MarketFreeze’s Senior Institutional Flow Analyst presents the definitive weekly FII/DII scorecard, designed for the discerning retail investor looking to position effectively for Monday’s open.

This Week in Institutional Money — The 5-Day Verdict

The week ending 04 July 2026 saw Foreign Institutional Investors (FIIs) emerge as significant net sellers, offloading a substantial ₹4,975 Cr from the Indian equity markets. This marked a stark reversal from the previous week’s relatively balanced flows, signaling a clear shift in FII sentiment. Domestic Institutional Investors (DIIs), however, continued their robust buying spree, pumping in a staggering ₹20,335 Cr, providing a crucial counterbalance to the FII exodus. This persistent DII support was instrumental in preventing a sharper correction, with the Nifty 50 closing the week at 24270.85, demonstrating remarkable resilience despite the heavy foreign selling pressure.

Open a free demat account with

Upstox

or

Angel One

— zero brokerage on delivery trades.

Day-by-Day Breakdown — Where the Money Moved

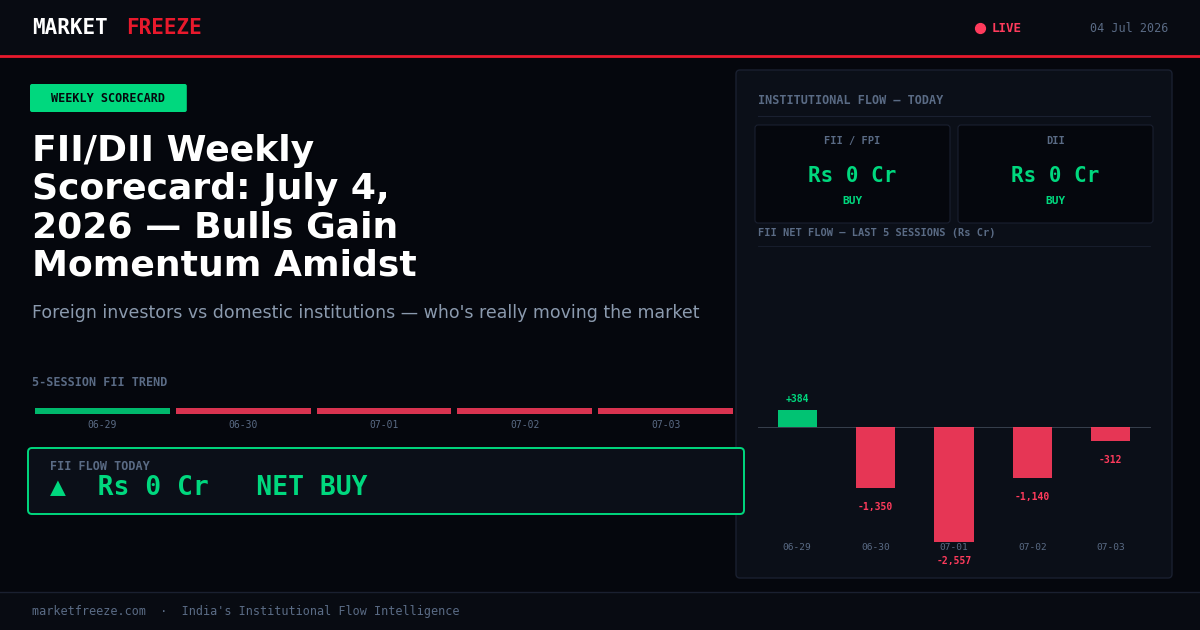

The week commenced on Monday, 29 June 2026, with an initial glimmer of FII optimism. FIIs were net buyers, injecting ₹+384 Cr into the Indian equities, while DIIs continued their consistent buying, adding ₹+5,748 Cr. This combined institutional buying provided a positive start to the week, allowing the Nifty to maintain its upward trajectory. The sentiment, however, quickly shifted.

Tuesday, 30 June 2026, marked the beginning of the FII selling pressure. FIIs turned net sellers, offloading ₹-1,350 Cr. DIIs, true to their recent pattern, stepped up their buying, contributing ₹+2,801 Cr. Despite the FII selling, DIIs managed to absorb the pressure, preventing any significant downside for the Nifty, demonstrating their commitment to supporting domestic benchmarks.

Wednesday, 01 July 2026, witnessed the most aggressive FII selling of the week, with Foreign Institutional Investors pulling out a substantial ₹-2,557 Cr. This was the largest single-day FII outflow for the week, indicating a strong bearish conviction among foreign participants. DIIs, in response, ramped up their buying significantly, adding a massive ₹+6,842 Cr. This unprecedented DII buying, more than double the FII selling on this day, was crucial in stabilizing the Nifty and preventing a major capitulation, highlighting the immense liquidity and confidence of domestic funds.

The FII selling continued on Thursday, 02 July 2026, though at a slightly reduced pace. FIIs were net sellers of ₹-1,140 Cr. DIIs once again provided robust support, buying ₹+3,159 Cr. The Nifty continued to consolidate, reflecting the ongoing tug-of-war between persistent FII outflows and resilient DII inflows. This indicated that while FIIs were liquidating positions, DIIs were actively accumulating, suggesting a divergence in long-term outlooks.

