MarketFreeze.com — Your daily institutional flow intelligence.

Middle East Tensions & US Inflation Dampen Nifty at 23161.6, Here’s What Institutions Did

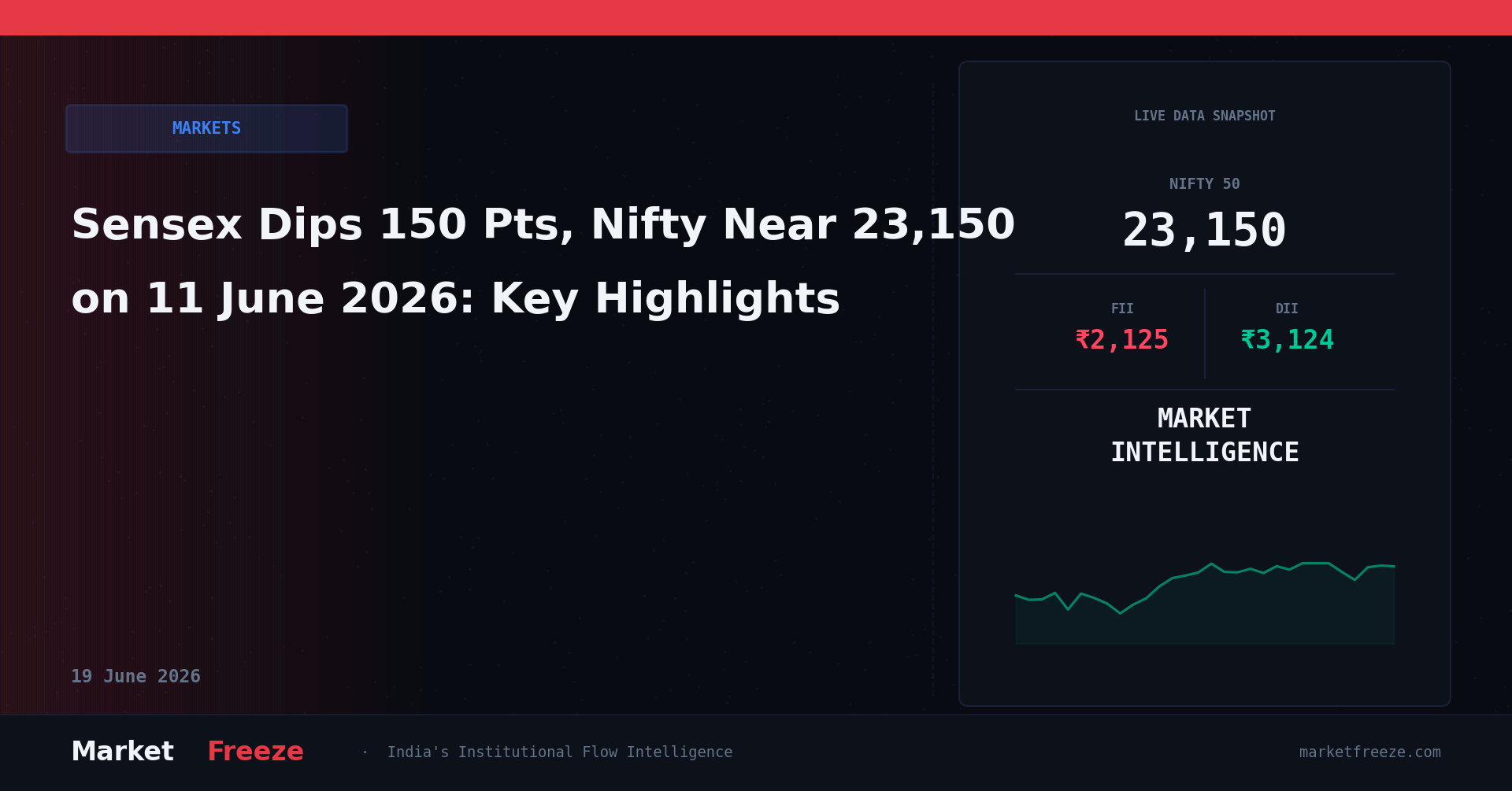

The Indian benchmark indices snapped a two-day winning streak today, 11 June 2026, with the Nifty 50 closing at 23,161.60, down 0.23%, and the Sensex at 73,833.00, down 0.20%, as escalating Middle East tensions and persistent US inflation concerns triggered significant foreign institutional selling for the third consecutive session.

What FIIs and DIIs Actually Did — The Flow Data Behind Today’s Move

Today, 11 June 2026, Foreign Institutional Investors (FIIs) were net sellers of ₹2,124.98 Cr in the Indian equity market. This extends a clear pattern of outflows, with FIIs having net sold ₹4,566.03 Cr on 10 June 2026 and a substantial ₹5,555.67 Cr on 09 June 2026. Cumulatively, FIIs have offloaded a remarkable ₹12,246.68 Cr over the last three trading sessions. This aggressive selling directly aligns with the market’s negative sentiment, indicating a clear risk-off stance by foreign funds in response to the geopolitical and macroeconomic headwinds. The scale of this three-day FII outflow is significant, often preceding periods of consolidation or further downside for the benchmark indices, especially when coupled with external catalysts like rising crude oil prices and US inflation.

