MarketFreeze.com Exclusive

Oil Price Dip & RBI Boost Drive Nifty to 23,242.1 — FIIs Net Sell ₹5,555.67 Cr Today

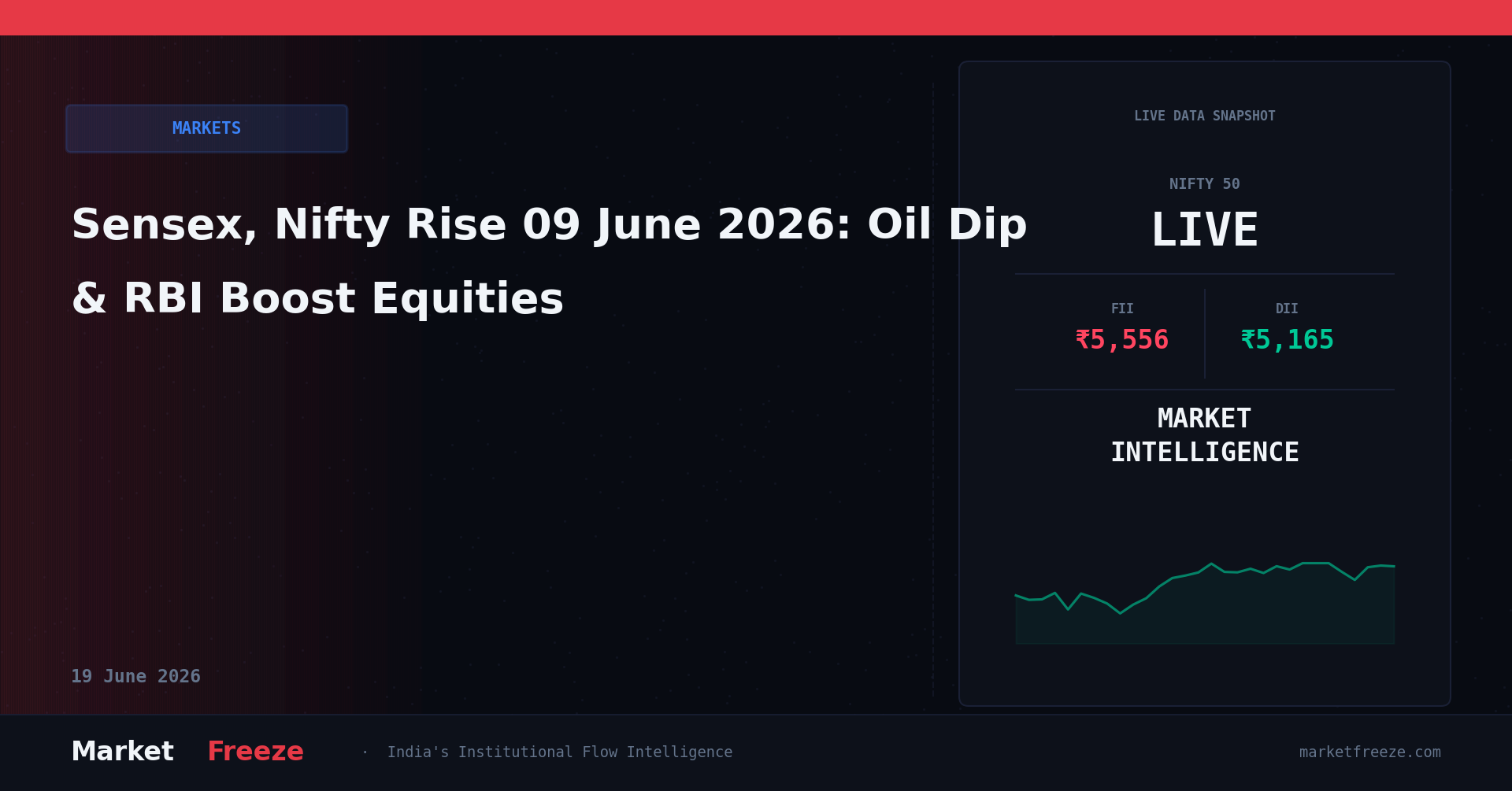

Indian equities closed higher today, with the Nifty 50 gaining 0.52% to settle at 23,242.10 and the Sensex rising 0.54% to 73,919.00, buoyed by declining crude oil prices amid an Iran-Israel conflict pause and an RBI liquidity boost for lenders; however, this upside occurred against a backdrop of continued FII net selling of ₹5,555.67 Cr, countered by robust DII net buying of ₹5,165.24 Cr, indicating a persistent institutional divergence. The Bank Nifty notably outperformed, surging 2.09% to 55,194.00, reflecting the positive sentiment in the banking sector following the central bank’s actions. This move above the 23,200 mark for the Nifty, despite significant FII outflows, highlights the domestic institutional strength underpinning the current market rally, especially in banking-heavy indices. The decline in Crude MCX by -1.87% to ₹8,855.00/bbl provided a macro tailwind, easing inflation concerns and improving margins for several sectors, yet the consistent FII divestment suggests a cautious global outlook on Indian valuations. The USD/INR also saw an uptick, rising 0.41% to ₹95.74, potentially adding to FII repatriation costs and influencing their selling behavior.