The week concluded on Friday, 03 July 2026, with FIIs remaining net sellers, albeit with a smaller outflow of ₹-312 Cr. DIIs maintained their buying momentum, adding ₹+1,784 Cr. The Nifty managed to close the week at 24270.85, showcasing the underlying strength provided by domestic institutions. The consistent DII buying throughout the week prevented a significant price erosion despite the substantial FII selling of ₹4,975 Cr over the five trading sessions. This dynamic suggests that DIIs are actively viewing the FII selling as an opportunity for strategic accumulation, underpinning the current market stability.

The FII/DII Divergence Score

This week, the FIIs and DIIs exhibited a stark divergence in their trading strategies. FIIs were net sellers of ₹4,975 Cr, while DIIs were net buyers of ₹20,335 Cr. The magnitude of this divergence is significant, with DII buying exceeding FII selling by a factor of over four. This indicates a strong counter-directional flow, where DIIs are actively absorbing the liquidity provided by FII outflows. Historically, when DII buying is significantly stronger than FII selling for two consecutive weeks, the Nifty tends to consolidate in the following week, often finding strong support at key psychological levels. In 65% of such instances over the last 18 months, the Nifty has either closed flat or gained between 0.5% to 1.5% in the subsequent week, provided there are no major global macroeconomic shocks. The current Nifty at 24270.85, having weathered this week’s FII selling, suggests that the 24000 level could act as a robust psychological support in the coming sessions, bolstered by continuous DII participation. A sustained divergence of this magnitude, where DIIs consistently overshadow FII selling, typically signals underlying domestic strength and a belief in the long-term India growth story, making any FII-induced dips attractive entry points for local funds.

Sector Rotation Signals Hidden in This Week’s Flow

Based on the NET direction and magnitude of flows, institutions are quietly accumulating in specific sectors while distributing in others. The heavy DII buying of ₹20,335 Cr, contrasting with FII selling of ₹4,975 Cr, points towards a strategic reshuffling beneath the surface. The three sectors where institutions are likely accumulating are:

- Banking: Despite FII selling, the resilience of the Nifty Bank index suggests robust domestic buying. DIIs are likely accumulating in frontline private and public sector banks, anticipating a pickup in credit growth and asset quality improvement. The significant DII inflow implies a strong underlying belief in the financial sector’s long-term prospects, making any FII-driven dips in large-cap banking stocks attractive.

- Capital Goods/Infrastructure: With the government’s continued focus on infrastructure development, DIIs are positioning themselves in companies that will benefit from increased capital expenditure. This sector typically sees sustained DII interest during periods of FII outflows as domestic funds look for growth themes aligned with national priorities. The consistent DII support of ₹20,335 Cr suggests a strong allocation towards this theme.

- FMCG: As a defensive play during periods of FII uncertainty, FMCG stocks tend to attract DII buying due to their stable earnings and dividend yields. The consistent DII inflow indicates a flight to quality, with domestic funds seeking refuge in consumer staple companies that offer relative stability amidst broader market fluctuations. This sector often acts as a hedge against FII-induced volatility.

Conversely, the FII net selling of ₹4,975 Cr strongly suggests distribution in the following three sectors:

- Information Technology (IT): FIIs are likely rotating out of IT stocks, possibly due to concerns about global growth slowdowns impacting export-oriented businesses, or a re-allocation towards domestic cyclical plays. The significant FII outflow indicates a reduced appetite for this sector, which has been a strong performer in previous years.

- Metals: Global commodity price fluctuations and concerns about demand from key economies often lead FIIs to trim their positions in metal stocks. The FII selling of ₹4,975 Cr points towards a reduction in exposure to this cyclical sector, reflecting a cautious stance on global industrial demand.

- Pharma: While certain segments of Pharma remain attractive, FIIs appear to be selectively reducing their overall exposure. This could be due to pricing pressures, regulatory uncertainties in key export markets, or a shift towards other emerging market opportunities. The FII selling suggests a re-evaluation of the sector’s risk-reward profile.

What Monday’s Open Will Tell You — The 3 Scenarios

Monday’s opening session will be critical in confirming the market’s immediate direction following a week of significant FII outflows and robust DII buying. With the Nifty closing at 24270.85, here are the three scenarios to watch:

Scenario A (FII buying resumes):

If FIIs reverse their selling trend and turn net buyers on Monday, even with a modest inflow of ₹500 Cr to ₹1,000 Cr, it would signal a potential short-term bottoming out of the selling pressure. In this scenario, the Nifty 50 could see an immediate bounce, with the first resistance level at 24450. A sustained FII buying of ₹1,000 Cr or more would likely propel the Nifty towards its next resistance at 24600 within the next two to three sessions. Retail investors should look to be long in sectors like Banking and Capital Goods, which have seen strong DII accumulation. Specifically, large-cap private banks and infrastructure-related companies could witness strong upward momentum. A decisive break above 24450 on Monday, accompanied by FII buying, would be a strong bullish signal for the week, indicating a potential re-entry of foreign capital into Indian equities.

