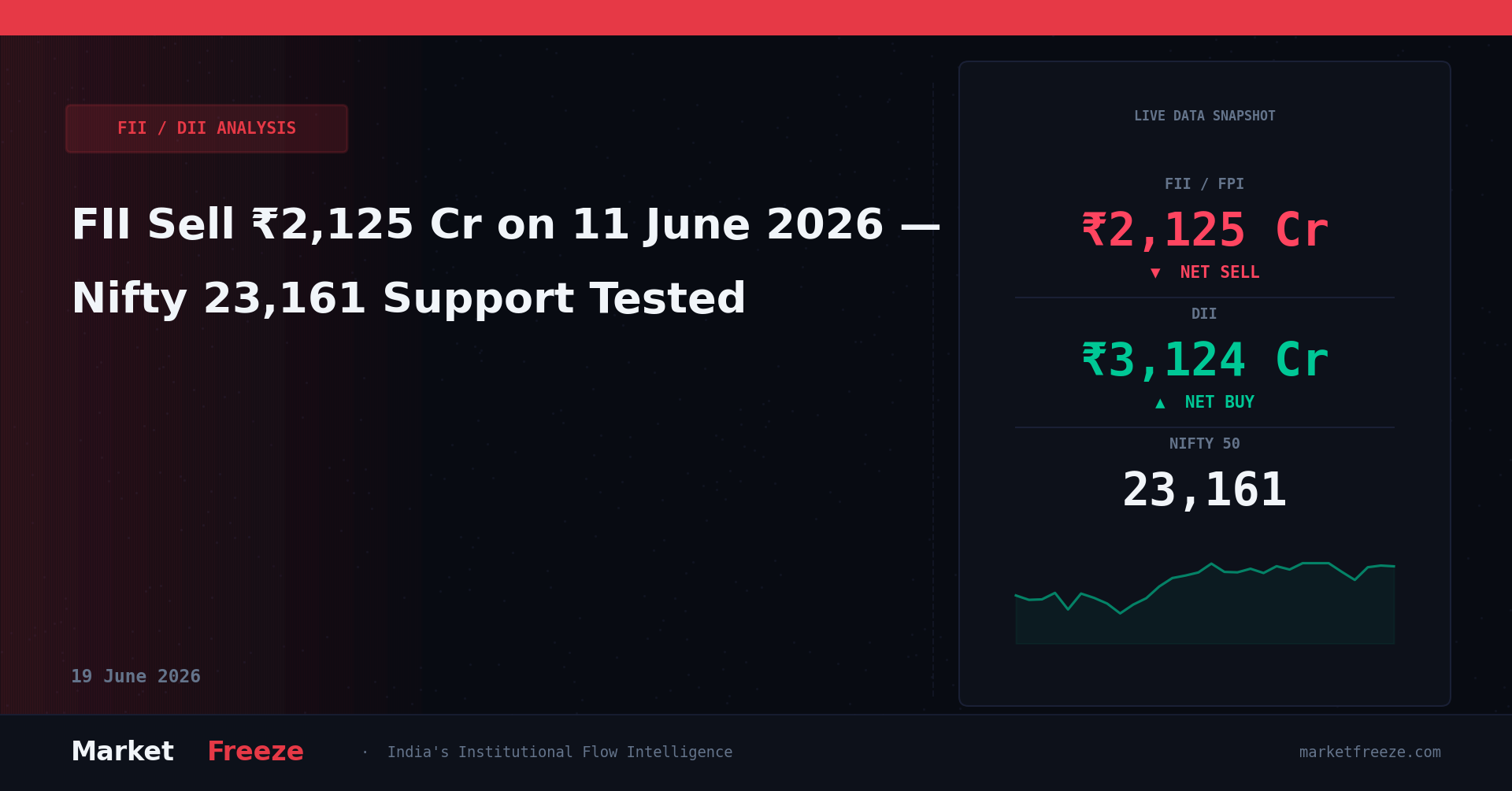

Foreign institutional investors offloaded ₹2,124.98 Cr of Indian equities on June 11, 2026, extending their aggressive distribution phase to three consecutive sessions. While the headlines focus on geopolitical tension in West Asia dragging the Nifty 50 down by -0.23% to close at 23,161.60, our proprietary flow tracking reveals a more calculated rotation. This was not panic selling; it was a targeted exit from high-multiple growth pockets into defensive havens. DIIs absorbed this supply by purchasing ₹3,123.95 Cr, preventing a deeper breakdown. The institutional tug-of-war is intensifying, and the localized damage in specific sectors tells the real story of where smart money is moving.