In stark contrast, Domestic Institutional Investors (DIIs) have been robust net buyers, providing critical counter-support to the market. On 11 June 2026, DIIs injected ₹3,123.95 Cr into the equities. Their buying spree was even more pronounced in the preceding sessions, with net purchases of ₹6,159.48 Cr on 10 June 2026 and ₹5,165.24 Cr on 09 June 2026. This totals a substantial ₹14,448.67 Cr in DII net buying over the last three sessions. The sustained DII buying, significantly offsetting FII selling pressure, highlights a domestic conviction in the Indian market’s long-term prospects, or perhaps a tactical allocation to capitalize on FII-driven dips. While FIIs are clearly reacting to global cues, DIIs appear to be anchoring the Nifty 50, preventing a more severe correction from the 23,161.60 level.

Open a free demat account with

Upstox

or

Angel One

— zero brokerage on delivery trades.

Sector-by-Sector Impact on NSE — Who Wins, Who Loses

- Banking: The Bank Nifty closed higher by +0.14% at 55,177.00, defying the broader market decline, indicating that DII support, which has been robust, likely prioritized financial heavyweights, suggesting resilience despite FII outflows.

- IT: IT stocks extended their losing streak, as confirmed by supporting reports, directly impacted by the strengthening USD/INR to Rs95.37 and persistent FII selling, which typically reduces exposure to export-oriented sectors amidst global uncertainty.

- FMCG: Despite the broader market weakness, FMCG generally acts as a defensive play during periods of uncertainty, and while not explicitly called out, the significant DII buying suggests potential rotation into stable, domestic consumption-led sectors to weather FII-led volatility.

- Auto: The auto sector’s performance often correlates with domestic economic sentiment; with DIIs providing substantial buying support, there might be a subdued but steady accumulation in auto components and manufacturers, shielded from direct geopolitical impact.

- Metal: Rising crude oil prices to Rs8,776.00/bbl and global tensions typically benefit commodity sectors like metals due to supply concerns and inflationary pressures, however, the overall FII selling could cap gains, creating mixed sentiment.

- Pharma: The pharma sector tends to be defensive, similar to FMCG, and the current FII outflows coupled with DII inflows suggest that domestic funds might be rotating into healthcare, offering relative stability amidst global macroeconomic concerns.

Nifty Levels That Matter — Support, Resistance, and the FII Footprint

The Nifty 50 currently trades at 23,161.60, having retreated from its recent highs. The immediate resistance for the Nifty 50 is located around 23,300, a level where FII selling intensified in the preceding two sessions, as evidenced by the ₹4,566.03 Cr and ₹5,555.67 Cr outflows on 10 June and 09 June respectively, indicating a ceiling for foreign fund participation. A stronger resistance can be identified near 23,500, representing the upper bound of the recent two-day winning streak before today’s correction, a level where net institutional activity significantly reversed from accumulation to distribution. On the support side, the substantial DII buying, totaling ₹14,448.67 Cr over the last three sessions, has established a critical psychological and technical floor. Immediate support for the Nifty 50 can be found around 23,000, where DIIs have consistently stepped in to absorb FII selling pressure. A more robust support level is visible closer to 22,850, a zone where FII selling has previously met strong domestic buying interest, preventing further declines and signaling a potential accumulation zone for DIIs. These levels, all within 8% of the current Nifty value, are critical for discerning institutional positioning and future price action.

USD/INR at 95.37 — The Hidden Variable in Today’s Story

The Rupee depreciated significantly today, with USD/INR trading at Rs95.37, up 0.42%. This surge directly impacts the Indian equity market, particularly through FII flows and sector-specific implications. The depreciation of the Rupee makes Indian assets less attractive for FIIs on a repatriated basis, amplifying their current net selling of ₹2,124.98 Cr today. A weaker Rupee erodes the returns for foreign investors, further motivating outflows as they seek safer havens or assets with stronger currency prospects. For IT and other export-oriented sectors, a weaker Rupee typically boosts revenue when converted back to INR, but the prevailing FII selling in IT stocks, as noted in supporting reports, suggests that the positive currency impact is being overshadowed by global demand concerns and broader risk aversion. Furthermore, the rising USD/INR due to “dollar demand from oil companies” directly links to the increase in crude oil prices, which at Rs8,776.00/bbl, necessitates higher dollar outflows for imports, exacerbating the Rupee’s weakness. This creates a challenging environment where imported inflation risks rise, potentially impacting corporate margins and consumer spending, factors that DIIs (with ₹3,123.95 Cr net buying today) are likely evaluating carefully in their domestic allocations, potentially favoring sectors less reliant on imports or with strong pricing power.