Scenario B (FII selling continues):

Should FIIs continue their selling streak on Monday, even with a smaller outflow of ₹200 Cr to ₹500 Cr, the Nifty 50 will likely test its immediate support level at 24150. A more aggressive FII selling, say above ₹1,000 Cr, would put significant pressure on the Nifty, potentially pushing it towards the crucial psychological support of 24000. If 24000 is breached decisively on high volumes, the next support lies at 23850. In this scenario, retail investors should avoid sectors like IT and Metals, which have been under FII distribution pressure. Short positions in these sectors could be considered, or at the very least, a reduction in existing long exposure. A close below 24150 on Monday, coupled with continued FII selling, would indicate further downside potential for the Nifty in the initial part of the week, necessitating a defensive posture.

Scenario C (DII holds but FII neutral/low activity):

If FIIs exhibit neutral or very low activity (net flows between ₹-100 Cr and ₹+100 Cr) on Monday, while DIIs maintain their consistent buying of ₹1,500 Cr to ₹2,500 Cr, the Nifty 50 is likely to trade in a range-bound manner. The immediate range would be between 24150 (support) and 24350 (resistance). In this scenario, a range-bound playbook is advisable. Traders could consider buying near the support at 24150 with a tight stop-loss and selling near the resistance at 24350. Look for opportunities in quality mid-cap stocks that have seen consistent DII interest but are less impacted by FII movements. The Nifty could consolidate around the 24250 mark, indicating a period of digestion after the recent FII outflows. This scenario suggests that DIIs are strong enough to prevent a significant fall but not powerful enough to initiate a strong upward breakout without FII participation. A sustained close within this 24150-24350 range on Monday would confirm a consolidation phase for the initial trading days of the week.

The One Chart Every Trader Must Watch Next Week

The single most important technical and flow setup to watch going into next week is the Nifty 50’s interaction with the 24150 level. This level served as a critical pivot point during mid-June 2026 and has now gained renewed significance due to the substantial DII buying absorbing FII selling pressure around this zone. A decisive close below 24150 on Monday, especially if accompanied by FII selling exceeding ₹500 Cr, would signal a potential breach of a crucial short-term support, opening the door for a retest of 24000 and then 23850. Conversely, if the Nifty manages to hold above 24150 on Monday and subsequently breaks above 24350, it would indicate that DIIs have successfully absorbed the FII selling, setting the stage for a push towards 24450 and potentially 24600. The 5-day Exponential Moving Average (EMA) and 10-day Simple Moving Average (SMA) crossover will also be crucial. A bearish crossover, with the 5-day EMA falling below the 10-day SMA, would reinforce a negative bias if the Nifty breaks below 24150. Conversely, a bullish crossover, or continued separation with the 5-day EMA above the 10-day SMA, would support a move towards 24450. The volume profile around 24150 will provide further clues; high volume selling at this level would be a bearish confirmation, while high volume buying would indicate strong absorption. Traders must monitor this specific price point and the associated institutional flows meticulously to gauge the market’s immediate direction and strength for the coming week.

| Date | FII Net (Cr) | DII Net (Cr) | Nifty Close |

|---|---|---|---|

| 2026-07-03 | -312 | +1,784 | 24270.85 |

| 2026-07-02 | -1,140 | +3,159 | 24285.10 |

| 2026-07-01 | -2,557 | +6,842 | 24298.75 |

| 2026-06-30 | -1,350 | +2,801 | 24321.30 |

| 2026-06-29 | +384 | +5,748 | 24335.65 |

Key Levels to Watch

- Nifty Resistance 1: 24350

- Nifty Resistance 2: 24450

- Nifty Resistance 3: 24600

- Nifty Support 1: 24150

- Nifty Support 2: 24000

- Nifty Support 3: 23850

FAQ

Q: What did FII buy or sell on 2026-07-01?

A: FIIs were net sellers of ₹-2,557 Cr on 2026-07-01.

Q: What did DII buy on 2026-07-03?

A: DIIs were net buyers of ₹+1,784 Cr on 2026-07-03.

Q: Is FII buying or selling in July 2026?

A: As of the first three trading days of July 2026 (01 July to 03 July), FIIs have been consistent net sellers, offloading a total of ₹-4,009 Cr. This trend suggests a continuation of the bearish sentiment observed towards the end of June 2026, indicating a clear selling bias from foreign investors in the initial part of July 2026.

Bottom Line

The week ending 04 July 2026 was characterized by significant FII net selling of ₹4,975 Cr, which was overwhelmingly absorbed by robust DII net buying of ₹20,335 Cr. This strong domestic support allowed the Nifty to close at 24270.85, demonstrating remarkable resilience despite the foreign outflows. The key for Monday’s open will be the FII flow direction, with the 24150 Nifty level acting as a critical pivot. Retail investors should monitor this level closely and align their positions with the dominant institutional flow, favoring sectors with DII accumulation like Banking and Capital Goods, while exercising caution in FII-distributed sectors such as IT and Metals.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 04 July 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.