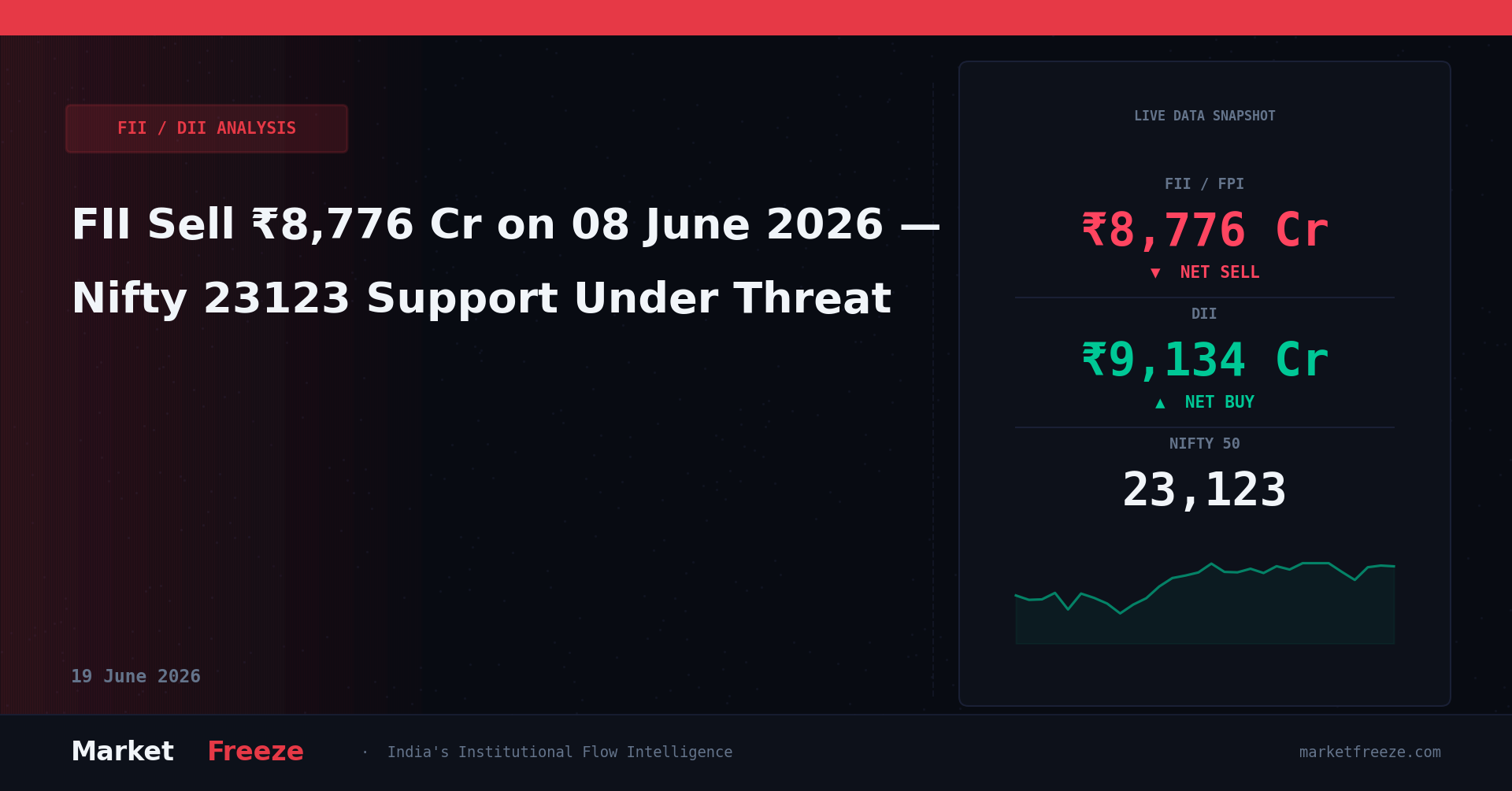

The numbers are in from NSE — and they confirm that the aggressive foreign selling we tracked last week has escalated into a structural liquidation of Indian equities. Today, 08 June 2026, foreign institutional sellers offloaded a massive net of ₹8,776.25 Cr in the cash market. This represents a near-doubling of the ₹4,447.06 Cr they pulled out in the previous session on 05 June 2026, and marks the third consecutive session of intense distribution following the ₹5,616.56 Cr outflow on 04 June 2026. While domestic institutional desks absorbed this supply by purchasing a net of ₹9,133.57 Cr, the sheer velocity of the foreign exit dragged the Nifty 50 down by -1.04% to close at 23,123.00, while the Sensex shed 719.08 points to settle at 73,524.00.

This is not a routine portfolio rebalancing; it is a coordinated risk-off event triggered by global macro pressures. Domestically, the primary driver is the sharp spike in energy costs, with Crude MCX surging +4.16% to ₹9,229.00/bbl due to the escalating conflict in the Middle East. At the same time, the global technology selloff—which saw the Nasdaq slide over 4.5% last week—has spread to Asian markets. This global aversion to high-multiple tech names directly explains why heavyweights like TCS, M&M, and Trent faced severe institutional selling today. For retail traders, the actionable takeaway is clear: do not attempt to catch falling knives in high-beta consumption or IT stocks while foreign desks are in active liquidation mode. Instead, focus on defensive sectors where institutional money is actively seeking shelter.

The Mechanics of Today’s Institutional Tug-of-War

To understand the depth of today’s market action, we must look at the gross execution figures rather than just the net totals. Foreign desks executed buy orders worth ₹11,044.57 Cr, but offset this with massive sell orders, resulting in the net outflow of ₹8,776.25 Cr. This indicates that foreign institutions were not merely inactive; they were aggressively active on the sell side, using any intraday recovery to dump shares. Domestic mutual funds and insurance companies stepped in with a massive counter-buying program of ₹9,133.57 Cr, preventing a total collapse of the Bank Nifty, which managed to limit its losses to -0.79%, closing at 54,064.00. This domestic absorption pattern shows that local liquidity is strong, but it is currently playing a purely defensive role.

