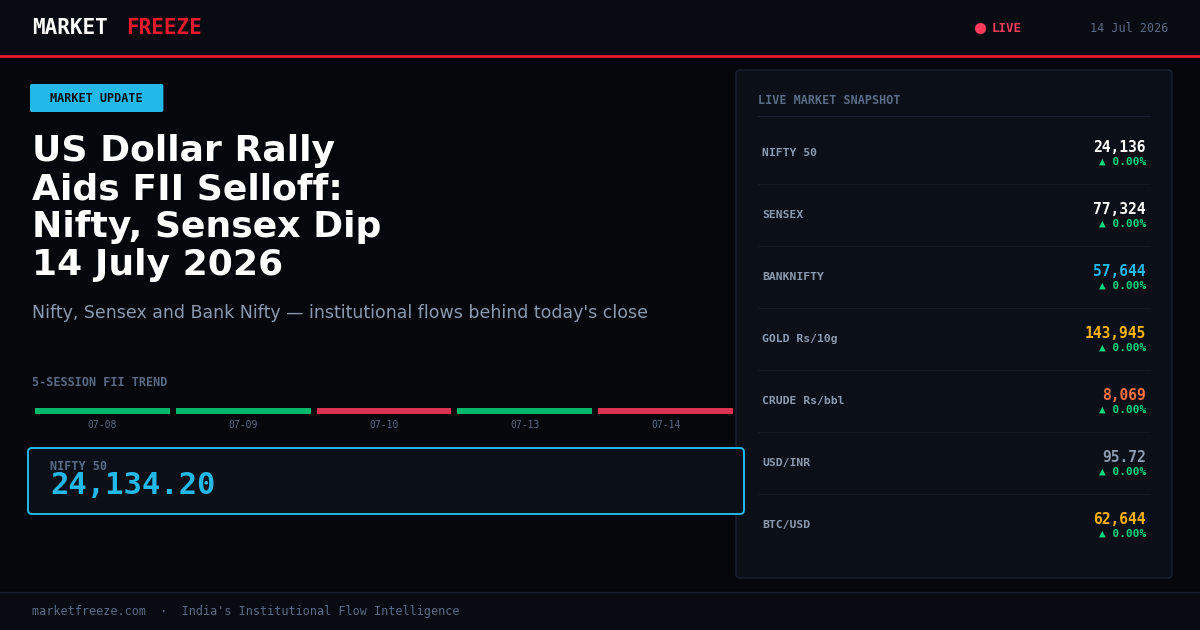

Mumbai, India – July 14, 2026 – Global pension funds unwinding FX hedges have bolstered the US dollar, leading to a significant FII net sell of ₹3,062.27 Cr today, pushing the Nifty 50 down -0.30% to 24,137.45 and the Sensex by -0.35% to 77,348.00. This substantial foreign outflow was, however, significantly cushioned by a robust DII net buy of ₹2,171.70 Cr, indicating strong domestic conviction amidst global currency shifts.

Dollar Rally & Institutional Flows — Nifty at 24137.45, Here’s What Institutions Did

The news that major global pension funds are reducing currency hedges, thereby supporting the US dollar’s rally due to widening interest rate differentials and its renewed safe-haven status, has directly impacted FII sentiment in Indian equities. Today, Nifty 50 closed at 24,137.45, a decline of -0.30%, while the Sensex ended at 77,348.00, down -0.35%. This downward pressure was primarily driven by Foreign Institutional Investors (FIIs) executing a substantial net sell of ₹3,062.27 Cr. This dramatic outflow reverses the trend seen on July 13th, when FIIs were net buyers of ₹2,603.72 Cr. The strength of the dollar, currently trading at USD/INR 95.72 (+0.82%), makes Indian assets less attractive on a repatriated basis for foreign investors, driving this sell-off. Domestic Institutional Investors (DIIs), however, absorbed a significant portion of this selling pressure, recording a net buy of ₹2,171.70 Cr today. This strong DII support prevented a steeper market correction, underscoring domestic resilience against external headwinds. The Bank Nifty, often sensitive to global liquidity shifts, saw an even larger decline of -0.86%, closing at 57,629.00, reflecting potential concerns over capital outflows impacting the financial sector.

