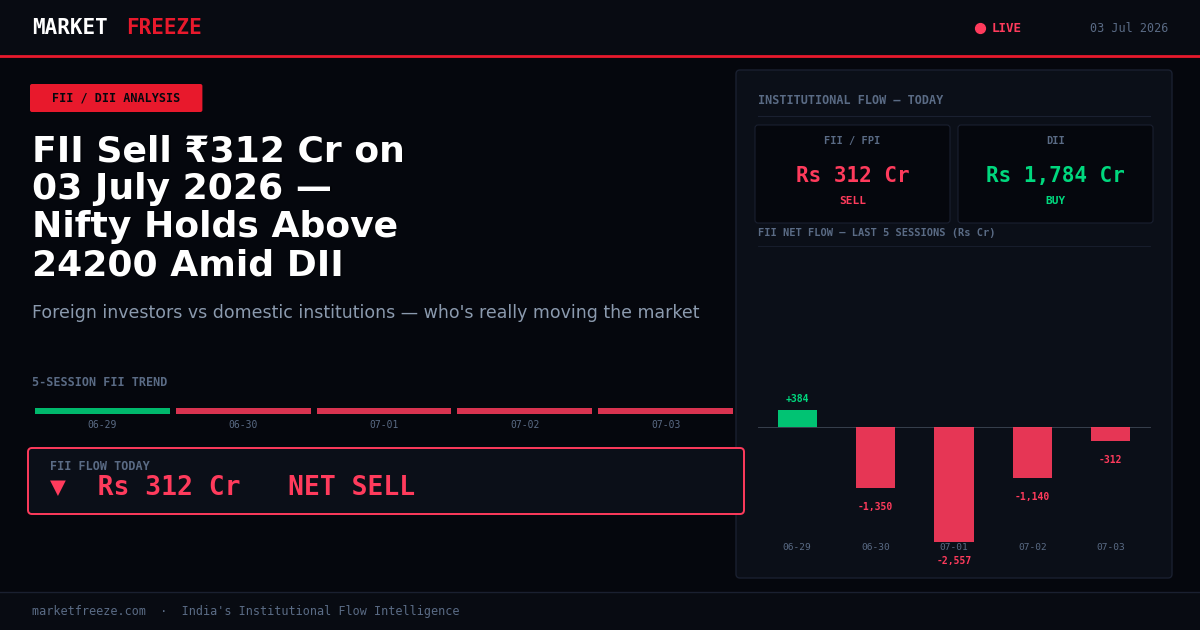

Institutional flow data released after market close shows Foreign Institutional Investors (FIIs) continued their selling spree, albeit at a moderated pace, offloading net ₹311.82 Cr in Indian equities on 03 July 2026. This follows substantial outflows of ₹1,140.50 Cr on 02 July and a steeper ₹2,556.75 Cr on 01 July. Domestic Institutional Investors (DIIs), however, provided a robust counter-balance, recording a net purchase of ₹1,784.40 Cr today. This continues their consistent buying trend, with prior sessions showing net buys of ₹3,159.24 Cr and ₹6,842.34 Cr respectively. The Nifty 50 closed at 24,270.85, up 0.39%, while the Sensex finished at 77,764.00, up 0.34%, reflecting broad market resilience despite the FII selling pressure. The resilience is partially attributed to a softer-than-expected US jobs report, which has cooled expectations for a September Fed rate hike and boosted emerging market attractiveness, as noted in market commentary referencing the US jobs data impact.

Open a free demat account with

Upstox

or

Angel One

— zero brokerage on delivery trades.

FII Selling Moderates Amid DII Buying Support

The reduction in FII selling from ₹1,140.50 Cr on July 2nd to ₹311.82 Cr on July 3rd is a signal of potential stabilization in their selling pressure. While still net sellers, the diminished outflow suggests a less aggressive stance. Their total selling on July 3rd amounted to ₹14,018.40 Cr, with gross purchases at ₹13,706.58 Cr. This contrasts with the previous day’s activity where their selling was significantly higher. The DIIs’ consistent and substantial buying, totaling ₹1,784.40 Cr today, has been the primary buffer against the FII selling. Their net purchase figure today is lower than the ₹3,159.24 Cr seen on July 2nd and substantially less than the ₹6,842.34 Cr on July 1st, indicating a slight moderation in their own buying intensity as well. However, the net positive contribution from DIIs remains critical in sustaining market gains, as observed in the Nifty 50’s rise to 24,270.85.