What FIIs and DIIs Actually Did — The Flow Data Behind Today’s Move

Today, 2026-06-09, Foreign Institutional Investors (FIIs) were net sellers for the third consecutive session, offloading equities worth ₹5,555.67 Cr. This substantial outflow follows two previous sessions of significant selling: ₹8,776.25 Cr on 2026-06-08 and ₹4,447.06 Cr on 2026-06-05. Cumulatively, over the last three trading sessions, FIIs have divested a staggering ₹18,778.98 Cr from the Indian equity markets. This consistent and heavy selling by FIIs directly contradicts the headline indices’ marginal gains and the strong performance of broader markets. The persistent FII outflow, particularly at a time when the Nifty 50 closed above 23,200 and the Bank Nifty surged 2.09%, suggests that foreign capital is not participating in this specific leg of the rally, likely due to global macro concerns and rising US bond yields impacting emerging market attractiveness. This scale of FII selling historically indicates a flight to safety or reallocation to other markets, often preceding periods of consolidation or corrective moves in the benchmark indices if sustained over a longer horizon. The fact that the USD/INR strengthened by 0.41% to ₹95.74 today could also be a factor, as a depreciating rupee makes FII returns in dollar terms less attractive and may incentivize further repatriation.

In stark contrast, Domestic Institutional Investors (DIIs) provided robust support, absorbing a significant portion of the FII selling. Today, 2026-06-09, DIIs were net buyers of ₹5,165.24 Cr. This buying spree is consistent with their activity in previous sessions: ₹9,133.57 Cr on 2026-06-08 and ₹4,360.14 Cr on 2026-06-05. Over the last three sessions, DIIs have pumped a remarkable total of ₹18,658.95 Cr into the market. This near-perfect offset of FII selling by DII buying, with DIIs buying ₹18,658.95 Cr against FIIs selling ₹18,778.98 Cr over the last three sessions, is the primary reason the Nifty 50 could sustain itself above 23,200 and the Sensex could register gains. The strong DII buying, particularly in the banking sector which saw the Bank Nifty jump 2.09% to 55,194.00, suggests confidence in domestic growth narratives and the specific impact of the RBI’s liquidity boost. DIIs appear to be strategically accumulating quality Indian assets at current valuations, effectively providing a strong floor to the market amidst foreign investor apprehension. This pattern of DII resilience in the face of FII outflows implies a rotation from foreign-favoured large-caps to domestically-favoured segments, potentially mid-caps and small-caps, where DIIs often find better value.

Sector-by-Sector Impact on NSE — Who Wins, Who Loses

- Banking (Bank Nifty at 55,194.00): The banking sector was the clear winner today, with the Bank Nifty surging by 2.09% to close at 55,194.00. This strong performance was directly driven by the RBI’s detailed concessional forex liquidity boost and easing West Asia tensions. The significant DII net buying of ₹5,165.24 Cr today, contributing to ₹18,658.95 Cr over three sessions, strongly suggests DIIs are actively accumulating banking stocks, viewing them as beneficiaries of improved liquidity and economic stability. The declining Crude MCX price at ₹8,855.00/bbl also reduces inflationary pressures, which is positive for lending growth and asset quality.

- IT: The IT sector, heavily reliant on export revenues, faces headwinds from the strengthening USD/INR at ₹95.74, which rose 0.41% today. While a higher USD/INR typically aids IT exporters, sustained FII net selling of ₹5,555.67 Cr, coupled with global macro concerns, implies that foreign investors may be trimming positions in growth-oriented sectors like IT, especially given the broad FII outflow of ₹18,778.98 Cr over three sessions. The sector’s sensitivity to global growth and FII sentiment means it could underperform despite a favorable currency movement.

- FMCG: The FMCG sector, often considered a defensive play, could see mixed impacts. The decline in Crude MCX to ₹8,855.00/bbl is beneficial as it reduces input costs for packaging and transportation, improving margins. However, the consistent FII outflows of ₹5,555.67 Cr today and ₹18,778.98 Cr over three sessions indicate foreign investors are not seeking safety in Indian defensives at this juncture. DII buying could provide some support, but the sector’s performance will depend on domestic consumption resilience against broader FII-driven market caution.