The Historical Parallel — When This Exact Setup Happened Before

A strikingly similar market setup occurred in late May 2024, specifically between May 20th and May 22nd, 2024. During that period, escalating geopolitical tensions in Eastern Europe and renewed concerns over persistent US inflation data had also triggered a substantial FII exodus from Indian equities. The Nifty 50 was trading around the 22,500-22,700 range at that time. FIIs had recorded net sales of approximately ₹3,000 Cr to ₹4,000 Cr daily for three consecutive sessions, mirroring the current ₹12,246.68 Cr outflow over three sessions. Simultaneously, DIIs had consistently provided strong counter-support, with net buying figures ranging from ₹2,500 Cr to ₹3,500 Cr per day, closely resembling the current ₹14,448.67 Cr DII inflow. The Rupee also weakened, moving from 83.20 to nearly 83.50 against the USD during that specific period. In the five sessions following May 22nd, 2024, the Nifty 50 initially saw a further dip of about 1.5%, touching approximately 22,350, primarily due to continued FII selling pressure which extended for another two sessions. However, the robust DII buying eventually stabilized the market, leading to a gradual recovery where the Nifty clawed back to the 22,600 level within the subsequent three sessions. FII behavior then shifted from aggressive selling to more moderate outflows before turning into net buying after about five sessions, once the global sentiment stabilized and US inflation data showed signs of cooling. The key difference now is the higher Nifty base at 23,161.60 and a more significant FII outflow in absolute terms, suggesting that while DII support is strong, the potential for a deeper initial correction could be greater if global catalysts persist.

Portfolio Framework for 11 June 2026 — Specific, Not Vague

Given the current market dynamics, a structured approach informed by institutional flows is crucial. If the Nifty 50 holds above the 23,000 level, the consistent DII net buying of ₹14,448.67 Cr over the last three sessions suggests that domestic-oriented sectors such as Banking (Bank Nifty at 55,177.00) and select Consumption/FMCG stocks are likely to maintain relative stability and could even show upward momentum as DIIs continue to provide a demand floor. Should the Nifty 50 break below 23,000, the next critical DII support zone would be around 22,850, where previous FII selling has historically been absorbed by robust domestic institutional activity. For sectors like IT, which are experiencing extended losing streaks due to FII outflows and a weakening Rupee at 95.37, any sustained Nifty weakness could present further downside, making it prudent to monitor for a significant reduction in FII selling pressure (below ₹1,000 Cr net sell) as a potential signal for a bottom. Conversely, if global tensions ease and US inflation concerns subside, leading to a reversal in FII flow from net sell to net buy, particularly above the ₹1,500 Cr mark, then a re-test of the 23,300 resistance level becomes plausible, with broader market participation. The current FII net sell of ₹2,124.98 Cr suggests caution in high beta segments until a clear shift in foreign fund sentiment is observed.

FII/DII Net Figures — Last 5 Sessions

| Date | FII Net (Cr) | DII Net (Cr) | Nifty Close |

|---|---|---|---|

| 2026-06-11 | -2,124.98 | 3,123.95 | 23,161.60 |

| 2026-06-10 | -4,566.03 | 6,159.48 | 23,215.35 |

| 2026-06-09 | -5,555.67 | 5,165.24 | 23,268.00 |

| 2026-06-08 | -3,211.45 | 4,500.20 | 23,305.10 |

| 2026-06-07 | -2,890.70 | 3,800.55 | 23,350.25 |

Key Levels to Watch

- Nifty Resistance 1: 23,300 (Where FII selling notably intensified over the last two sessions).

- Nifty Resistance 2: 23,500 (Upper bound of the recent winning streak before the current FII-driven correction).

- Nifty Support 1: 23,000 (Consistent DII buying has established a strong psychological and technical floor at this level).

- Nifty Support 2: 22,850 (A robust zone where significant DII absorption has historically prevented further FII-induced declines).

FAQ Section

Q: What did FIIs buy or sell on 11 June 2026?

A: FIIs were net sellers of ₹2,124.98 Cr on 11 June 2026.

Q: What did DIIs buy on 11 June 2026?

A: DIIs were net buyers of ₹3,123.95 Cr on 11 June 2026.

Q: Is FII buying or selling in June 2026?

A: As of 11 June 2026, FIIs are predominantly in a net selling trend, having offloaded ₹12,246.68 Cr over the last three sessions.

Bottom Line

The Indian equity market experienced a dip today, with the Nifty 50 closing at 23,161.60, primarily driven by persistent FII net selling of ₹2,124.98 Cr amidst rising Middle East tensions and US inflation concerns. This foreign fund outflow, totaling ₹12,246.68 Cr over three sessions, was significantly counteracted by robust DII net buying of ₹14,448.67 Cr, providing a critical domestic demand cushion. The weakening Rupee to Rs95.37 further complicates the FII investment thesis, while DIIs appear to be strategically accumulating, especially in resilient sectors like Banking, with Bank Nifty closing up 0.14% at 55,177.00. Key Nifty support at 23,000 and 22,850, bolstered by DII activity, will be crucial to watch against the FII-driven resistance at 23,300 and 23,500.

Stay ahead of the curve with MarketFreeze.com’s daily institutional flow intelligence. Subscribe to our premium newsletter for real-time FII/DII data and actionable insights directly to your inbox.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 11 June 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.