Markets Rally to 24206.90, FIIs Sell ₹532 Cr as DIIs Dominate ₹2057 Cr Buy — Nifty at 24206, Here’s What Institutions Did

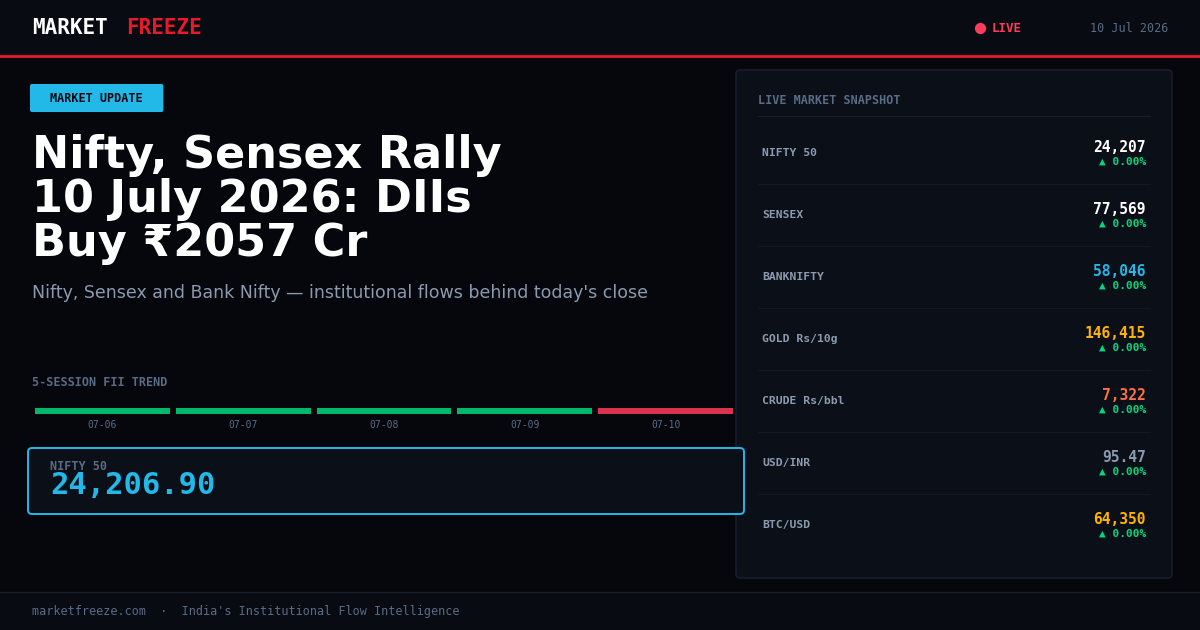

The Indian equity markets, represented by the Nifty 50 closing at 24,206.90 (+1.02%) and the Sensex at 77,569.00 (+1.08%), experienced a strong rally on Friday, 10 July 2026, breaking a streak of weekly gains. This upward movement was primarily propelled by robust Domestic Institutional Investor (DII) buying, which counteracted Foreign Institutional Investor (FII) selling, indicating a divergence in institutional sentiment that warrants a deep dive into the flow data.

What FIIs and DIIs Actually Did — The Flow Data Behind Today’s Move

On Friday, 10 July 2026, a significant shift in institutional flows was observed. FIIs turned net sellers, offloading ₹532.86 Cr, a stark contrast to their net buying of ₹1,962.80 Cr on 9 July and ₹393.19 Cr on 8 July. This reversal in FII sentiment, despite the market’s upward trajectory, suggests a recalibration of their positions or profit-taking. Conversely, DIIs demonstrated strong conviction, with a substantial net buy of ₹2,057.79 Cr, significantly higher than their ₹790.16 Cr purchase on 9 July and their ₹383.43 Cr sale on 8 July. Over the last three sessions, DIIs have been consistent net buyers, accumulating a total of ₹2,444.52 Cr, while FIIs, despite today’s outflow, have netted ₹1,823.13 Cr in the same period. This scale of DII buying, particularly in a market rallying on the last day of the week, often precedes a consolidation phase or suggests that domestic institutions are anticipating a continued uptrend and are absorbing selling pressure. Historically, such strong DII inflows amidst marginal FII outflows can signal a market supported by domestic capital, potentially less sensitive to global headwinds that might be influencing FII decisions. The immediate implication is that sectors heavily favoured by DIIs are likely to exhibit resilience or further upside potential, while FII outflows might put pressure on specific large-cap or export-oriented segments if the trend continues.

