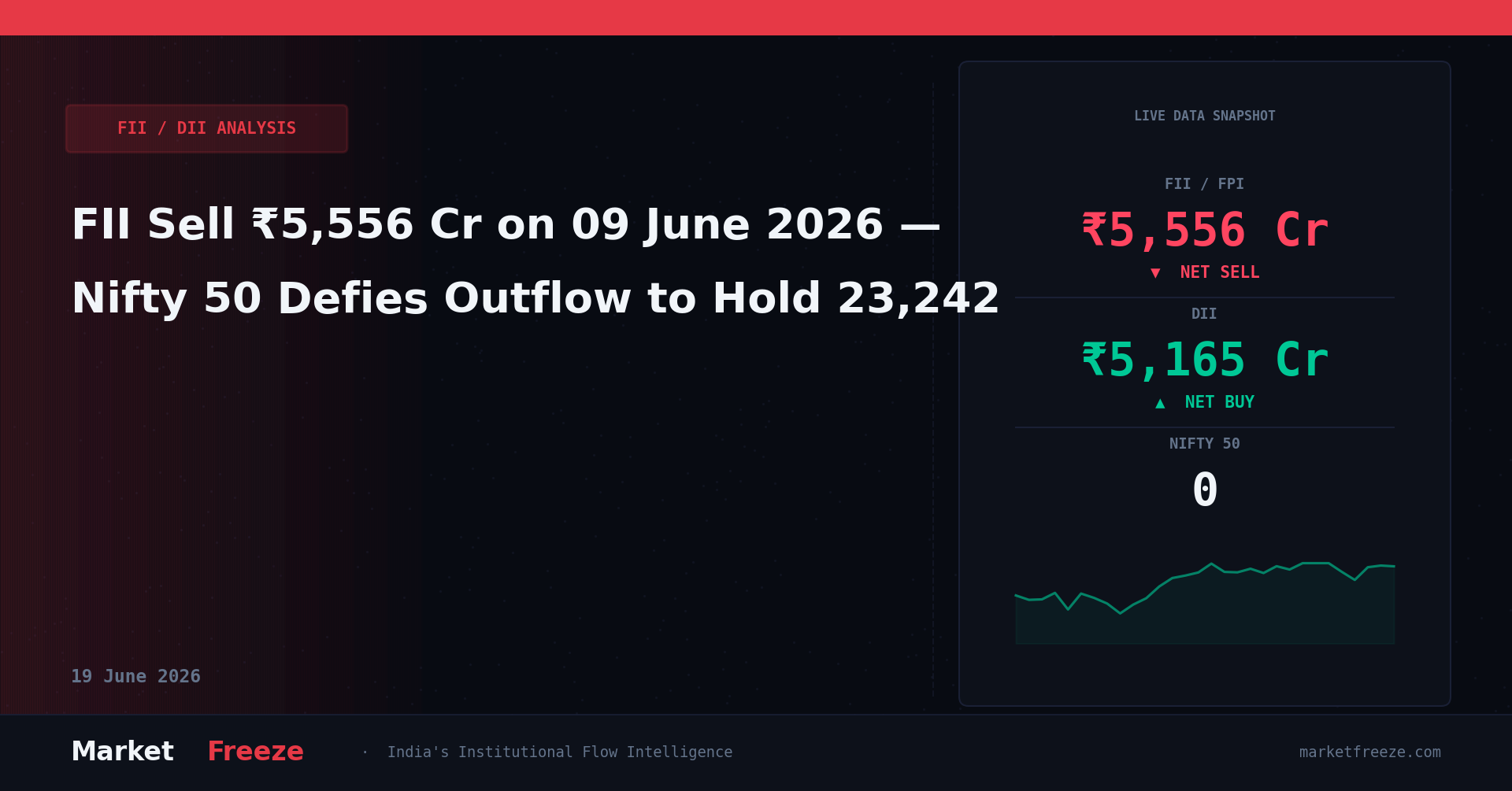

Thursday’s closing bell brought clarity: foreign portfolio allocators executed a net sell-off of ₹5,555.67 Cr on June 9, 2026, marking their third consecutive session of heavy distribution. While headline indices managed to shrug off this relentless pressure, with the Nifty 50 closing up 0.52% at 23,242.10 and the Sensex gaining 0.54% to settle at 73,919.00, the underlying execution mechanics tell a far more nuanced story. This was not a broad-based market recovery; it was a highly targeted liquidity rescue operation funded almost entirely by domestic mutual funds and insurance companies. Domestic institutions absorbed the supply by purchasing a net ₹5,165.24 Cr, preventing a structural breakdown below critical support levels, but leaving the broader market vulnerable to any reduction in domestic cash buffers.