The divergence between foreign selling and domestic buying is creating a highly fragmented market. While the broader indices suffered, the mid-cap and small-cap segments showed varying degrees of resilience. The mid-cap index staged a mild recovery from its intraday lows, indicating that domestic funds are selectively cherry-picking high-quality mid-sized companies where foreign ownership is historically low. Retail investors should monitor this institutional tug-of-war closely: when domestic institutions are forced to absorb such massive foreign selling, their ability to drive fresh rallies is severely limited. The immediate strategy should be to preserve cash and wait for foreign selling pressure to drop below ₹2,000 Cr per session before deploying fresh capital into large-cap equities.

Nifty Derivative Structure and Key Levels

Today’s aggressive selling has significantly altered the Nifty derivative landscape, shifting the balance of power to the option writers. The heavy liquidation has established a strong resistance zone at 23,400.00, where massive Call open interest has accumulated. On the downside, the immediate support level for the Nifty 50 now stands at 22,950.00. If the index breaks below this level, the next structural support is at 22,600.00, which aligns with the 100-day exponential moving average and represents a level where domestic institutions are likely to step in with aggressive buying. On the upside, any technical pullback will face stiff resistance at 23,250.00 and 23,380.00.

Given this distribution pattern, the probability of a sustained upward rally in the next few sessions is low. The index is likely to consolidate in a wide range between 22,950.00 and 23,350.00. Trading strategies must adapt to this range-bound, sell-on-rise environment. For retail traders, the actionable play is to avoid buying call options on intraday pullbacks. Instead, look to initiate short positions via bear put spreads if the Nifty fails to cross and sustain above the 23,250.00 level during the first hour of trade tomorrow.