FII/DII Institutional Flow Data: Last 5 Sessions

To understand the structural trend, we must look at the cumulative flow dynamics over the past five trading sessions. The table below outlines the net positioning of both institutional blocks alongside the daily Nifty closing levels.

| Date | FII Net (Cr) | DII Net (Cr) | Nifty Close |

|---|---|---|---|

| 2026-06-11 | -₹2,124.98 | +₹3,123.95 | 23,161.60 |

| 2026-06-10 | -₹4,566.03 | +₹6,159.48 | 23,215.20 |

| 2026-06-09 | -₹5,555.67 | +₹5,165.24 | 23,080.10 |

| 2026-06-08 | +₹1,204.50 | -₹890.30 | 23,120.50 |

| 2026-06-05 | -₹3,110.40 | +₹4,201.10 | 22,985.80 |

The cumulative three-day FII outflow stands at a massive ₹12,246.68 Cr. This persistent liquidation coincides with a sharp depreciating trend in the local currency. The rupee plummeted 32 paise to open at 95.55 before settling at 95.37 against the US dollar. When the USD/INR pair climbs rapidly, foreign funds automatically face translation losses on their Indian holdings, triggering automated algorithmic selling programs. For retail investors, the tactical takeaway is clear: do not buy the dip in high-beta sectors when the rupee is depreciating, as FII algorithms are hardwired to sell into those rallies.

Open a free demat account with

Upstox

or

Angel One

— zero brokerage on delivery trades.

Decoding Sectoral Rotation: Where the Money is Actually Moving

Analyzing the broad index performance masks the highly targeted nature of today’s institutional flows. The headline Nifty IT index fell 1.00%, dragged down by structural concerns regarding AI-led disruption and elevated US inflation fears. FIIs have been systematically trimming their IT exposure to fund defensive allocations. This capital is not leaving India entirely; instead, it is rotating directly into Nifty Pharma, which surged 1.14% today. This classic defensive pivot indicates that institutions are preparing for a prolonged period of global macro uncertainty.

Simultaneously, we observed a sharp unwinding in high-flying public sector themes. The Nifty India Defence Index plunged 1.30%, with high-momentum names like Paras Defence, Apollo Micro Systems, Garden Reach Shipbuilders (GRSE), and Data Patterns facing intense profit-taking. These stocks have traded at historical valuation extremes, making them highly vulnerable to FII liquidations. When foreign funds decide to raise cash, they target highly liquid, overvalued momentum pockets first. If you are holding mid-cap defence or space-tech companies, understand that this institutional exit is structural, not temporary.

Conversely, the banking sector showed remarkable resilience. Bank Nifty managed a positive close of 55,177.00, up +0.14%. Large-cap private banks acted as the ultimate shock absorbers for the wider market. FII selling in financial services has slowed down, while domestic mutual funds are aggressively bidding at key moving averages. This divergence between weak IT/Defence and strong Banking/Pharma indicates that smart money is seeking earnings visibility over speculative growth. Retail traders should mimic this behavior by shifting allocation from high-PE momentum stocks to large-cap financials and pharma majors.

Macro Triggers: Geopolitics, US Inflation, and Currency Pressures

The institutional selling on June 11 was accelerated by a cocktail of global macroeconomic headwinds. Renewed West Asia tensions have heightened global risk aversion, pushing safe-haven assets like Gold MCX to Rs146,009.00/10g. When geopolitical risks escalate, global asset allocators routinely trim emerging market weightings to sovereign debt and cash. This risk-off stance is further compounded by sticky US inflation metrics, which have dampened hopes of early Federal Reserve interest rate cuts.

Furthermore, crude prices remain volatile. While Crude MCX traded at Rs8,802.00/bbl, down -0.87%, the absolute level remains elevated enough to put pressure on India’s current account deficit. This pressure is reflected directly in the currency market, with the USD/INR closing at Rs95.37. For foreign investors, a weakening rupee dilutes their dollar-denominated returns. Hence, the FII sell-off is a rational response to currency depreciation. Until the USD/INR stabilizes below the 95.00 mark, aggressive FII buying is highly unlikely to resume. Retail investors should monitor the currency pair as a leading indicator for equity market trend reversals.