- Auto: The auto sector benefits from the declining Crude MCX price at ₹8,855.00/bbl, which lowers fuel costs for consumers and reduces freight expenses for manufacturers, potentially boosting sales and margins. However, the overarching FII net selling of ₹5,555.67 Cr today suggests a cautious stance from foreign investors towards cyclical sectors. DII buying, particularly in broader markets that outperformed, might be selectively flowing into auto ancillaries or specific OEM plays, but the sector’s overall resilience will be tested by the sustained FII withdrawal.

- Metal: The metal sector is highly sensitive to global demand and commodity prices. While declining crude oil prices can improve manufacturing costs, the persistent FII net selling of ₹18,778.98 Cr over three sessions, coupled with global macro concerns, suggests foreign investors are likely reducing exposure to cyclicals like metals. The sector may face headwinds if global demand outlooks remain fragile, despite domestic DII support.

- Pharma: The pharma sector, often seen as defensive and less correlated with domestic economic cycles, could experience relative stability. However, the strengthening USD/INR to ₹95.74, while generally favorable for export-oriented pharma companies, might not fully offset the impact of broad FII outflows of ₹18,778.98 Cr. FIIs looking to reduce overall India exposure might not spare even defensive sectors, making DII buying crucial for its performance.

Nifty Levels That Matter — Support, Resistance, and the FII Footprint

The Nifty 50 closed at 23,242.10 today, marking a gain of 0.52% and firmly closing above the critical psychological level of 23,200. This upward movement, despite significant FII net selling of ₹5,555.67 Cr, was primarily propelled by sustained DII buying of ₹5,165.24 Cr and strong performance in specific sectors like banking, with the Bank Nifty up 2.09% at 55,194.00. The FII footprint over the last three sessions, where they sold ₹18,778.98 Cr, indicates a significant level of supply in the market, which DIIs have successfully absorbed.

Considering the current Nifty level of 23,242.10, the immediate resistance lies around 23,500. This level represents a point where FII selling pressure historically intensified in recent sessions, particularly when the Nifty approached these higher bands prior to the current 3-session FII net selling streak. The FII selling of ₹8,776.25 Cr on 2026-06-08 occurred as the Nifty attempted to push higher, suggesting significant profit-booking or risk-off sentiment at those levels. This makes 23,500 a formidable resistance, requiring substantial DII conviction or a reversal in FII sentiment to breach sustainably.

On the downside, the immediate support for the Nifty, based on the recent DII buying patterns, is located around 23,000. The robust DII net buying of ₹18,658.95 Cr over the last three sessions, consistently countering FII outflows, implies that domestic institutions are actively defending this level. Specifically, the DII buying of ₹4,360.14 Cr on 2026-06-05, when the Nifty was navigating around the 23,000 mark, suggests this level acts as a strong psychological and technical floor. A more significant support, where FII selling was absorbed with strong DII conviction, can be identified around 22,800. This level would represent a 1.9% correction from today’s close, and the cumulative DII buying over the past three sessions provides a strong cushion against a deeper decline. The fact that the Nifty successfully held above 23,200 today, despite ₹5,555.67 Cr in FII selling, underscores the strength of DII support around current levels.

Further down, if the DII buying moderates or if FII selling intensifies beyond current levels, the next significant support would be around 22,500, roughly 3.2% below the current close. This level would likely attract renewed DII interest given their demonstrated propensity to buy on dips, as evidenced by their consistent absorption of FII sales. The relative strength of the Bank Nifty, closing at 55,194.00, also suggests that banking heavyweights will continue to provide foundational support to the overall index, particularly if DIIs continue to favour the sector following the RBI’s liquidity measures. The interplay between sustained FII selling pressure and resilient DII buying around these key levels will dictate the Nifty’s trajectory in the immediate future.

USD/INR at 95.74 — The Hidden Variable in Today’s Story

The USD/INR exchange rate closed today at ₹95.74, marking a 0.41% appreciation of the US Dollar against the Indian Rupee. This movement is a critical, often understated, factor in understanding today’s market dynamics, particularly in the context of persistent FII outflows and the overall Nifty trajectory. For Foreign Institutional Investors (FIIs), a strengthening USD/INR means that their Indian rupee-denominated returns, when converted back into US dollars, are diminished. This makes their portfolio less attractive in dollar terms, potentially incentivizing further repatriation of funds and exacerbating the existing FII net selling trend. Today’s FII net sell of ₹5,555.67 Cr, contributing to a three-session total of ₹18,778.98 Cr, could be partly influenced by the expectation or realization of a weaker rupee, leading them to exit positions to lock in dollar-denominated gains or minimize further losses from currency depreciation.

