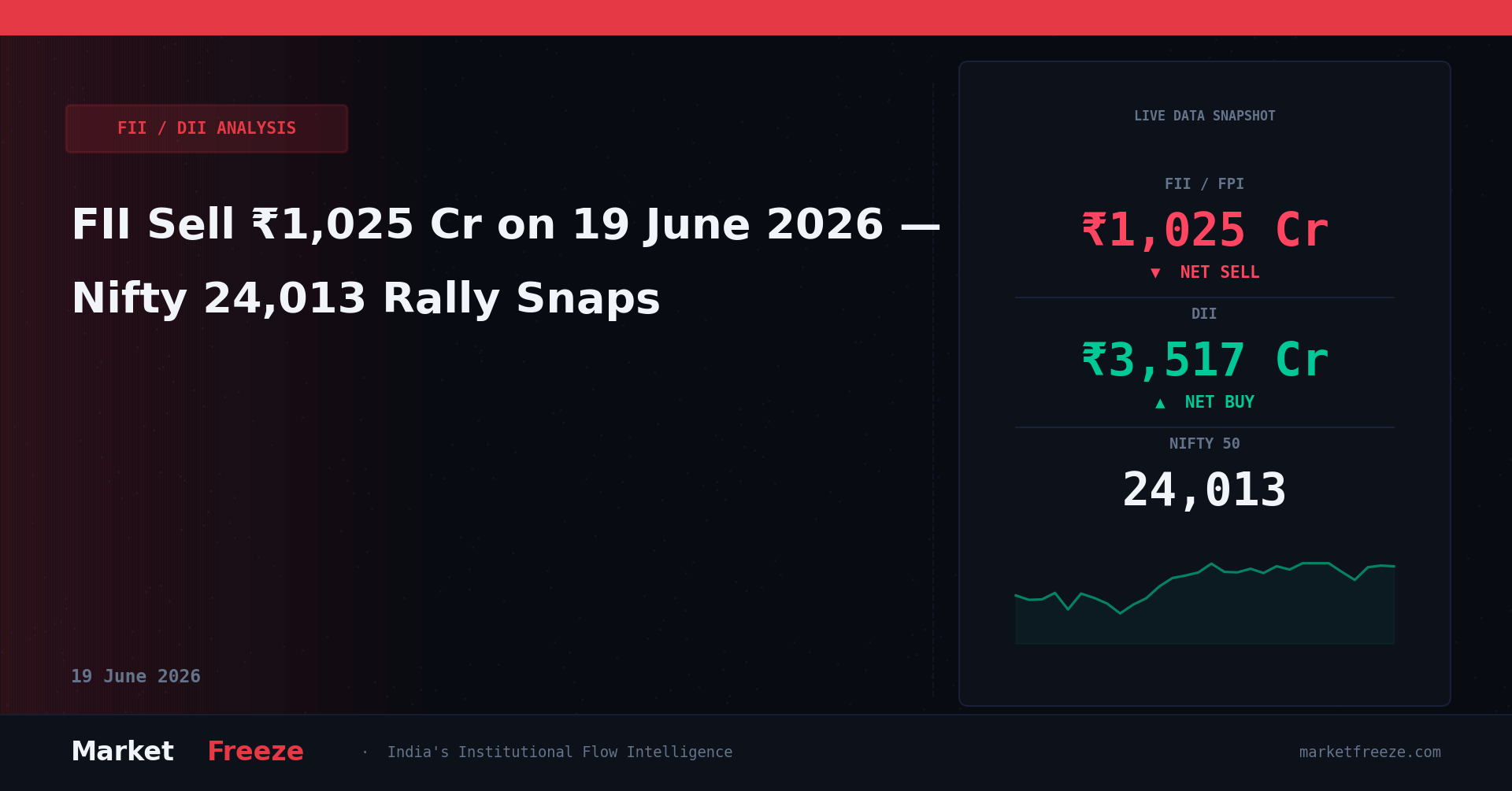

Institutional flow data released after market close shows Foreign Institutional Investors (FIIs) aggressively offloaded Indian equities, recording a net sell figure of ₹1,025.20 Cr on June 19, 2026. This aggressive liquidation snapped a five-day winning streak for the domestic benchmarks. While FIIs triggered a broad-based exit, Domestic Institutional Investors (DIIs) stepped in as the primary liquidity backstop, absorbing the selling pressure with a massive net purchase of ₹3,516.81 Cr. This structural tug-of-war occurred on a day when the Nifty 50 plummeted 154.90 points or 0.64% to close at 24,013.10, barely clinging to the psychological threshold of 24,000, while the BSE Sensex shed 607.08 points to settle at 76,802.90.