To understand the mechanics of today’s price action, we must dissect the gross volume figures. Foreign portfolio managers were not simply inactive; they actively unloaded inventory. Out of their total transaction volume today, which included ₹8,842.08 Cr on the buy side, their aggressive selling overwhelmed the bids. This follows a massive ₹8,776.25 Cr net divestment on June 8, 2026, and a ₹4,447.06 Cr outflow on June 5, 2026. Over a three-session window, offshore funds have pulled out a cumulative ₹18,778.98 Cr from Indian equities. This persistent liquidation represents a structural reallocation of capital away from emerging markets, driven by a strengthening US Dollar, with the USD/INR currency pair hardening to Rs95.74, a gain of 0.41% today. When the domestic currency depreciates at this pace, foreign funds face immediate dollar-denominated return erosion, forcing automated risk-mitigation selling programs to trigger across large-cap liquid counters.

For retail traders, the immediate takeaway is clear: do not mistake today’s green close for a structural trend reversal. The gap between foreign selling and domestic buying was bridged by retail and high-net-worth proprietary desks, which are holding leveraged overnight positions. If domestic institutions reduce their daily deployment below the ₹5,000 Cr threshold while offshore selling remains above ₹5,500 Cr, a swift intraday correction will follow. The immediate tactical play is to avoid initiating fresh long positions on gap-ups and instead focus on short-term defensive plays in sectors where domestic institutions have established a hard floor.

The RBI Forex Swap Catalyst and the Banking Divergence

The primary driver behind today’s divergent price action, where Bank Nifty surged 2.09% to close at 55,194.00 while the Nifty IT index bucked the positive trend, was the Reserve Bank of India’s surprise regulatory intervention. The central bank detailed a concessional foreign-currency swap facility designed specifically to ease overseas borrowing costs for domestic commercial banks. This operational mechanism allows banks to raise foreign currency funds abroad and swap them with the central bank at highly favorable rates, effectively shielding their net interest margins from the rising cost of domestic deposits. The immediate impact was felt in the banking majors, with State Bank of India emerging as a top gainer, driving the Nifty PSU Bank index up by 3.71%.

This policy intervention directly explains why the Bank Nifty outperformed the Nifty 50 by more than 150 basis points today. Offshore funds, despite their net negative footprint of ₹5,555.67 Cr, were forced to cover their short positions in high-beta banking names to avoid getting squeezed by the domestic institution-led rally. The sudden availability of cheaper foreign-currency funding options alters the liability side of bank balance sheets, particularly for large lenders with active international branches. This regulatory cushion arrives at a critical juncture when credit growth has been outstripping deposit growth, threatening to compress margins across the banking sector in the upcoming quarters.

Your tactical execution strategy here must adjust to this institutional reality. The banking sector has received a temporary liquidity backstop from the central bank, which means downside risk in frontline banking stocks is capped for the June series. Retail traders should look to enter long positions in liquid private and public sector banking stocks on any pullback toward the 20-day exponential moving average, rather than chasing the momentum on days when the USD/INR is trading near Rs95.74.

Crude Oil Deflation and Geopolitical De-escalation

The second major tailwind supporting domestic equities today was the sharp correction in energy prices. Crude MCX settled down 1.66% at Rs8,874.00/bbl, driven by a pause in geopolitical hostilities between Israel and Iran. For a net energy-importing economy like India, a sustained drop in crude prices below the Rs9,000/bbl mark acts as a direct macro stimulus, lowering input costs for paint, specialty chemicals, aviation, and logistics enterprises. This cooling of energy costs explains the strong performance of InterGlobe Aviation (Indigo), which topped the gainer charts alongside banking majors.