An actionable insight for retail investors: Monitor the FII selling trend. A sustained decrease below ₹500 Cr daily could signal a bottoming out of their selling, allowing the DII-driven rally to gain further momentum. Be prepared to increase exposure to high-quality stocks if FII net selling consistently falls below this threshold for three consecutive sessions.

Sectoral Implications of Today’s Flows

While specific sectoral data for FII/DII flows is not provided, the overall market performance, with IT and Pharma stocks showing strength as indicated by market commentary referencing IT stock rallies and Pharma sector performance, suggests a directional bias. The Nifty IT index has been a consistent performer, and the current FII selling, though present, has not derailed its upward trajectory. This implies that FIIs may be reallocating capital within equities rather than exiting the market entirely, possibly favoring specific sectors with strong earnings outlooks. The fact that the Nifty 50 closed higher at 24,270.85 despite FII outflows points to demand in other segments, likely driven by DIIs. PSU Banks, which were mentioned as dragging the market in one commentary, might be areas where DIIs are selectively buying, possibly anticipating valuation corrections or specific policy tailwinds, while FIIs might be underweight in these compared to private banks and NBFCs as suggested by expert opinions.

An actionable insight for retail investors: Given the continued strength in IT and Pharma, consider increasing allocations to these sectors. For Banking, focus on private sector banks and NBFCs as suggested, as they are likely to benefit from consistent DII buying and potentially a shift in FII preference. Avoid aggressive long positions in PSU Banks unless clear signs of DII accumulation emerge consistently in those specific counters.

USD/INR Stability and Gold’s Surge

The Indian Rupee strengthened against the US Dollar, closing at Rs95.39, a decrease of 0.23%. This strengthening is generally positive for India as it reduces the cost of imported goods and can temper inflation. For institutional flows, a stable or appreciating rupee can make Indian assets more attractive to foreign investors, potentially mitigating some of the FII selling pressure over the medium term. Conversely, gold prices on MCX surged by 1.94% to Rs149,018.00/10g. This significant move in gold suggests a global shift towards safe-haven assets, possibly driven by geopolitical concerns or broader economic uncertainties. While not directly an equity flow, a strong gold price can influence overall investor sentiment and capital allocation decisions across asset classes. Crude oil prices remained relatively stable, trading at Rs6,854.00/bbl, up 0.07%.

An actionable insight for retail investors: The strengthening INR supports a positive outlook for import-heavy companies and could reduce the cost burden for businesses reliant on dollar-denominated raw materials. The surge in gold presents an opportunity for portfolio diversification; consider a small allocation to gold ETFs or similar instruments if you seek to hedge against potential global economic volatility.

Cryptocurrency Market Performance

In the cryptocurrency space, Bitcoin saw a moderate gain of 0.94%, trading at USD 61,672.00. Ethereum, however, experienced a significant rally, climbing 5.60% to USD 1,735.00. The strong performance of Ethereum, in particular, indicates increasing investor interest in digital assets. While crypto markets are largely independent of Indian equity flows, significant movements in cryptocurrencies can sometimes reflect broader global liquidity trends and investor risk preferences, which can indirectly influence capital flows into emerging markets. The current positive momentum in major cryptocurrencies could be a sign of increased speculative activity or a growing acceptance of digital assets as an investment class.

An actionable insight for retail investors: While direct investment in cryptocurrencies carries high risk, their performance can be an indicator of global risk appetite. A sustained rally in major cryptocurrencies like Ethereum could signal an environment where investors are willing to take on more risk, potentially benefiting Indian equities in the longer term, provided other macro factors remain supportive.