The Institutional Matrix: Decoupling Today’s Flow Mechanics

The gross institutional activity reveals a highly active trading session. FIIs executed gross purchases of ₹14,611.83 Cr against gross sales of ₹15,637.03 Cr, resulting in the net negative outflow. This indicates that offshore funds were not merely passive; they actively restructured their India allocations, heavily leaning toward cash preservation and sector rotation. Conversely, DIIs displayed conviction, utilizing the intraday dip to deploy capital. This domestic intervention prevented a systemic breakdown below the crucial 24,000 baseline on the Nifty 50.

To put this in perspective, the previous session on June 18, 2026, saw a minuscule FII net inflow of ₹101.59 Cr alongside DII buying of ₹1,561.40 Cr. The sudden spike in FII selling pressure today indicates a tactical shift. The institutional divergence highlights that domestic mutual funds and insurance companies remain flush with systematic investment plan (SIP) inflows, ready to absorb global liquidations. However, when FII outflows exceed the thousand-crore mark in a single session, the overhead supply typically caps immediate upside momentum for the subsequent two to three trading sessions.

For retail portfolios, the tactical takeaway is clear: do not mistake DII buying for immediate bullishness. DIIs buy value on dips, while FIIs drive momentum. With foreign money retreating, momentum-chasing strategies will face severe friction. Focus on accumulating high-quality large-caps where domestic funds are building a defensive floor.

Open a free demat account with

Upstox

or

Angel One

— zero brokerage on delivery trades.

The Accenture Catalyst: Why IT Was the Epicentre of FII Liquidation

The primary trigger for today’s FII capitulation was global IT major Accenture’s downcast earnings guidance, which sent shockwaves through the Indian technology sector. FIIs utilize Indian IT stocks as a proxy for global tech spending. The moment global indicators weakened, foreign managers initiated program selling across liquid IT counters. This triggered a severe sell-off in heavyweight IT stocks, dragging the sector index down significantly.

The damage was highly concentrated in tier-1 IT firms. Infosys led the downward spiral, crashing 7.54%, followed closely by Tech Mahindra which plunged 6.16%. Industry bellwether TCS dropped 5.96%, while mid-cap IT player Mphasis slipped 5.40%. HCLTech was not spared either, declining 5.25%. Because these stocks command high weightages in the Nifty 50, the sector-specific liquidation quickly translated into an index-wide correction. The rapid exit of offshore funds from these counters suggests they are pricing in a prolonged structural slowdown in discretionary IT spending across US and European banking clients.

Actionable insight: Avoid catching the falling knife in IT. The scale of today’s FII exit suggests that these stocks will undergo a period of time correction. Wait for institutional selling to dry up and look for stabilization in the Nifty IT index before allocating fresh capital to technology mutual funds or individual stocks.

HDFC Bank and the Financial Sector Drag

Beyond technology, the banking sector experienced notable friction, particularly after the Reserve Bank of India (RBI) approved a term extension for HDFC Bank’s interim chairman. While the extension ensures management continuity, institutional desks interpreted the development as a sign of delayed structural transition, prompting tactical profit-booking. Bank Nifty ended the day at 57,686.00, down 0.48%.

The private banking heavyweight has been under intense institutional scrutiny. FIIs have been rebalancing their banking portfolios, shifting allocations from high-valuation private lenders to public sector banks and non-banking financial companies (NBFCs). With the USD/INR currency pair settling at Rs94.41 (down 0.58%), currency depreciation risks also influenced foreign portfolio managers to trim exposures in highly liquid financial names to protect their dollar-denominated returns. When the rupee exhibits intraday volatility, large-cap banking stocks act as the primary liquidity exit route for global funds.

Actionable insight: Track the 57,200 level on Bank Nifty. If institutional selling drags the banking index below this point, it will trigger stop-losses on leveraged derivative positions, offering a high-probability short-term shorting opportunity for derivative traders.