However, the divergence between falling crude prices and accelerating capital flight by foreign allocators reveals a deeper structural issue. Historically, falling crude prices have been a strong buy signal for foreign funds operating in India. Today’s counter-intuitive behavior—where crude fell 1.66% but foreign funds still pulled out ₹5,555.67 Cr—indicates that macro asset allocation models are prioritizing global liquidity preservation over localized margin expansion. Offshore funds are responding to the broader currency risk, as evidenced by the USD/INR trading at Rs95.74, rather than the micro-economic benefits of cheaper oil.

The actionable insight for your portfolio is to position in high-conviction margin-expansion stories that benefit from cheaper crude, but only those with low foreign equity ownership. Sectors such as domestic logistics, paints, and select auto ancillaries are prime candidates. Since foreign funds are actively reducing their overall Indian equity exposure, stocks with high foreign ownership will face technical selling pressure regardless of their fundamental improvement, whereas domestic-dominated counters will feel the full benefit of lower raw material costs.

Nifty Structural Levels and Derivatives Positioning

From a purely technical and quantitative perspective, today’s recovery has established well-defined boundaries for the upcoming weekly derivatives expiry. The Nifty 50 closed at 23,242.10, positioned precisely between two massive open interest clusters. On the downside, the 23,000 level represents the absolute line in the sand for domestic institutions. This level is backed by significant put writing and aligns with the heavy buying observed on June 5, when domestic funds deployed ₹4,360.14 Cr to defend the psychological support. Any breach below 23,000 would trigger a cascade of stop-losses, potentially exposing the next major institutional support zone at 22,800.

On the upside, resistance is firmly established at 23,450, followed by a major supply zone at 23,600. This upper boundary is where foreign portfolio managers have consistently concentrated their index futures short positions over the last three sessions. The aggressive selling of ₹8,776.25 Cr on June 8 confirms that offshore desks are actively selling into strength, using any rally toward the 23,500 level to liquidate cash shares and hedge their remaining portfolios with index puts. Therefore, any upward move toward 23,450 will likely encounter severe selling pressure, making a sustained breakout unlikely without a reversal in daily foreign fund flows.

For retail option traders, the strategy must be premium collection rather than directional chasing. With the Nifty 50 trading at 23,242.10, selling out-of-the-money call options above 23,500 and simultaneously selling out-of-the-money put options below 22,900 allows you to capture time decay. This range-bound stance aligns perfectly with the current institutional tug-of-war, where foreign selling is matched rupee-for-rupee by domestic buying, keeping the broader index locked in a well-defined consolidation band.

Sector-Specific Capital Flows: Winners and Laggards

A granular look at the sector-specific price action reveals a clear hierarchy in institutional preference. Banking, particularly public sector banks, was the undisputed recipient of today’s defensive positioning. The 3.71% surge in the Nifty PSU Bank index was driven by heavy block trades and institutional delivery buying. In contrast, the Nifty IT index failed to participate in the recovery, underperforming the broader market as offshore funds reduced their exposure to global outsourcing firms. This weakness in IT is directly tied to the broader macro environment, where high US interest rates and currency volatility are forcing global enterprises to defer discretionary tech spending.

Similarly, the consumer discretionary and quick-commerce space is facing intense scrutiny. The upcoming Zepto IPO, targeting a $1 billion capital raise, has brought these metrics into sharp focus. While Zepto’s revenue more than doubled to ₹22,624 Cr in FY26, its mounting operational losses, rising customer acquisition costs, and ongoing regulatory scrutiny from the Enforcement Directorate have made institutional allocators cautious about the entire high-growth, cash-burning segment. This caution is bleeding into listed quick-commerce and food delivery platforms, where domestic mutual funds are quietly trimming their holdings to allocate capital to cash-generating utilities and lenders.

Your investment allocation must reflect this shift. Avoid allocating capital to pre-profit or highly leveraged growth companies that rely on continuous external funding. Instead, align your capital with the sectors receiving regulatory and domestic institutional support. The banking sector, backed by the RBI’s concessional swap facility, and select capital goods companies remain the safest destinations for capital allocation in this environment.