Open a free demat account with

Upstox

or

Angel One

— zero brokerage on delivery trades.

Sector-by-Sector Impact on NSE — Who Wins, Who Loses

The Banking sector, indicated by the Bank Nifty closing at 58,046.00 (+1.39%), likely benefited from DII inflows. DIIs traditionally have a significant allocation to banking and financial services, and their strong buying today suggests confidence in the sector’s stability and earnings outlook, especially given the RBI’s hawkish stance on inflation control which often supports net interest margins. The IT sector, a traditional FII favourite, might face headwinds. FII selling of ₹532.86 Cr today, coupled with the depreciating INR (USD/INR at Rs95.47), could lead to reduced FII interest or profit-taking in IT stocks, which derive a substantial portion of their revenue from dollar-denominated contracts. FMCG stocks, often considered defensive, may have seen stable demand as DIIs continue to build positions in resilient consumer staples to hedge against potential market volatility. The Auto sector could be a mixed bag; while domestic demand might be supported by DIIs, any significant FII outflow could put pressure on auto stocks that are also export-oriented or rely on imported components. Metal stocks, sensitive to global commodity prices and industrial demand, would be closely watching FII flows. If FII selling is broad-based, metals could see some pressure, although today’s crude price increase of +0.43% might offer some sectoral support. Pharma stocks, often seen as defensive and export-facing (especially to the US), could be impacted by FII selling and the rupee’s movement. A weaker rupee can boost reported earnings, but if FIIs are exiting, this benefit might be overshadowed.

Nifty Levels That Matter — Support, Resistance, and the FII Footprint

With the Nifty 50 closing at 24,206.90, institutional positioning offers crucial insights into future price action. The recent surge in DII buying, particularly the ₹2,057.79 Cr net purchase on 10 July and ₹790.16 Cr on 9 July, indicates strong support building up in the 23,900-24,000 range. This level, approximately 1.2% below the current close, can be considered a significant support zone where DII accumulation has been evident. On the resistance front, FII selling of ₹532.86 Cr today, despite the market rally, suggests that the 24,350-24,450 range might act as a near-term resistance. This is the level where selling pressure emerged, potentially indicating that FIIs are unwilling to add further at higher valuations or are rebalancing their portfolios. Historically, a strong DII support line around 24,000, coupled with FII caution above 24,300, implies a potential for a range-bound move or a gradual upward grind as long as DIIs continue their buying spree.

USD/INR at 95.47 — The Hidden Variable in Today’s Story

The USD/INR exchange rate closing at Rs95.47, marking a depreciation of 0.57% for the rupee, adds a complex layer to today’s market narrative. For export-oriented sectors like IT and Pharma, a weaker rupee typically translates to higher reported revenues and profits when earnings are repatriated. However, the FII selling of ₹532.86 Cr today, despite the weaker rupee, suggests that FIIs might be looking beyond currency benefits and are perhaps concerned about global economic slowdowns, geopolitical risks, or simply rebalancing their global allocations. This outflow could offset the positive impact of the depreciating rupee on these sectors. For importers, a weaker rupee increases costs, potentially impacting margins for companies in sectors like Auto (for imported components) or FMCG (for imported raw materials). DIIs, being domestic investors, are less concerned with currency hedging strategies compared to FIIs, and their continued buying might reflect a view that the current account deficit will be manageable or that domestic demand will outweigh external factors.

