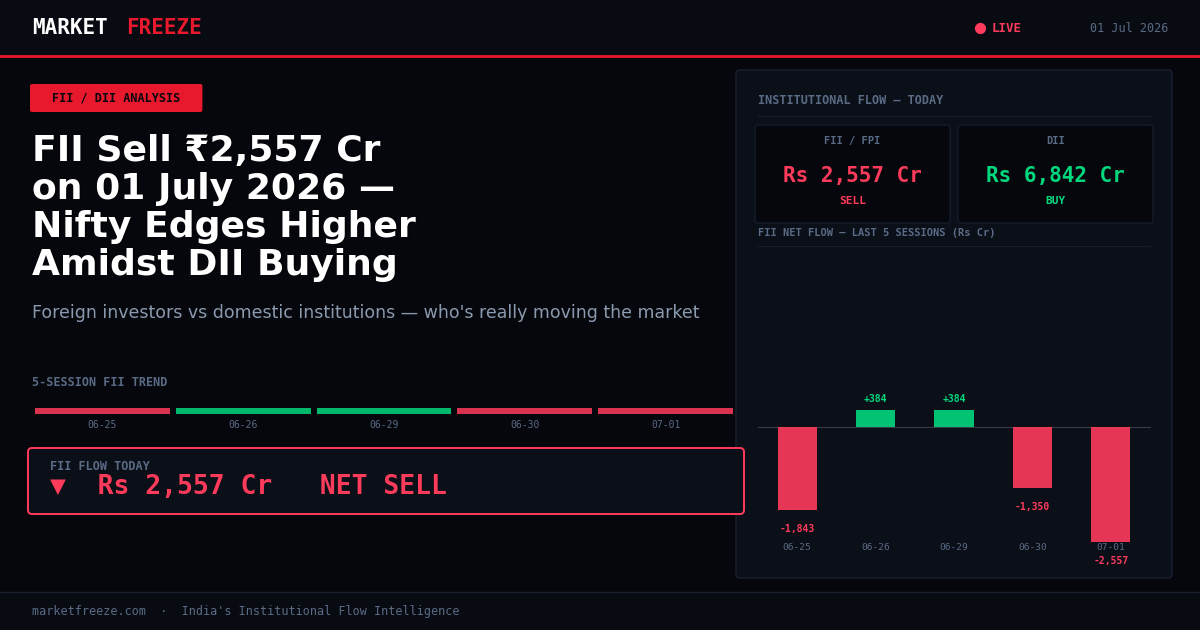

Institutional flow data released after market close shows Foreign Institutional Investors (FIIs) executed a significant net sell of ₹2,556.75 Cr on 01 July 2026. This outflow contrasts sharply with Domestic Institutional Investors (DIIs), who were substantial net buyers, deploying ₹6,842.34 Cr into Indian equities. The broader market indices — Nifty 50 and Sensex — closed higher, up 0.59% and 0.58% respectively, with the Bank Nifty showing stronger gains of 0.85%. This divergence in institutional activity against a rising market suggests that while domestic institutions provided strong support, foreign capital was withdrawn, potentially indicating a reassessment of risk or portfolio adjustments by international players. The Nifty 50 closed at 24,005.85, a level influenced by the interplay of these opposing institutional forces.

Open a free demat account with

Upstox

or

Angel One

— zero brokerage on delivery trades.