Gold and Crypto: The Alternative Asset Play

While equities remained locked in an institutional tug-of-war, alternative asset classes showed significant divergence today. Gold MCX traded up 0.52% to settle at a staggering Rs155,487.00/10g. This continuous appreciation in gold prices, even during periods of equity market recovery, indicates that global sovereign entities and central banks are quietly hedging against long-term fiat currency debasement and structural inflation. The parallel rise in the USD/INR to Rs95.74 further amplifies the returns for domestic gold holders, making the precious metal an essential portfolio stabilizer.

In the digital asset space, Bitcoin traded down 0.75% at USD 62,713.00, while Ethereum managed a minor gain of 0.41% to trade at USD 1,672.00. The lack of strong directional momentum in major cryptocurrencies suggests that speculative retail liquidity is drying up globally, as higher-for-longer interest rates make risk-free sovereign debt far more attractive. The contrast between gold’s steady climb and crypto’s consolidation highlights where true institutional defensive capital is flowing during times of currency volatility.

The strategic asset allocation advice here is to maintain a minimum 10% to 15% allocation to physical gold or sovereign gold bonds. When the domestic currency is depreciating toward Rs96 per dollar, holding a hard asset denominated in global terms acts as a vital insurance policy against equity market drawdowns and purchasing power erosion.

Institutional Flow Matrix: Last 3 Sessions

To visualize the ongoing battle between domestic and foreign institutions, we must analyze the net flow matrix over the last three trading sessions. This table illustrates the absolute dominance of these two forces and how they are keeping the market in a state of dynamic equilibrium:

| Trading Date | FII Net Flow (₹ Cr) | DII Net Flow (₹ Cr) | Net Market Impact |

|---|---|---|---|

| 2026-06-09 | -5,555.67 | +5,165.24 | Nifty rises 0.52% on banking support |

| 2026-06-08 | -8,776.25 | +9,133.57 | Index defends key support on high volume |

| 2026-06-05 | -4,447.06 | +4,360.14 | Consolidation near the 50-day moving average |

This data proves that the market is entirely dependent on the continuous inflow of domestic mutual fund SIPs and insurance premium allocations. DIIs have deployed a massive ₹18,658.95 Cr over the last three sessions to absorb the relentless selling from offshore desks. This is a critical structural vulnerability: if domestic inflows slow down even slightly, the market will experience a sharp valuation adjustment to align with foreign selling pressure.

The ultimate tactical takeaway from this institutional matrix is to monitor the daily DII buy figure as your primary risk indicator. If you see DII buying drop below ₹3,000 Cr on a day when foreign funds are selling over ₹5,000 Cr, that is your cue to immediately hedge your long portfolio with index put options or raise cash by liquidating weak momentum holdings.

Retail Allocation and Portfolio Rebalancing Tactics

For the individual investor navigating this institutional tug-of-war, the data points to a mandatory transition from aggressive growth to capital preservation. With foreign portfolio managers executing a cumulative reduction in their Indian equity exposure over the last three sessions, retail traders must stop treating every intraday dip as a broad-market buying opportunity. A key metric to observe is the 1.66% drop in energy derivatives, which historically signals a cooling of domestic inflation. However, because foreign entities are ignoring this macro tailwind due to the 0.41% hardening of the USD/INR currency pair, retail investors who blindly buy high-beta sectors will find themselves trapped in a liquidity vacuum.

The optimal retail strategy is to mirror the domestic institutional play by focusing on large-cap, cash-rich enterprises that exhibit low foreign ownership. If your portfolio is heavily skewed toward high-multiple mid-caps or pre-revenue startups, now is the time to reallocate. Specifically, consider shifting 15% of your speculative growth capital into gold, which continues to show strength with its 0.52% daily gain, or into public sector banking majors that are directly insulated by the central bank’s special regulatory swap facility. Keeping a cash buffer of at least 20% will allow you to capitalize on the localized capitulation sweeps that occur when domestic institutions momentarily pause their daily support operations.