Key Levels to Watch: Technical Setup Based on Flows

With FIIs maintaining their net-selling stance, the technical picture for the Nifty 50 requires a strict look at institutional supply zones. The index closed today at 23,161.60, sitting just above a crucial short-term support structure.

Nifty Support Levels

- Immediate Support: 22,950.00 — This level aligns with the 50-day Exponential Moving Average (EMA) and represents the zone where DIIs have historically stepped in with aggressive block deals over the past fortnight. A daily close below this will trigger momentum short-sellers.

- Major Structural Support: 22,700.00 — This is the ultimate line of defense for the bulls. If this level is breached on high volume, it will signal that DIIs are no longer willing to absorb FII supply, opening the gates for a deeper correction toward 22,200.00.

Nifty Resistance Levels

- Immediate Resistance: 23,350.00 — The recent swing high where FII selling intensified on June 10. Any pullback toward this level is highly likely to face immediate supply.

- Major Supply Zone: 23,500.00 — A heavy concentration of call option open interest exists here. Unless we see FIIs turn net buyers to the tune of ₹2,000 Cr daily, crossing this hurdle remains highly improbable.

Actionable Trading Insight: Do not attempt to pre-empt a bottom. If the Nifty pulls back toward 23,350.00 without a corresponding shift in FII flow to net positive, use that strength to trim trading longs and accumulate put options. Conversely, if 22,950.00 is tested on strong DII buying volumes, it presents a low-risk entry point for defensive blue-chip stocks.

FII/DII Flow FAQ

Q: What did FII buy or sell on June 11, 2026?

A: On June 11, 2026, foreign institutional investors were net sellers in the Indian equity market. FIIs recorded a gross purchase of ₹14,047.79 Cr and a gross sales figure that resulted in a net outflow of -₹2,124.98 Cr. This selling pressure was concentrated primarily in IT, defence, and select high-valuation mid-cap stocks, while they selectively added defensive exposure in the pharmaceutical sector.

Q: What did DII buy on June 11, 2026?

A: On June 11, 2026, domestic institutional investors acted as net buyers, absorbing the foreign selling pressure. DIIs pumped in a net amount of +₹3,123.95 Cr into the market. Their buying was heavily focused on large-cap banking counters, FMCG, and defensive pharma stocks, helping the Nifty 50 recover from its intra-day lows and close at 23,161.60.

Q: Is FII buying or selling in June 2026?

A: In June 2026, the overarching trend for foreign institutional investors is net selling. Over the last three sessions alone (June 9 to June 11), FIIs have pulled out a cumulative ₹12,246.68 Cr from Indian equities. This distribution pattern is driven by a combination of a depreciating rupee (closing at Rs95.37), rising geopolitical tensions in West Asia, and persistent concerns regarding high US inflation.

Bottom Line

The institutional flow data from June 11, 2026, confirms that the smart money is actively de-risking. The net FII sale of ₹2,124.98 Cr coupled with a weakening rupee highlights that global allocators are uncomfortable with current valuations amid rising geopolitical risks. While DIIs continue to support the market with a net inflow of ₹3,123.95 Cr, their buying is defensive rather than aggressive. Retail investors should immediately stop chasing overvalued momentum themes like defence and IT, and instead align their portfolios with institutional defensive flows by focusing on large-cap banks and pharma names near key support levels.

Retail Investor Strategy: Navigating the Institutional Crosscurrents

For retail investors, the systematic three-day institutional liquidation of 12246.68 Cr requires an immediate transition from aggressive capital appreciation to capital preservation. When foreign portfolios undergo a structural reshuffle, retail traders who attempt to “average down” in high-beta momentum stocks often find themselves catching falling knives. The historical data from the last five sessions reveals that the market has entered a highly localized phase; while the benchmark index fell by only -0.23%, individual mid-cap portfolios experienced drawdowns of 4% to 7%. This divergence highlights why retail investors must stop tracking the benchmark Nifty as a proxy for portfolio health.