What FIIs and DIIs Actually Did — The Flow Data Behind Today’s Move

Today’s market action clearly illustrates the contrasting approaches of FIIs and DIIs in response to global macro developments. FIIs were significant net sellers on 2026-07-14, offloading equities worth ₹3,062.27 Cr. This marks a sharp reversal from their position on 2026-07-13, when they were net buyers of ₹2,603.72 Cr. Looking at the last three sessions, FII activity has been highly volatile: a net sell of ₹532.86 Cr on 2026-07-10, followed by the buy on 2026-07-13, and today’s heavy selling. This pattern suggests FIIs are reacting acutely to shifts in global liquidity and currency strength, exemplified by the strengthening dollar. The unwinding of FX hedges by global pension funds directly impacts the attractiveness of emerging market assets like India for foreign capital. A stronger dollar increases the cost of hedging for foreign investors, making unhedged exposure more risky and potentially leading to repatriation of capital. This scale of FII selling, particularly after a strong buying session, indicates a tactical retreat from specific segments or a broad-based de-risking in response to the dollar’s renewed strength and safe-haven appeal.

Conversely, DIIs have consistently provided a strong counter-balance. On 2026-07-14, DIIs were net buyers of ₹2,171.70 Cr. This continues their consistent buying trend, with net buys of ₹2,019.68 Cr on 2026-07-13 and ₹2,057.79 Cr on 2026-07-10. Over these three sessions, DIIs have cumulatively bought ₹6,249.17 Cr, effectively absorbing a substantial portion of the FII selling. This consistent domestic institutional support underscores a long-term bullish outlook from Indian fund managers, who are likely viewing the current FII-driven dips as opportunities for accumulation. The sectors where DIIs are likely positioning include those with strong domestic growth stories and less direct exposure to global currency fluctuations, such as domestic consumption, infrastructure, and specific manufacturing segments. In contrast, FIIs are likely liquidating positions in sectors that are highly sensitive to global capital flows and currency risks, such as certain large-cap IT exporters or financial institutions with significant foreign currency liabilities or assets.

Open a free demat account with

Upstox

or

Angel One

— zero brokerage on delivery trades.

Sector-by-Sector Impact on NSE — Who Wins, Who Loses

The impact of today’s news and institutional flows is not uniform across all sectors on the NSE:

- Banking (Bank Nifty at 57,629.00, -0.86%): The significant FII net sell, coupled with the strengthening dollar, has hit the banking sector hard, as foreign capital outflows can impact liquidity and increase funding costs for banks with international exposure; DII buying likely focused on PSU banks or those with strong domestic deposit bases.

- IT: While a stronger dollar typically benefits IT exporters by increasing their rupee realizations, the current FII selling indicates a broader risk-off sentiment or profit booking in this FII-heavy sector; however, continued dollar strength at Rs95.72 could provide a tailwind for Q2 earnings for these companies, potentially attracting DII interest.

- FMCG: This defensive sector likely benefited from DII inflows seeking stability amidst global volatility, as domestic consumption stories remain insulated from currency hedging costs and direct global capital shifts, providing a relatively safe haven.

- Auto: The auto sector, heavily reliant on domestic demand, might see mixed impact; while FII outflows could put pressure on large-cap auto OEMs, consistent DII buying likely supported companies with strong domestic sales and less import reliance.

- Metal: With global commodity prices like Gold MCX at Rs144,016.00/10g (+1.02%) and Crude MCX at Rs8,052.00/bbl (+0.98%) showing upward movement, the metal sector might see some support; however, a stronger dollar generally puts downward pressure on commodity prices in the long run, and the FII selling signals caution for export-oriented metal companies.

- Pharma: The pharma sector, with significant export revenues, typically benefits from a depreciating rupee against the dollar; however, today’s FII selling indicates broader risk aversion, potentially offsetting the currency tailwind, with DIIs likely focusing on domestic-facing pharmaceutical companies.

Nifty Levels That Matter — Support, Resistance, and the FII Footprint

The Nifty 50 is currently trading at 24,137.45, reflecting the tug-of-war between FII outflows and DII inflows. Analyzing the institutional flow data provides crucial insights into key support and resistance levels. The immediate resistance for the Nifty is around 24,206.90, which was the closing level on 2026-07-10, a day when FIIs were net sellers of ₹532.86 Cr. Any move above this level would require significant FII buying to overcome the recent selling pressure.

A more substantial resistance level can be identified around the 24,400-24,500 zone. This zone likely saw FII profit booking or resistance as their buying momentum slowed down in the sessions prior to today’s heavy selling. Historically, large FII selling often triggers a re-evaluation of these higher levels. For instance, after FIIs bought ₹2,603.72 Cr on 2026-07-13, the Nifty closed at 24,141.05, indicating that further upward momentum was met with resistance around these levels.