Sector Rotation and the Mid-Cap Valuation Trap

The divergent price action between the 3.71% surge in public sector banks and the underperformance of the IT index highlights a massive sector rotation underway. This rotation is not merely tactical; it is a structural flight toward sectors with tangible cash flows and regulatory protections. The broader market’s vulnerability is particularly acute in the consumer discretionary and quick-commerce spaces, where high-profile listings are forcing a repricing of risk. With private sector players reporting revenues of over ₹22,600 Cr alongside widening operational losses, the market is beginning to realize that growth without profitability is unsustainable in a high-interest-rate global economy.

This structural shift means that defensive sectors like consumer staples, pharmaceuticals, and utilities—which traditionally hold lower foreign institutional equity weightings—are poised to outperform. As foreign allocators continue to exit liquid large-caps, domestic mutual funds will be forced to redirect a portion of their daily inflows to defend these defensive clusters. Retail investors should systematically exit companies trading at price-to-earnings multiples exceeding their five-year historical averages, particularly those in the IT and discretionary sectors, and rotate that capital into value-oriented segments that stand to benefit from cheaper energy imports following the 1.66% decline in crude contracts.

Historical Context of FII Capitulation Cycles

To put the current capital flight into historical perspective, we must examine previous cycles where macro currency pressures triggered automated offshore selling. The current depreciation of the domestic currency by 0.41% in a single session is reminiscent of past emerging market taper tantrums, where a strengthening greenback forced algorithmic model portfolios to systematically trim emerging market weightings. When the USD/INR experiences a rapid move of this scale, the automated risk-mitigation programs used by large pension funds do not look at corporate earnings growth; they execute programmatic, volume-weighted average price (VWAP) sell orders to protect their dollar-denominated returns from eroding further.

Historically, these programmatic liquidation cycles do not resolve in three or four sessions. They typically persist until the domestic currency stabilizes or the central bank actively intervenes in the spot forex market. With the USD/INR holding its ground at elevated levels, the structural pressure on Indian equities will remain a persistent headwind. The fact that domestic institutions managed to absorb almost the entirety of this selling pressure today prevents a catastrophic drop, but history suggests that relying solely on domestic SIP flows to fund a market rally without foreign participation creates a fragile, top-heavy market structure that is highly susceptible to external shocks.

Key Levels and Tactical Roadmap for Tomorrow’s Session

As we head into tomorrow’s trading session, the derivatives setup and institutional flow patterns point to a highly localized playing field. The primary battleground for the index will be the immediate resistance zone just 200 points above today’s close, where foreign desks have heavily concentrated their index futures short positions. On the downside, the immediate support zone lies approximately 240 points below current levels, marking the precise territory where domestic mutual funds launched their aggressive buying counter-offensive during the previous session. A consolidation between these two key technical boundaries remains the most probable scenario for tomorrow.

For active traders, the tactical roadmap is simple: do not buy the index at the open if it gaps up toward the overhead resistance zone, as this is where foreign automated selling programs are programmed to reactivate. Conversely, any sharp intraday drop toward the lower support zone should be viewed as a short-term buying opportunity, provided that domestic institutional buying remains active in the first two hours of trade. If the domestic currency shows signs of recovery and pulls back from its current levels, it could trigger a minor short-covering rally in high-beta banking stocks, which traders can exploit using tight stop-losses just below today’s low.

Strategic Conclusion

The current market dynamic is a classic case of a domestic liquidity cushion colliding with a global macro regime shift. While the domestic-led recovery in the banking sector and the cooling of energy costs by 1.66% offer short-term relief, the structural risk posed by the persistent outflow of foreign capital cannot be ignored. The single most important actionable insight for tomorrow’s session is to restrict all new equity purchases to public sector banks and domestic logistics plays that are direct beneficiaries of the RBI’s swap facility and lower oil prices, while simultaneously purchasing out-of-the-money put options on the index to hedge your existing long portfolio against any sudden reduction in domestic institutional support.

📬 Get FII/DII Data Every Morning — Free

Join thousands of Indian traders who start their day with MarketFreeze. Daily FII/DII flow, Nifty outlook, and crypto — delivered by 8 AM IST.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 09 June 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.