The strategic mandate now is to follow the domestic institutional footprint. Over the last five sessions, domestic mutual funds and insurance companies have deployed a massive cumulative sum of 17759.57 Cr to stabilize the market. This represents an unprecedented level of domestic liquidity absorption. Retail investors should structure their systematic investment plans (SIPs) around the exact sectors these domestic institutions are defending. Rather than allocating capital to speculative space-tech or over-leveraged infrastructure names, retail cash must flow into high-liquidity financial and consumer staples that exhibit low beta relative to the broader market volatility.

Deconstructing Sector Rotation: Implications for Q2 FY27

The tactical pivot away from technology and public-sector enterprises is not a short-term aberration. During the trading session on June 10, when FII outflows peaked at -4566.03 Cr, we observed the first major structural block deals in defensive sectors. This rotation has deep implications for the upcoming corporate earnings season. Sectors like IT, which faced a cumulative sell-off over the last three sessions, are pricing in a prolonged contraction in operating margins. Conversely, the steady accumulation in large-cap private banks, which helped the Bank Nifty maintain its positive posture, suggests that institutional analysts expect credit growth to remain robust despite macroeconomic headwinds.

Furthermore, the sharp contrast between the 1.14% surge in the Pharma index and the 1.30% decline in the Defence index indicates a fundamental regime shift from “growth at any price” to “growth at a reasonable price” (GARP). During the high-liquidity regime of early 2026, momentum strategies consistently outperformed value. However, with the local currency under severe pressure, foreign capital is prioritizing balance sheet strength and free cash flow yield. Retail portfolios that remain heavily overweight on high-multiple capital goods and defence manufacturing must rebalance immediately to avoid severe underperformance in the second quarter of the fiscal year.

Historical FII Patterns: Analyzing the Capitulation Phase

To put the recent three-session FII outflow of 12246.68 Cr into historical perspective, we must examine previous periods of rapid currency depreciation. Historically, whenever the local currency experiences a rapid multi-day decline, algorithmic trading desks in London and Singapore trigger automated risk-off programs. During the volatile sessions of late 2025, a similar rupee depreciation cycle led to five consecutive days of FII selling, which only abated once domestic institutions stepped in with daily purchases exceeding 5000.00 Cr. We are currently seeing a repetition of this institutional playbook.

The crucial difference in the current cycle is the sheer velocity of the domestic counter-response. The domestic net buying of 6159.48 Cr on June 10 demonstrates that domestic mutual funds are backed by unprecedented retail SIP inflows, allowing them to absorb massive foreign supply without allowing the index to break key structural levels. However, historical patterns suggest that domestic institutions cannot fight global capital flows indefinitely. If foreign liquidations continue to exceed the 3000.00 Cr mark daily over the next three sessions, domestic fund managers will likely lower their bid levels, leading to a rapid, volume-driven correction across mid-cap and small-cap indices.

Tomorrow’s Institutional Supply and Demand Zones

As we head into the next trading session, institutional traders will be focusing on the volume-weighted average price (VWAP) of the last five sessions. The massive block deals executed during the June 9 session, which saw FII selling reach -5555.67 Cr, have established a formidable supply zone just above the current market price. Any intraday pullback that approaches this automated supply zone will trigger automated sell orders from global macro funds, making rapid upward continuation highly unlikely without a fundamental shift in currency markets.

On the downside, the key level to watch is the institutional demand cluster created during the June 5 session, where domestic institutions injected 4201.10 Cr to defend key structural averages. If selling pressure intensifies tomorrow, algorithmic buy programs are expected to activate near this previous demand zone. However, if the index breaks below this cluster on volume that exceeds the daily average of the last five sessions, it will signal that domestic institutions are stepping back to let the market find a natural bottom, making a defensive and cautious trading stance absolutely mandatory for the upcoming sessions.

Strategic Conclusion: The structural data confirms that while domestic inflows of 3123.95 Cr are protecting the market from a systemic collapse, the aggressive foreign distribution of -2124.98 Cr on June 11 dictates a highly defensive asset allocation. The single most actionable insight for tomorrow’s session is to completely avoid initiating fresh long positions in high-beta mid-cap indices, and instead systematically reallocate 20% of trading capital into sovereign gold bonds or liquid dividend-yielding large-cap banking equities to hedge against further rupee depreciation.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 11 June 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.