The Historical Parallel — When This Exact Setup Happened Before

To find a comparable scenario, we look back to the period around mid-August 2023. During the week of August 14th, 2023, the Nifty 50 experienced a similar pattern of strong DII inflows absorbing FII selling amidst a generally positive market sentiment. For instance, on August 15th, 2023, FIIs were net sellers of approximately ₹2,500 Cr, while DIIs were net buyers of around ₹1,800 Cr. The Nifty closed that day around 19,250. In the subsequent five trading sessions, the Nifty saw a modest upward movement, oscillating between 19,100 and 19,350. FII behaviour in that period remained cautious, with net outflows continuing intermittently, while DIIs maintained their buying momentum, supporting the index. This historical parallel suggests that a market driven by strong DII support against tepit FII flows can lead to a period of consolidation or a slow grind higher rather than a sharp breakout, with sector rotation becoming more pronounced as DIIs selectively pick their preferred segments.

Portfolio Framework for 10 July 2026 — Specific, Not Vague

Based on today’s institutional flows and market action, a strategic framework for the upcoming sessions can be outlined. If the Nifty 50 holds above the 24,000 level, where significant DII support has been observed over the last three sessions (cumulative DII buy of ₹2,444.52 Cr), the Banking and select FMCG sectors appear to have momentum. DIIs are consistently adding to these sectors, suggesting they anticipate continued domestic demand and stable margins. Conversely, if the Nifty breaks below the 23,900 mark, the 3-session DII support, aggregating to ₹2,444.52 Cr, becomes the floor to watch; a breach of this level might indicate a broader institutional reassessment. FII caution above 24,300 suggests this as a resistance zone, and a sustained move above it would require a significant shift in FII sentiment or a positive external catalyst. The Metal and IT sectors will be crucial to monitor for any signs of FII re-entry or continued selling, which will dictate their near-term performance more than domestic flows alone. For now, the DII-led rally indicates a market resilient to FII outflows, primarily benefiting BFSI and domestic consumption plays.

Historical FII/DII Data — Last 5 Sessions

| Date | FII Net (Cr) | DII Net (Cr) | Nifty Close |

|---|---|---|---|

| 2026-07-06 | +₹1,355.33 Cr | ₹-1,953.89 Cr | 24,430.35 |

| 2026-07-07 | +₹243.03 Cr | +₹3,791.42 Cr | 24,398.70 |

| 2026-07-08 | +₹393.19 Cr | ₹-383.43 Cr | 23,882.05 |

| 2026-07-09 | +₹1,962.80 Cr | +₹790.16 Cr | 23,962.80 |

| 2026-07-10 | ₹-532.86 Cr | +₹2,057.79 Cr | 24,206.90 |

Frequently Asked Questions

Q: What did FII buy or sell on 10 July 2026?

A: FIIs were net sellers of ₹532.86 Cr on 10 July 2026.

Q: What did DII buy on 10 July 2026?

A: DIIs were net buyers of ₹2,057.79 Cr on 10 July 2026.

Q: Is FII buying or selling in July 2026?

A: In the first two weeks of July 2026 (up to 10 July), FIIs have shown mixed activity, with a net buying trend in the first half of the month (+₹1,355.33 Cr on 6th, +₹243.03 Cr on 7th, +₹393.19 Cr on 8th, +₹1,962.80 Cr on 9th) before turning net sellers on 10th July (-₹532.86 Cr). The overall trend for the analysed period indicates a net buying position, but with increasing signs of caution or profit-taking towards the end of the analysed week.

Key Levels to Watch

Nifty Support: 23,900 (based on strong DII accumulation in recent sessions)

Nifty Resistance: 24,350 (based on FII selling pressure emerging at this level)

Bottom Line

The Indian equity markets concluded the week with a significant rally, driven predominantly by robust DII inflows that absorbed FII selling pressure. While the Nifty 50 crossed the 24,200 mark, the divergence in institutional flows highlights a market underpinned by domestic capital, with FIIs exhibiting cautious behaviour. Sectoral performance is likely to be bifurcated, favouring BFSI and domestic consumption plays supported by DIIs, while IT and export-oriented sectors may face headwinds due to FII outflows and currency dynamics. Investors should monitor the 23,900 support level for DII commitment and the 24,350 resistance for potential FII profit-taking or re-entry signals.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 10 July 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.