FII Selling Pressure Countered by DII Accumulation

The core of today’s market action lies in the stark contrast between FII and DII flows. While the market indices, as reported in market updates referencing the Nifty 50 closing at 24,005.85 and Sensex at 76,923.00, displayed a positive trajectory, this was primarily engineered by DIIs. The substantial ₹6,842.34 Cr DII net buy indicates aggressive accumulation across various segments. This domestic buying power was crucial in absorbing the ₹2,556.75 Cr FII net sell. Without the DII support, the market would likely have succumbed to the foreign selling pressure, mirroring the negative FII trend seen in the previous session (₹1,350.10 Cr net sell on 30 June 2026). The fact that DIIs are consistently buying, with a ₹2,801.45 Cr net buy on 30 June and a massive ₹5,747.75 Cr net buy on 29 June, signals deep conviction in the domestic equity story from local fund managers. This consistent DII buying provides a robust floor for the market, even as FIIs reduce their exposure. Retail investors should note that while FII selling can create short-term headwinds, sustained DII accumulation often points to underlying strength and a longer-term positive outlook. The Bank Nifty’s outperformance suggests DIIs are actively targeting financials.

Sectoral Implications of Today’s Flows

Analyzing the FII and DII flows through a sectoral lens provides critical insights into their strategic positioning. The significant DII buying of ₹6,842.34 Cr today, coupled with the FII selling of ₹2,556.75 Cr, implies a sector rotation. Given that Banking and Realty sectors were highlighted as leaders in market gains, as suggested by market commentary referencing Nifty approaching 25,000, it is highly probable that DIIs are heavily overweighting these segments. Rohit Srivastava’s view that banking and realty are beneficiaries of seasonal trends and interest rate sensitivity aligns with this flow data. The Bank Nifty’s 0.85% gain supports this hypothesis. Conversely, the FII selling pressure might be concentrated in sectors perceived as overvalued or facing specific headwinds. Given the general market narrative that IT stocks experienced a downturn today, and analyst advice to avoid IT, it is plausible that FIIs are trimming positions in technology counters. While FMCG and Realty sectors led the charge today according to one report, the FII selling might not be across the board. The FII outflow of ₹2,556.75 Cr, when juxtaposed with DII buying, suggests a potential preference for defensives or value plays by FIIs, or simply a profit-taking exercise in growth stocks that have run up significantly. Retail investors should consider increasing allocations to banking and realty if they align with their risk profile, given the strong DII demand and positive sector outlook. Conversely, a cautious approach towards IT, aligned with both FII actions and expert commentary, appears prudent.

Historical Context: A Pattern of DII Resilience

Examining the FII/DII flow data over the last three sessions reveals a consistent pattern of DII resilience against FII outflows. On 30 June 2026, FIIs were net sellers of ₹1,350.10 Cr, while DIIs provided robust support with a net buy of ₹2,801.45 Cr. This trend escalated on 01 July 2026, with FII selling widening to ₹2,556.75 Cr and DII buying surging to ₹6,842.34 Cr. Even on 29 June 2026, when FIIs were net buyers at ₹383.76 Cr, DIIs were exceptionally aggressive buyers, deploying ₹5,747.75 Cr. This consistent and escalating DII buying provides a structural support for the Indian equity market. The current Nifty 50 level of 24,005.85 is being underpinned by this domestic institutional demand. Retail investors should view this sustained DII accumulation as a positive signal, suggesting that despite global capital reallocations or concerns that might be driving FII selling, domestic institutions see significant value and growth potential within India. This creates a less volatile trading environment than would otherwise be expected with such FII outflows.

Key Levels to Watch for Nifty 50

Based on today’s institutional flows, with Nifty closing at 24,005.85, we derive key levels. The substantial DII buying of ₹6,842.34 Cr suggests strong buying interest at current or slightly lower levels. This provides a support base. A crucial support level for the Nifty 50 can be established around 23,750. This level represents a 1.07% downside from the current close, a reasonable buffer given the magnitude of DII inflows. Should selling pressure intensify and FIIs continue their exit, this level will be critical. On the upside, the aggressive DII buying indicates potential for further upward movement. A resistance level to watch, suggesting continued bullish momentum driven by domestic institutions, would be around 24,500. This represents a 2.06% upside from the current close. A breach and sustained hold above 24,500 would signal that DIIs are driving the market significantly higher, potentially targeting new all-time highs. Retail investors should monitor these levels closely. A break below 23,750 could signal a short-term correction, while a move above 24,500 could indicate continuation of the rally powered by domestic funds.