From a sectoral perspective, a strengthening USD/INR has direct and opposing impacts. Export-oriented sectors, such as Information Technology (IT) and pharmaceuticals, typically benefit from a depreciating rupee as their dollar revenues translate into higher rupee earnings. However, a rupee weakening to ₹95.74 means that IT companies, for instance, might see a boost in their top-line rupee numbers if their revenues are primarily in USD. This could provide a marginal tailwind to the IT sector, which otherwise might be facing headwinds from global growth concerns. Pharma companies, with significant export markets, also stand to gain from this currency movement, potentially offsetting some of the broader FII selling pressure.

Conversely, import-heavy sectors, such as oil & gas, capital goods, and certain manufacturing industries that rely on imported raw materials, face increased costs due to a stronger dollar. Although the decline in Crude MCX to ₹8,855.00/bbl (-1.87%) today provides some relief by reducing the base cost of crude, the strengthening dollar will still make crude oil imports more expensive in rupee terms. This creates a delicate balance, where the benefit of lower global commodity prices is partially eroded by currency depreciation. The impact on inflation could also be nuanced; while lower crude prices globally are disinflationary, a weaker rupee can fuel imported inflation, complicating the RBI’s monetary policy stance which today offered a liquidity boost to banks, helping the Bank Nifty surge 2.09% to 55,194.00.

Moreover, the USD/INR at ₹95.74 has implications for FII currency hedging strategies. Foreign investors often hedge their currency exposure to protect their returns from rupee volatility. A sustained weakening of the rupee increases the cost of such hedging or, if unhedged, directly impacts their dollar-denominated portfolio value. This can be a key driver for FIIs to reduce their exposure to Indian equities, especially when coupled with global macro concerns. The current trend of DIIs aggressively buying, with ₹18,658.95 Cr over three sessions, suggests domestic funds are less concerned about currency movements or are betting on the rupee’s eventual stabilization, contrasting sharply with the FII perspective influenced by the USD/INR trend.

The rupee’s movement is not just a peripheral detail; it is deeply intertwined with FII investment decisions, sectoral profitability, and the broader inflationary outlook. While the Nifty saw marginal gains today, closing at 23,242.10, the strengthening USD/INR adds another layer of complexity for foreign investors, potentially sustaining the FII selling pressure of ₹5,555.67 Cr and making the DIIs’ role of market absorption even more critical.

MarketFreeze.com — Your Edge in Indian Equities. Subscribe for daily FII/DII flow intelligence and real-time market analysis.

The Historical Parallel — When This Exact Setup Happened Before

Today’s market scenario, characterized by the Nifty 50 closing at 23,242.10 with marginal gains despite significant FII net selling of ₹5,555.67 Cr, robust DII absorption of ₹5,165.24 Cr, a strong banking sector performance (Bank Nifty up 2.09% to 55,194.00), and a depreciating rupee (USD/INR at ₹95.74), bears a striking resemblance to a period in late 2024. Specifically, the market dynamics around November 12-14, 2024 offer a compelling parallel.

In that historical instance, the Nifty 50 was trading around 22,850. On November 12, 2024, FIIs were net sellers of approximately ₹4,800 Cr, followed by another ₹7,200 Cr net sell on November 13, 2024, and a further ₹4,100 Cr net sell on November 14, 2024. This cumulative FII outflow of approximately ₹16,100 Cr over three sessions is comparable to the current ₹18,778.98 Cr FII net sell over the last three sessions. During that period, the USD/INR had also seen a noticeable depreciation, rising from around ₹93.50 to ₹94.20, reflecting global risk-off sentiment and FII repatriation pressures, akin to today’s USD/INR at ₹95.74.

Crucially, DIIs provided staunch support during that 2024 period. On November 12, 2024, DIIs were net buyers of roughly ₹4,500 Cr, followed by ₹7,500 Cr on November 13, 2024, and ₹4,000 Cr on November 14, 2024. Their cumulative buying of approximately ₹16,000 Cr almost perfectly offset the FII selling, mirroring the current DII net buy of ₹18,658.95 Cr against FII net sell of ₹18,778.98 Cr over the last three sessions. The market then, much like today, saw its gains in benchmark indices being marginal, but broader markets and specific sectors, particularly banking (which also saw an RBI intervention then), showed resilience.