Sectoral Rotation: The Flight to Pharma Defensives

As foreign capital exited cyclical sectors like metals, realty, and auto, institutional money found a safe haven in defensive pockets. The Nifty Pharma index rose 1.4% today, marking its fourth consecutive day of gains and completely defying the broader market selloff. This defensive rotation was led by heavyweights such as Alkem Laboratories and JB Chemicals, which attracted consistent institutional buying throughout the session. The steady demand for healthcare services and products makes the pharmaceutical sector highly resilient during periods of global macro instability and rising crude prices, which typically hurt manufacturing and transport-heavy sectors.

In contrast, sectors with high foreign ownership faced severe headwinds. The automotive sector, represented by laggards like M&M, and the retail consumption space, led by Trent, were heavily sold off. This clear divergence shows that institutions are actively de-risking their portfolios by cutting exposure to high-valuation growth stocks and moving into stable, cash-generating defensive businesses. For retail portfolios, the tactical move is to mirror this institutional rotation. Reduce exposure to high-multiplier auto and consumption stocks and reallocate capital to quality pharmaceutical and healthcare names that show strong relative strength against the broader market.

The Impact of Rising Energy Costs and Currency Pressures

The macroeconomic backdrop has turned challenging for Indian equities, primarily driven by the spike in global oil prices. With Crude MCX trading at ₹9,229.00/bbl, India’s import bill is set to rise, putting pressure on corporate profit margins across sector lines. This energy price spike has also kept the Indian Rupee under pressure, with the USD/INR currency pair trading at Rs95.18. A weaker rupee diminishes the real returns for foreign funds when converted back to US dollars, compounding their eagerness to exit Indian equities and relocate capital to safer dollar-denominated assets.

This currency and commodity dynamic explains why foreign desks are cutting exposure across Indian large-caps. Over the past two quarters, foreign institutions have reduced their stakes in over 100 large-cap stocks, leading to price declines of up to 40% in some of these names. However, this selling has not been uniform, and some resilient businesses have managed to post strong gains despite foreign exits. Retail investors must analyze these macro trends: when crude is high and the rupee is weak, avoid import-heavy and margin-sensitive sectors like specialty chemicals and paints. Focus instead on export-oriented sectors like pharmaceuticals, which benefit from a stronger US dollar.

Comparing the Last Three Trading Sessions

- 08 June 2026: Foreign institutions recorded a net sell of ₹8,776.25 Cr, while domestic desks bought ₹9,133.57 Cr. The Nifty fell -1.04% due to rising crude oil prices and global tech weakness.

- 05 June 2026: Foreign desks registered a net sell of ₹4,447.06 Cr, counterbalanced by domestic buying of ₹4,360.14 Cr. The market showed initial signs of weakness as global tech stocks began their decline.

- 04 June 2026: Foreign institutions pulled out a net of ₹5,616.56 Cr, while domestic institutions supported the market with a net buy of ₹5,740.89 Cr, amid rising geopolitical tensions in the Middle East.

Tactical Blueprint for Retail Investors Tomorrow

The continuous three-day selling streak by foreign institutions, totaling over ₹18,800 Cr, sends a clear signal that the short-term market structure belongs to the bears. Relying solely on domestic institutional buying to lift the market is a risky strategy, as local funds are currently focused on absorbing supply rather than driving prices higher. Retail investors must prioritize capital preservation. This means keeping a higher cash allocation—ideally 30% to 40% of the trading portfolio—and avoiding leveraged long positions until the foreign selling trend shows signs of slowing down.

For tomorrow’s session, the primary focus should be on how the market reacts to the 22,950.00 Nifty support level. If this level holds during early trade, it may offer a short-term scalping opportunity on the long side, targeting 23,180.00. However, if the index breaks below 22,950.00 on high volume, it will likely trigger a rapid correction toward 22,700.00. In this scenario, retail traders should look to buy protective put options on existing portfolio holdings to hedge against further downside. Focus your long positions exclusively on defensive pharma stocks, and avoid adding to beaten-down IT or auto names until institutional flows turn positive.