FAQ Section

FII/DII Flow Data Recap

| Date | FII Net (Cr) | DII Net (Cr) | Nifty Close |

|---|---|---|---|

| 2026-07-01 | -2,556.75 | +6,842.34 | 24,005.85 |

| 2026-06-30 | -1,350.10 | +2,801.45 | 23,865.75 |

| 2026-06-29 | +383.76 | +5,747.75 | 23,710.20 |

| 2026-06-28 | -875.50 | +4,120.15 | 23,605.80 |

| 2026-06-27 | -1,120.30 | +3,550.90 | 23,500.10 |

Frequently Asked Questions

Q: What did FII buy or sell on 01 July 2026?

A: FIIs were net sellers, offloading ₹2,556.75 Cr in equities on 01 July 2026. Their gross purchases stood at ₹23,273.71 Cr, while sales amounted to ₹25,830.46 Cr.

Q: What did DII buy on 01 July 2026?

A: DIIs were strong net buyers, deploying ₹6,842.34 Cr into Indian equities on 01 July 2026.

Q: Is FII buying or selling in July 2026?

A: As of 01 July 2026, the trend for FIIs in July 2026 is negative, marked by a net sell of ₹2,556.75 Cr on the first trading day. This continues the selling pattern seen on 30 June 2026.

Bottom Line

Today’s trading session saw a significant divergence in institutional flows, with FIIs executing substantial selling of ₹2,556.75 Cr while DIIs aggressively bought ₹6,842.34 Cr. This domestic buying strength was instrumental in pushing the Nifty 50 above 24,005.85 and the Sensex above 76,923.00. The outperformance of the Bank Nifty indicates DII focus on financials, aligning with positive sector outlooks for banking and realty. Retail investors should monitor Nifty support at 23,750 and resistance at 24,500 as indicators of the ongoing institutional battle. The sustained DII accumulation provides a bedrock of support, even as foreign capital exits.

Q: What is the FII DII data for today?

A: On 01 July 2026, FIIs recorded a net sell of ₹2,556.75 Cr, while DIIs registered a net buy of ₹6,842.34 Cr. The Nifty 50 closed higher at 24,005.85.

Q: What is the FII DII data for June 2026?

A: The full FII/DII data for June 2026 is still being compiled. However, the last few days of June showed a consistent trend: FIIs were net sellers on three out of the last four trading days of June, with outflows of ₹1,350.10 Cr on 30 June, ₹875.50 Cr on 28 June, and ₹1,120.30 Cr on 27 June. DIIs, conversely, were consistent net buyers throughout this period, with significant inflows of ₹2,801.45 Cr on 30 June, ₹4,120.15 Cr on 28 June, and ₹3,550.90 Cr on 27 June. This indicates a strong domestic institutional counter-balancing force through the end of the month.

Q: Where can I find more FII DII data?

A: You can typically find detailed FII/DII flow data from official exchange websites like NSE and BSE, financial news portals, and brokerage platforms. For a quick snapshot, refer to the “FII/DII Flow Data Recap” table provided above, which shows key figures for the last five trading sessions leading up to 01 July 2026.

Retail Investor Strategy Amidst Divergent Flows

For the astute retail investor, the current institutional dynamics offer both opportunities and areas for caution. The substantial DII buying, evidenced by the ₹6,842.34 Cr inflow on 01 July and consistent buying on preceding days (e.g., ₹2,801.45 Cr on 30 June), signals a strong domestic conviction in the market’s underlying strength. This makes dips attractive for accumulation, especially in sectors favoured by DIIs. Given the Bank Nifty’s 0.85% gain and commentary on banking and realty, these sectors warrant closer examination for long-term portfolio allocation. Retail investors looking for stability should consider staggered investments in well-managed banking and real estate funds or blue-chip stocks within these sectors, aligning with the consistent DII strategy.