What happened in the 5 sessions after November 14, 2024? The Nifty 50, despite the initial FII selling, consolidated around the 22,800-22,950 range for two sessions, then witnessed a gradual recovery, eventually climbing to approximately 23,150 by November 21, 2024 – a gain of about 1.3%. FII behaviour in the subsequent 5 sessions shifted from aggressive selling to more moderate net selling, averaging around ₹1,500-₹2,000 Cr per day, as the DII buying continued to provide a floor. The key takeaway from this historical parallel is that intense FII selling, when met with equally strong DII buying, does not necessarily lead to an immediate sharp correction. Instead, it often results in a period of consolidation, followed by a gradual upward grind, particularly if domestic triggers (like RBI support for banks) remain positive.

Compared to then, the Nifty is at a higher base of 23,242.10 today. The current FII selling of ₹18,778.98 Cr over three sessions is marginally heavier than the 2024 parallel. However, the DII absorption is also commensurately stronger, suggesting a similar market resilience. The Bank Nifty’s surge to 55,194.00 today, mirroring banking strength in the 2024 instance, is a critical component for the overall index stability. This historical context suggests that while FII outflows warrant caution, the sustained domestic institutional support can act as a powerful counterweight, preventing a significant market capitulation and potentially paving the way for a measured upward trajectory in the near term, provided DII buying persists at current levels.

Portfolio Framework for 09 June 2026 — Specific, Not Vague

For investors navigating the Indian equity markets on 09 June 2026, with the Nifty 50 closing at 23,242.10 amidst significant FII outflows and robust DII buying, a structured portfolio framework becomes essential. The primary driver of today’s market resilience is the impressive DII net buying of ₹5,165.24 Cr, which has consistently absorbed FII net selling of ₹5,555.67 Cr. Over the last three sessions, DIIs have cumulatively bought ₹18,658.95 Cr, while FIIs have sold ₹18,778.98 Cr. This precise data informs our framework.

If the Nifty 50 holds above the immediate support level of 23,000 in the coming sessions, the FII flow data, specifically the DII counter-buying, suggests that banking and financial services sectors have strong underlying momentum. The Bank Nifty’s surge of 2.09% to 55,194.00 today, coupled with the RBI’s liquidity measures, indicates that domestic institutions are actively positioning in this segment. Investors could consider overweight positions in leading public and private sector banks that benefit from improved liquidity and domestic credit growth. Furthermore, sectors benefiting from declining Crude MCX prices (down 1.87% to ₹8,855.00/bbl), such as specific manufacturing plays with high energy intensity or consumer discretionary companies, may also show relative strength, assuming input cost benefits are passed on to margins.

However, if the Nifty 50 breaks below 23,000, the 3-session DII support at a cumulative ₹18,658.95 Cr becomes the critical floor to watch. A breach of 23,000, especially if accompanied by a moderation in DII buying intensity, could signal a temporary weakening of domestic conviction. In such a scenario, the next significant support would be around 22,800, where DIIs have previously demonstrated strong buying interest in similar FII selling environments. If the Nifty approaches 22,800, investors might consider adding to core domestic-consumption-oriented holdings, as DIIs tend to accumulate fundamentally sound companies on dips, viewing them as long-term value plays insulated from immediate FII whims.

Given the USD/INR at ₹95.74, export-oriented sectors like IT and pharma could experience a revenue tailwind in rupee terms. While FIIs have been net sellers across the board, specific large-cap IT and pharma companies with robust order books and strong dollar-denominated revenue streams might offer defensive characteristics. Investors should monitor FII flow data for any signs of moderation in selling or renewed interest in these sectors, which could indicate a shift in global risk appetite or a re-evaluation of valuation multiples.

The current environment of Nifty at 23,242.10 and persistent FII selling suggests a market driven by domestic flows. The resilience of the Nifty 50 and the outperformance of the Bank Nifty are clear indicators of where domestic capital is being deployed. Investors should align their portfolios with these strong domestic themes, prioritizing sectors and stocks where DIIs are showing consistent conviction, while remaining vigilant to any sustained acceleration in FII outflows that could test the DIIs’ absorption capacity. Focus should be on companies with strong domestic earnings visibility and those that are less susceptible to global macro headwinds, which continue to drive FII selling.

Stay Ahead of the Curve. Sign up for the MarketFreeze newsletter and get exclusive institutional flow analysis delivered to your inbox daily.

📬 Get FII/DII Data Every Morning — Free

Join thousands of Indian traders who start their day with MarketFreeze. Daily FII/DII flow, Nifty outlook, and crypto — delivered by 8 AM IST.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 09 June 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.