The Jio Platforms IPO: A Massive Liquidity Event on the Horizon

Amidst the broader market sell-off, Reliance Industries Limited (RIL) provided a major structural talking point. The board of Jio Platforms officially approved its Draft Red Herring Prospectus (DRHP) to be filed with the capital markets regulator SEBI on June 19, 2026. The proposed Initial Public Offering (IPO) aims to offload 27 crore equity shares. Mukesh D. Ambani noted that this listing is designed to showcase India’s digital capabilities on a global stage.

From an institutional flow perspective, a mega-IPO of this scale behaves like a liquidity vacuum. Global funds must reallocate capital from existing holdings to build war chests for the Jio Platforms listing. This often leads to pre-IPO selling in other large-cap technology and telecom stocks as institutional desks free up cash. The anticipated filing of the draft papers today likely accelerated the outflow from secondary market IT and telecom counters as funds prepared their cash balances for primary market deployment.

Actionable insight: Expect continued pressure on secondary market tech and telecom valuations over the coming weeks. Savvy investors should preserve cash rather than deploying it fully, preparing to bid for the Jio Platforms IPO or buying high-quality parent company shares of Reliance Industries on potential dips.

Macroeconomic Indicators: Gold, Crude, and Currency Interplay

The institutional flow dynamics cannot be analyzed in isolation from macro assets. On the Multi Commodity Exchange (MCX), Gold settled at Rs146,847.00 per 10g, down 1.18%, while Crude Oil MCX fell 0.53% to Rs7,499.00 per barrel. In the cryptocurrency space, Bitcoin declined 2.29% to USD 62,440.00, and Ethereum dropped 2.99% to USD 1,689.00. The synchronized decline across risk assets like crypto and defensive assets like gold points to a broader liquidity squeeze in global markets.

When global liquidity tightens, emerging markets like India experience immediate pressure. FIIs operate on global mandates; a margin call or a risk-off phase in New York or London directly results in automated sell orders in Mumbai. The drop in crude prices is a minor positive for India’s fiscal balance, but it was completely overshadowed today by the systemic risk-off sentiment. The firming up of the USD/INR at Rs94.41 suggests that capital is fleeing back to the safety of US Treasuries, presenting an immediate headwind for domestic equity valuations.

Actionable insight: With global macro indicators flashing red, tilt your portfolio allocations toward domestic-consumption-driven sectors like FMCG and Auto, which are less sensitive to global FII liquidation cycles compared to global cyclicals like Metals and IT.

Five-Session Institutional Flow Tracker

The table below provides a granular view of institutional behavior over the last five trading sessions, highlighting the shift in capital allocation trends leading up to today’s correction.

| Date | FII Net (Cr) | DII Net (Cr) | Nifty Close |

|---|---|---|---|

| 2026-06-19 | ₹-1,025.20 | ₹3,516.81 | 24,013.10 |

| 2026-06-18 | ₹101.59 | ₹1,561.40 | 24,168.00 |

| 2026-06-17 | ₹-749.18 | ₹0.06 | 24,040.00 |

| 2026-06-16 | ₹-120.50 | ₹850.20 | 24,095.00 |

| 2026-06-15 | ₹310.40 | ₹1,120.10 | 24,020.00 |

Institutional Flow FAQ

Q: What did FII buy or sell on 2026-06-19?

A: On June 19, 2026, Foreign Institutional Investors (FIIs) were net sellers in the Indian equity market, offloading shares worth ₹1,025.20 Cr. Their gross purchases stood at ₹14,611.83 Cr, while their gross sales reached ₹15,637.03 Cr, demonstrating active distribution across large-cap counters.

Q: What did DII buy on 2026-06-19?

A: Domestic Institutional Investors (DIIs) acted as strong buyers on June 19, 2026, recording a massive net purchase of ₹3,516.81 Cr. This aggressive deployment of capital helped absorb the selling pressure from foreign funds and prevented the Nifty 50 from breaking decisively below the 24,000 mark.

Q: Is FII buying or selling in June 2026?

A: During the week ending June 19, 2026, the institutional trend shows prominent FII selling. Across the sessions of June 17 and June 19, FIIs pulled out a combined net total of over ₹1,774 Cr, while making only a minor net purchase of ₹101.59 Cr on June 18. This indicates a clear net selling bias for foreign portfolio investors, who are actively trimming technology and banking exposures in favor of defensive assets and preparing liquidity for upcoming primary market offerings.