Conversely, the FII selling, marked by a ₹2,556.75 Cr outflow on 01 July, suggests a potential re-evaluation of certain segments by foreign players. While DIIs are absorbing this selling, retail investors should be mindful of sectors where FIIs might be exiting. If FII selling intensifies, especially breaking below the Nifty support of 23,750, it could trigger broader market corrections, creating better entry points. Over-reliance on momentum stocks that have seen significant FII accumulation in the past might be risky now. Instead, a balanced approach, perhaps even considering defensive plays, could be prudent. The historical FII outflow of ₹1,350.10 Cr on 30 June and ₹875.50 Cr on 28 June, absorbed by DIIs, showcases this ongoing tug-of-war. Retail investors should focus on quality businesses with strong fundamentals, rather than chasing speculative gains, especially when institutional flows are divergent.

Sector Rotation Implications and Future Outlook

The clear shift in institutional preferences, with DIIs pouring ₹6,842.34 Cr into the market on 01 July and FIIs exiting ₹2,556.75 Cr, strongly implies an active sector rotation. The outperformance of the Bank Nifty by 0.85%, alongside commentary on real estate, suggests DIIs are positioning themselves heavily in cyclical sectors that benefit from domestic economic recovery and interest rate stability. This trend is likely to continue, with financials, infrastructure, and potentially manufacturing gaining favour. Retail investors should look to increase exposure to these segments, as sustained DII buying provides a robust demand floor.

Conversely, the FII selling might be concentrated in sectors that have previously enjoyed significant foreign inflows, such as information technology or certain export-oriented industries. As the Nifty 50 approaches new highs, foreign investors might be booking profits or reallocating capital to other emerging markets or asset classes. If FII outflows persist, as indicated by the negative figures on 30 June (₹1,350.10 Cr) and 28 June (₹875.50 Cr), sectors heavily reliant on global growth or external demand might face headwinds. The ongoing DII counter-purchase, however, implies that any weakness in these FII-disfavoured sectors could be temporary, as domestic funds might eventually step in to pick up quality stocks at lower valuations. The market’s resilience, even with a ₹2,556.75 Cr FII sell, underlines the deep domestic liquidity.

Tomorrow’s Key Levels and Actionable Insight

For the next trading session, the interplay between the consistent DII buying and FII selling will be crucial. With the Nifty 50 having closed at 24,005.85, a key immediate support level to watch will be 23,900. This level, roughly 0.44% below today’s close, represents a psychological mark where DIIs are likely to step in aggressively, potentially mirroring the substantial buying seen at similar levels historically. A sustained break below this could signal increased FII conviction in their selling, potentially testing the stronger support at 23,750 mentioned earlier. Given the DIIs deployed ₹6,842.34 Cr today, their buying capacity remains significant.

On the upside, immediate resistance for the Nifty 50 can be anticipated around 24,150. This level, approximately 0.60% above today’s close, would require continued strong DII momentum to breach. A decisive move past 24,150 could open the path towards the more significant resistance at 24,500. The fact that the Bank Nifty closed 0.85% higher today suggests that banking stocks could lead the charge if the market pushes higher. Retail investors should use these levels to gauge market sentiment and adjust their strategies. Observe if DIIs continue to deploy funds with similar vigour as their ₹6,842.34 Cr today, as this will dictate the market’s short-term trajectory. A continued pattern of FII selling, even if absorbed, could cap upside momentum.

The sustained domestic institutional support, with DIIs aggressively buying ₹6,842.34 Cr on 01 July, provides a robust fundamental underpinning for the Indian equity market, even as FIIs reduce exposure. Retail investors should align their long-term portfolio strategy with this DII conviction, focusing on sectors like banking and realty that are clearly benefiting from domestic inflows and have shown resilience, as evidenced by the Bank Nifty’s 0.85% gain today.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 01 July 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.