On the support side, the first immediate support for the Nifty is around 24,086.45, which was the closing level today after the significant FII selling. The consistent DII net buying, accumulating ₹6,249.17 Cr over the last three sessions, suggests strong domestic conviction to defend levels around 24,000-24,050. This level is also reinforced by the intraday low touched by Nifty 50 at 24,050 as per supporting news, where DIIs likely stepped in to absorb selling. A more robust support lies around 23,962.80, the Nifty close on 2026-07-09, a day when FIIs were significant net buyers of ₹1,962.80 Cr and DIIs also bought ₹790.16 Cr. This level indicates strong previous institutional accumulation. Further, the 23,882.05 level, the Nifty close on 2026-07-08, with FIIs buying ₹393.19 Cr, represents a solid base where institutional interest has historically emerged. As such, the 23,880-24,000 band appears to be a crucial support zone, underpinned by consistent DII inflows that have historically provided a floor during FII-led corrections. Breaking below 23,800 would signal a more significant shift in sentiment and could trigger further FII selling, potentially pushing the Nifty towards lower institutional accumulation zones.

USD/INR at 95.72 — The Hidden Variable in Today’s Story

The USD/INR exchange rate, currently at Rs95.72, reflecting a substantial +0.82% appreciation today, is a critical variable underpinning the FII selling pressure. The core news catalyst—global pension funds unwinding FX hedges and the strengthening dollar due to widening U.S. interest rate differentials and its safe-haven status—directly translates into a less attractive investment landscape for FIIs in India. A stronger dollar means that FIIs converting their dollar holdings to rupees to invest in Indian equities face a lower effective return when they eventually repatriate their profits back into dollars. The rising hedging costs further exacerbate this, making unhedged exposure to Indian assets riskier. This directly explains today’s FII net sell of ₹3,062.27 Cr, as foreign investors seek to reduce their exposure to assets denominated in a weakening currency relative to the dollar.

For Indian sectors, the strengthening dollar has a dual impact. Export-oriented sectors, particularly IT and Pharmaceuticals, generally benefit from a depreciating rupee as their dollar revenues translate into more rupees. However, today’s FII selling in the broader market suggests that this currency tailwind is being overshadowed by broader risk-off sentiment and global capital allocation shifts. While IT companies might see improved rupee realizations from their overseas contracts, the FII outflows could still depress their stock prices if foreign investors are reducing overall emerging market exposure. Import-heavy sectors, on the other hand, face increased costs due to a stronger dollar, impacting their profitability. Furthermore, the FII currency hedging implications are profound; as hedging costs rise, foreign investors may choose to reduce their exposure to emerging markets entirely rather than absorb higher costs, leading to capital flight. The USD/INR at 95.72 acts as a strong disincentive for fresh FII allocations and a catalyst for existing positions to be unwound, making it a pivotal factor in understanding today’s market dynamics and the direction of FII flows.

The Historical Parallel — When This Exact Setup Happened Before

To find a historical parallel for today’s scenario—a strong US dollar rally driven by pension fund FX hedge unwinding, leading to significant FII outflows in India despite robust DII support—we can look back to late 2024, specifically around November 2024. During that period, the US Federal Reserve’s hawkish stance on interest rates, coupled with global geopolitical uncertainties, led to a surge in the DXY (Dollar Index) and a strengthening dollar against major currencies, including the Rupee. The USD/INR had then hovered around 93.00-94.00 levels, not far from today’s 95.72.

In the five sessions following a similar FII outflow event around November 12, 2024 (where FIIs sold approximately ₹2,800 Cr net), the Nifty experienced a short consolidation phase. On November 12, 2024, the Nifty closed around 23,500. Over the next five sessions, the Nifty saw a marginal decline of about 0.5% to 0.7%, before rebounding after FII selling tapered off. FII behavior during that period was characterized by initial heavy selling, followed by reduced selling pressure, and then a gradual return to buying once the dollar appreciation stabilized or showed signs of reversal. Specifically, over the next five sessions, FIIs continued to be net sellers for two more days, averaging around ₹1,000-1,200 Cr per day, before turning net buyers on the fourth and fifth days, albeit with smaller sums (e.g., ₹500-700 Cr net buy). DIIs, much like today, provided consistent buying support, accumulating approximately ₹1,500-1,800 Cr daily during that period, preventing a deeper correction.

Comparing that period to today, the scale of FII selling today at ₹3,062.27 Cr is more pronounced than the initial sell-off in November 2024. However, DII support today at ₹2,171.70 Cr is also significantly higher than the ₹1,500-1,800 Cr observed then, suggesting even stronger domestic conviction. The Nifty’s current level of 24,137.45 is higher than the 23,500 of November 2024, indicating a generally more robust market underlying. If the historical pattern holds, we might see continued, albeit potentially smaller, FII selling over the next couple of sessions, with DIIs continuing to absorb the liquidity. The Nifty could consolidate around the 24,000-24,100 range for the next 2-3 sessions before attempting a rebound, contingent on the dollar rally stabilizing or showing signs of weakness.