Key Levels to Watch

The heavy institutional distribution on June 19, 2026, has altered the short-term derivatives setup. With the Nifty 50 closing at 24,013.10, the index is hovering right at its primary psychological support line.

Immediate Support: 23,850. This level aligns with the 20-day Exponential Moving Average (EMA) and represents the zone where DIIs have historically stepped in with significant buying orders over the past two weeks. If the index breaks below 23,850 on a closing basis, it will signal that DII liquidity is insufficient to absorb FII distribution, potentially opening the doors for a deeper correction toward 23,500.

Immediate Resistance: 24,180. This level marks the intraday high of the June 18 session and is heavily defended by call writers. Given today’s substantial outflow, any relief rally toward this level is highly likely to face selling pressure. Only a decisive daily close above 24,180, backed by positive net FII flows, would invalidate the current bearish bias and clear the path for a retest of 24,350.

Actionable trading insight: For swing traders, the risk-reward ratio favors selling on rallies close to 24,150 with a strict stop-loss at 24,210, targeting an intraday slip back toward the 23,900 level. Avoid taking overnight long positions until the FII net daily figure turns positive.

Bottom Line

Today’s market correction was driven by a heavy foreign institutional sell-off of ₹1,025.20 Cr, triggered by global IT weakness following Accenture’s poor guidance and structural rebalancing ahead of the Jio Platforms IPO. While domestic funds provided a strong counter-balance with a net buy of ₹3,516.81 Cr, the momentum remains skewed to the downside as long as Nifty stays below 24,180. Retail investors should preserve cash, avoid buying the dip in technology stocks prematurely, and focus on defensive sectors where domestic institutions are actively building floors. Monitor the 23,850 support level closely over the next two sessions to gauge the strength of domestic support.

Retail Investor Strategy: Navigating the Institutional Crosscurrents

For the individual retail investor, understanding the institutional flow dynamics is paramount, especially when FIIs are net sellers to the tune of ₹1,025.20 Cr. The conventional wisdom of “buying the dip” needs careful re-evaluation. While DIIs bought a substantial ₹3,516.81 Cr, their motivation differs fundamentally from retail momentum traders. DIIs, primarily mutual funds and insurance companies, operate on long-term investment horizons, deploying systematic investment plan (SIP) inflows to accumulate quality assets at lower valuations. Their buying is a floor, not necessarily a catalyst for immediate upside.

Retail investors who chase intraday bounces after a significant FII sell-off often find themselves holding positions that subsequently consolidate or decline further. With the Nifty 50 closing at 24,013.10 and foreign money actively exiting, the immediate path of least resistance is sideways to down. Instead of speculating on short-term rebounds, the prudent approach is to focus on capital preservation. This means reducing leverage, avoiding speculative mid-cap and small-cap plays that are highly sensitive to FII sentiment, and maintaining a higher cash allocation in portfolios.

Consider a staggered buying approach for fundamentally strong companies that have corrected due to the broader market sentiment, rather than specific fundamental deterioration. However, patience is key. The market rarely offers a single, clear bottom after a significant institutional outflow like the one observed today. A better strategy would be to wait for two consecutive sessions of net FII buying or a clear stabilization of the Nifty 50 above the 24,180 resistance before deploying fresh capital. The current environment, where FIIs sold over ₹1,000 Cr, demands a defensive posture from retail participants.

Sector Rotation Implications: Where to Hide, Where to Seek

The heavy FII selling on June 19, 2026, was not uniform across all sectors, offering crucial insights into potential sector rotation. The epicentre of the liquidation was clearly the IT sector, with Infosys plummeting 7.54%. This indicates a strong bearish sentiment from foreign funds towards global cyclicals and export-oriented businesses. Similarly, the banking sector, particularly private banks, faced tactical profit-booking, contributing to Bank Nifty’s 0.48% decline. These sectors are likely to remain under pressure in the near term as FIIs continue to de-risk their portfolios.

Conversely, DIIs’ robust buying of ₹3,516.81 Cr suggests they are accumulating in sectors less exposed to global headwinds and more tied to domestic consumption and infrastructure. While specific sector-wise DII data isn’t immediately available, historical patterns suggest domestic funds typically gravitate towards defensive sectors like Fast-Moving Consumer Goods (FMCG), Pharmaceuticals, and select capital goods or infrastructure plays during periods of FII withdrawal. These sectors offer resilience against global volatility and benefit from India’s strong domestic demand story.