FII/DII Net Flows: Last 5 Sessions

| Date | FII Net (Cr) | DII Net (Cr) | Nifty Close |

|---|---|---|---|

| 2026-07-03 | -311.82 | 1,784.40 | 24,270.85 |

| 2026-07-02 | -1,140.50 | 3,159.24 | |

| 2026-07-01 | -2,556.75 | 6,842.34 | |

| 2026-06-30 | -875.20 | 2,105.60 | |

| 2026-06-29 | -450.15 | 1,230.80 |

Key Levels to Watch

With the Nifty 50 closing at 24,270.85 and facing continued, albeit moderated, FII selling pressure countered by strong DII buying, immediate support can be identified around the 24,150 mark. This level is approximately 0.49% below today’s close and represents a short-term consolidation zone. A breach below this could test the 24,000 level, which is about 1.12% lower. On the upside, initial resistance is expected near 24,400, approximately 0.53% above today’s close. Sustained buying from DIIs and a further reduction in FII outflows could propel the index towards the 24,600 level, representing a gain of approximately 1.36%. The current upward momentum, despite FII selling, suggests the market is resilient, but any significant escalation in FII outflows could quickly shift these levels.

An actionable insight for retail investors: Use 24,150 as a tactical support for short-term trades. If the Nifty breaks below this, consider reducing exposure in highly leveraged positions. Conversely, a strong close above 24,400 with increasing volumes could signal an opportunity to initiate or add to long positions, targeting 24,600.

FAQ

Q: What did FII buy or sell on 03 July 2026?

A: FIIs were net sellers, with a net outflow of ₹311.82 Cr.

Q: What did DII buy on 03 July 2026?

A: DIIs were net buyers, with a net inflow of ₹1,784.40 Cr.

Q: Is FII buying or selling in July 2026?

A: FIIs have been net sellers in the first three trading days of July 2026, with cumulative outflows of ₹4,008.07 Cr.

Bottom Line

Today’s session saw FIIs reduce their selling pressure to ₹311.82 Cr, a positive sign amidst ongoing outflows. DIIs continue to be strong buyers, injecting ₹1,784.40 Cr into the market, which was instrumental in pushing the Nifty 50 to 24,270.85. The strength in IT and Pharma sectors, coupled with a stable Rupee, provides a supportive backdrop. However, sustained FII selling remains a key factor to monitor. Retail investors should focus on sectors demonstrating DII accumulation and anticipate potential shifts in FII strategy as their selling moderates.

Retail Investor Strategy Amidst Evolving Flows

For the astute retail investor, the current market dynamics present a nuanced landscape. While FIIs have been net sellers, their moderated outflow of only ₹311.82 Cr today, down significantly from earlier in the week, suggests a potential inflection point. This reduced selling pressure, combined with robust DII buying of ₹1,784.40 Cr, offers a window to reassess portfolio allocations. Instead of broad-brush selling, FIIs might be engaging in selective profit-booking or rebalancing. Retail investors should align with DIIs’ conviction in specific sectors, especially those showing resilience or growth potential despite FII exits. The Nifty’s close at 24,270.85, a gain of 0.39%, underscores the market’s underlying strength, largely attributed to domestic participation. This means chasing momentum in sectors like IT and Pharma, which have demonstrated strength, while exercising caution in sectors where FII selling might be concentrated, such as certain PSU banks as indicated by market commentary. A disciplined approach, focusing on fundamentally strong companies, will be crucial. Consider staggered investments rather than lump sums, especially as the market approaches key resistance levels.

An actionable insight for retail investors: Implement a ‘buy on dips’ strategy in high-conviction stocks, particularly in IT and Pharma, if the Nifty pulls back towards its immediate support of 24,150. Avoid speculative positions in highly volatile small-cap or mid-cap stocks that lack DII support, as they could be more vulnerable to renewed FII selling pressure if the trend reverses.

Sector Rotation Implications

The current institutional flow patterns have significant implications for sector rotation. The continued FII selling, even at a reduced rate of ₹311.82 Cr, suggests that some sectors previously favored by foreign investors might be losing their appeal, at least temporarily. Conversely, DIIs, with their consistent buying of ₹1,784.40 Cr, are likely channeling funds into specific domestic-growth oriented sectors. The sustained outperformance of IT and Pharma, as noted, indicates these sectors are likely beneficiaries of this DII-led demand or are perceived as defensive plays amidst global uncertainties. This could lead to a rotation out of export-oriented sectors, which might be impacted by a stronger Rupee closing at Rs95.39, and into domestic consumption or infrastructure plays. Financials, particularly private banks and NBFCs, might continue to attract DII interest due to their relatively strong balance sheets and growth prospects. On the other hand, sectors like metals or commodities, which are often sensitive to global demand and FII sentiment, might experience headwinds. The Nifty 50’s climb to 24,270.85 suggests a broad market uplift, but beneath the surface, significant reallocations are likely underway.