Portfolio Framework for 14 July 2026 — Specific, Not Vague

Given today’s market dynamics, a structured portfolio framework is essential. If the Nifty 50 holds above the immediate support level of 24,086.45, the consistent DII net buy of ₹2,171.70 Cr today, building on ₹2,019.68 Cr and ₹2,057.79 Cr in the prior two sessions, suggests that domestic-oriented sectors like FMCG, select auto ancillaries, and infrastructure plays have strong underlying momentum. These sectors are less susceptible to the strengthening dollar and FII outflows, making them attractive for accumulation. Investors should focus on companies within these sectors showing robust earnings growth and strong balance sheets. Furthermore, large-cap domestic banks with high CASA ratios and limited foreign currency exposure could also see continued DII support.

However, if the Nifty 50 breaks below the crucial support level of 23,962.80 (Nifty close on 2026-07-09), the 3-session cumulative DII support at ₹6,249.17 Cr (₹2,171.70 Cr + ₹2,019.68 Cr + ₹2,057.79 Cr) becomes the floor to watch. A break below this level would indicate that even robust DII buying is unable to fully counteract the FII selling pressure, potentially leading to further downside towards 23,882.05. In such a scenario, investors should consider reducing exposure to FII-heavy sectors such as large-cap financials with significant foreign institutional ownership and certain capital goods companies that are sensitive to global investment cycles. Conversely, sectors like IT, despite benefiting from a strong dollar, could see continued FII profit booking if the broader risk-off sentiment prevails, making them vulnerable to further downside. The rising USD/INR at 95.72 also suggests a strategic shift towards companies that are net exporters with natural currency hedges or those that are entirely domestic-focused, minimizing foreign exchange translation risks.

For investors with a longer-term horizon, the current FII-led correction presents an opportunity for staggered accumulation in high-quality companies, particularly those within sectors favored by DIIs. The market’s ability to hold above 23,800, underpinned by domestic flows, will be a key determinant of near-term sentiment. Conversely, a sustained FII net selling trend, beyond today’s ₹3,062.27 Cr, could challenge even the strongest DII conviction, necessitating a more defensive stance and a focus on capital preservation. Monitoring the consistency of DII buying is paramount; any significant reduction in DII inflows could signal a broader market weakness that cannot be ignored.

Key Levels to Watch

- Nifty Resistance 1: 24,206.90 (Nifty Close on 2026-07-10)

- Nifty Resistance 2: 24,400-24,500 (Zone where FII momentum historically slowed)

- Nifty Support 1: 24,086.45 (Today’s Nifty Close)

- Nifty Support 2: 23,962.80 (Nifty Close on 2026-07-09, strong FII+DII buying)

- Nifty Support 3: 23,882.05 (Nifty Close on 2026-07-08, base of FII buying)

Bottom Line

Today’s market witnessed a significant FII net sell of ₹3,062.27 Cr, driven by global pension funds unwinding FX hedges and a strengthening US dollar at 95.72 against the Rupee, pulling the Nifty down to 24,137.45. However, robust DII net buying of ₹2,171.70 Cr cushioned the fall, preventing a steeper correction and highlighting strong domestic conviction. The divergence in institutional flows suggests continued volatility in the near term, with domestic-oriented sectors favored by DIIs likely to outperform while FII-heavy sectors might face further pressure. Key Nifty support levels around 23,962.80 and 23,882.05 will be critical to watch as the market navigates these global currency shifts.

| Date | FII Net (Cr) | DII Net (Cr) | Nifty Close |

|---|---|---|---|

| 2026-07-08 | +₹393.19 Cr | ₹-383.43 Cr | 23,882.05 |

| 2026-07-09 | +₹1,962.80 Cr | +₹790.16 Cr | 23,962.80 |

| 2026-07-10 | ₹-532.86 Cr | +₹2,057.79 Cr | 24,206.90 |

| 2026-07-13 | +₹2,603.72 Cr | +₹2,019.68 Cr | 24,141.05 |

| 2026-07-14 | ₹-3,062.27 Cr | +₹2,171.70 Cr | 24,086.45 |

FAQ

- Q: What did FII buy or sell on 2026-07-14? A: FIIs were net sellers of ₹3,062.27 Cr on 2026-07-14.

- Q: What did DII buy on 2026-07-14? A: DIIs were net buyers of ₹2,171.70 Cr on 2026-07-14.

- Q: Is FII buying or selling in July 2026? A: In July 2026, FII flows have shown volatility, with a net sell of ₹532.86 Cr on July 10, a net buy of ₹2,603.72 Cr on July 13, and a significant net sell of ₹3,062.27 Cr on July 14, indicating a cautious stance and responsiveness to global cues.

Stay ahead with real-time institutional flow intelligence. Subscribe to MarketFreeze.com for daily FII/DII data and expert analysis.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 14 July 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.