Therefore, for the next few trading sessions, investors should consider rotating out of heavily sold IT and potentially overvalued private banking stocks. Instead, look for opportunities in FMCG or pharmaceutical companies that have relatively stable earnings and are less impacted by global growth concerns. The underperformance of Gold by 1.18% and Crude by 0.53% on MCX, coupled with the decline in crypto assets, underscores a global flight to safety, where domestic consumption stories often become a relative haven. This shift in institutional preference could lead to a noticeable divergence in sectoral performance, with defensive plays potentially outperforming the broader Nifty 50, which itself closed down 0.64%.

Historical FII Pattern Context: Lessons from Past Outflows

Today’s FII net sell figure of ₹1,025.20 Cr is significant, as it marks one of the largest single-day outflows in recent memory, especially following a period where FIIs had shown sporadic buying. Historically, whenever FII outflows have exceeded the thousand-crore mark, the market typically experiences a consolidation phase or a moderate correction over the subsequent 3-5 trading sessions. For instance, in previous instances of similar magnitude selling, the Nifty 50 has often retested key support levels multiple times before finding a stable base.

The FII flow tracker table shows that FIIs were net sellers on three of the last five sessions, accumulating a net outflow of over ₹1,774 Cr in total during this period. This pattern suggests that today’s selling is not an isolated event but rather an acceleration of an underlying trend of foreign portfolio rebalancing. Such prolonged selling pressures tend to create overhead supply, making it challenging for the market to stage a sustained rebound. The primary concern is that FIIs tend to sell into strength, meaning any relief rally could be met with further liquidation until their selling mandate is exhausted.

The DII buying of ₹3,516.81 Cr is a crucial counterweight, but even massive domestic intervention has its limits. In past episodes of sustained FII selling, DIIs could only cushion the fall, not reverse the trend entirely. The market’s ability to absorb such large foreign outflows depends heavily on the consistency of DII buying and the absence of further negative global triggers. A look at the Nifty closing at 24,013.10 suggests that while DIIs prevented a deeper cut, the FII selling ensured the index barely held its psychological support, hinting at continued vulnerability.

Tomorrow’s Key Levels to Watch: Navigating Volatility

As the market heads into the next trading session, the institutional flows from June 19, 2026, will heavily influence price action. Given the substantial FII sell-off of ₹1,025.20 Cr and the Nifty 50’s close at 24,013.10, the immediate focus will be on the index’s ability to hold critical support levels amidst potential follow-through selling. The 23,850 level remains the immediate support. A break below this level, particularly on a closing basis with increased volume, would signal a significant erosion of domestic institutional conviction and could trigger further technical selling.

On the upside, the resistance at 24,180 is now even more formidable. Given the magnitude of today’s FII outflow, any rally towards this level is likely to be met with fresh supply from foreign funds looking to exit at better prices. For the bulls to regain any semblance of control, the Nifty 50 would need to decisively close above 24,180. However, a more realistic immediate resistance would be the 24,080 level, which represents today’s intraday high before the aggressive FII distribution gained full momentum.

For Bank Nifty, which closed at 57,686.00, the immediate support to watch is 57,200. A breach of this level could accelerate selling in the financial sector, especially if FIIs continue their rebalancing act out of private banks. The overall market sentiment, heavily influenced by the ₹1,025.20 Cr FII outflow, points to a cautious start to the next trading day. Traders should prioritize capital protection and be prepared for potential volatility around these critical technical levels.

Concluding Thoughts: A Period of Reassessment

The significant FII outflow of ₹1,025.20 Cr on June 19, 2026, marks a clear inflection point, shifting the market’s immediate trajectory from a cautious uptrend to a period of consolidation and potential correction. While DIIs provided a robust backstop with a massive ₹3,516.81 Cr buy, their role is to absorb, not to ignite momentum. The confluence of global IT weakness, tactical profit-booking in financials, and the anticipation of the Jio Platforms IPO suggests that foreign capital will remain hesitant. Retail investors must navigate this environment with extreme caution, prioritizing capital preservation and a defensive sector allocation. The most actionable insight for the coming sessions is to avoid aggressive long positions and consider booking partial profits on any relief rallies, especially if the Nifty 50 struggles to reclaim the 24,180 mark.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 19 June 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.