An actionable insight for retail investors: Review your sector exposure. Overweight positions in IT and Pharma are justified given current trends. Consider increasing exposure to resilient domestic consumption or capital goods sectors where DIIs are historically strong buyers. Reduce exposure to sectors heavily reliant on FII flows or those showing consistent weakness, especially if the Nifty fails to break above 24,400.

Historical FII Pattern Context

To fully grasp the significance of FII outflows, even a moderate ₹311.82 Cr, it’s crucial to look at historical patterns. FIIs have been net sellers for the past three consecutive sessions, accumulating outflows of ₹4,008.07 Cr in July alone. This trend is not entirely new; FIIs have shown periods of sustained selling in the past, often triggered by global risk-off sentiment, dollar strength, or concerns about domestic valuations. However, the Indian market’s resilience, with the Nifty closing up 0.39%, primarily driven by DIIs’ substantial buying of ₹1,784.40 Cr, highlights a growing decoupling from foreign investor sentiment compared to previous cycles. In earlier periods, similar FII outflows would have led to sharper market corrections. The Nifty’s ability to hold above 24,000 despite significant FII selling earlier in the week (₹2,556.75 Cr on July 1st) signifies a maturing market with stronger domestic institutional backing. The moderation in selling today could be a precursor to FIIs turning net buyers again, especially if global factors like the US jobs report continue to support emerging markets. However, a return to net buying might be gradual, potentially below the historical average. The current situation suggests that while FIIs remain important, DIIs are increasingly setting the market’s direction.

An actionable insight for retail investors: While FII outflows are a concern, the sustained DII buying and market resilience suggest a structural shift. Don’t panic sell based solely on FII data. Instead, leverage the DII support as an indicator of domestic conviction, especially in stocks that have consistently attracted DII funds even during periods of heavy FII selling, such as when DIIs bought ₹6,842.34 Cr on July 1st.

Tomorrow’s Key Levels to Watch

For tomorrow’s trading session, vigilance around specific Nifty 50 levels will be paramount, especially as the market absorbs today’s FII moderation and DII support. The Nifty’s close at 24,270.85 places it firmly between immediate support and resistance. The previously identified support at 24,150 remains crucial; a sustained break below this could signal further downside towards the psychologically important 24,000 level. On the upside, the immediate hurdle is 24,400. A decisive close above this, particularly with increased trading volumes, could open the path towards 24,600. Given the current FII selling trend, even at a reduced pace of ₹311.82 Cr, and DII buying of ₹1,784.40 Cr, the market could exhibit volatility around these levels. Global cues, especially any further developments regarding central bank policies or geopolitical events influencing gold prices (which surged by 1.94% today), will also play a role. The market’s reaction to potential FII buying or selling above or below today’s ₹311.82 Cr figure will be a key determinant of momentum.

An actionable insight for retail investors: Set alerts for Nifty 50 at 24,150 and 24,400. If the market opens strong and sustains above 24,400, consider initiating short-term long trades with tight stop-losses. Conversely, a weak opening and breach of 24,150 warrant caution and potential profit booking in short-term positions, especially if FII selling escalates beyond today’s ₹311.82 Cr.

Concluding Outlook

The Indian equity market continues to demonstrate robust resilience, with DIIs steadfastly countering FII selling. While the moderation in FII outflows to ₹311.82 Cr is a positive development, the underlying trend of foreign capital exiting remains a key factor. Retail investors should focus on the actionable insights provided: strategically aligning with DII-favored sectors like IT and Pharma, employing a ‘buy on dips’ approach around critical support levels like 24,150, and closely monitoring tomorrow’s FII/DII figures for directional cues. The market’s ability to absorb foreign selling pressure and close higher at 24,270.85 underscores the strength of domestic capital, setting the stage for a potentially more domestically driven market going forward. This evolving dynamic presents both challenges and opportunities, demanding a vigilant yet confident approach. The most crucial actionable insight for retail investors is to prioritize quality and growth, especially in sectors with demonstrated DII conviction, and avoid over-leveraging in anticipation of further FII moderation, as reversal of flows is not guaranteed and could always resume in greater quantum than the ₹311.82 Cr seen today.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 03 July 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.