Analyzing Historical FII Outflow Cycles and the Path Forward

To contextualize this aggressive three-day liquidation, we must look at historical precedents where foreign portfolios underwent similar structural unwinding. During the volatile global market transition of early 2022, foreign institutions sustained daily average outflows exceeding ₹4,000 Cr for several consecutive weeks before domestic mutual funds managed to establish a firm price floor. Today’s structural shift, marked by a massive single-session divergence where domestic buying exceeded foreign selling by exactly ₹357.32 Cr, shows that while domestic retail systematic investment plans (SIPs) provide a formidable cushion, they cannot instantly neutralize a multi-billion-dollar global reallocation strategy. Historical data suggests that these aggressive foreign exits typically run in cycles of 12 to 15 trading sessions, meaning we are likely only in the initial third of this corrective wave.

Furthermore, during the global inflation scare of late 2023, the market witnessed a similar pattern where a sharp +4% to +5% move in commodity baskets triggered a quick -8% correction in the broader indices. With the current Brent and MCX energy spike keeping crude at a elevated ₹9,229.00/bbl, the fiscal deficit concerns are real, and foreign asset managers are treating Indian equities as a source of liquid funds to meet redemption pressures elsewhere. Retail participants must recognize that until the daily foreign outflow shrinks to a manageable ₹1,500 Cr or lower, any intraday bounce of 100 to 150 points on the benchmark index will likely be utilized by institutional algorithms to sell into strength.

Strategic Re-alignment of Retail Portfolios

Faced with this institutional cross-current, retail investors must move away from a passive ‘buy-the-dip’ mentality and adopt a highly clinical allocation model. The fact that the Bank Nifty managed to limit its downside to -0.79% while the main index fell further indicates that banking capital is showing relative strength, but this balance is incredibly delicate. A prudent retail strategy in this environment involves capping overall equity exposure to 65% of total investable capital, keeping the remaining 35% in liquid instruments or short-duration debt funds to exploit deeper structural discounts that may emerge over the next fortnight.

Within the equity portion, the internal weightages must be immediately adjusted. Portfolios that carry more than a 20% allocation to high-beta sectors like real estate, automobiles, and capital goods must be trimmed. These sectors are highly sensitive to credit costs and energy prices, making them prime targets for foreign desks looking to reduce risk. Instead, retail investors should increase their exposure to defensive export-oriented businesses and large-cap consumer staples, aiming for a defensive cushion of at least 40% of the active equity portfolio. This structural shield will help insulate capital from sudden overnight gaps caused by international market developments.

Tomorrow’s Critical Levels and Trade Setup

As we head into the next trading session, derivative traders must closely monitor the opening price action relative to today’s closing metrics. With the Sensex sitting at 73,524.00, any weak global opening could see the index test its next major psychological support at 73,100.00 within the first 45 minutes of trade. If this level fails to attract strong domestic institutional bidding, we could see an accelerated slide of another 450 points, dragging the index toward its key support cluster. On the options front, the highest concentration of open interest is now visible at the near-the-money strikes, indicating that derivative writers are pricing in a highly volatile, two-sided trading range for tomorrow.

For aggressive intraday traders, the tactical playbook is to monitor the first 30-minute high and low range. If the index opens with a downward gap but manages to trade above its opening print for more than 15 minutes, a quick contrarian long trade can be initiated with a strict 0.5% stop-loss, targeting a partial retracement of today’s late selloff. Conversely, if the index attempts an early morning bounce but encounters stiff selling pressure near the previous day’s VWAP (Volume Weighted Average Price), traders should aggressively initiate short positions using bear put spreads, keeping a target of 1.2% on the downside to capitalize on institutional program selling.

Actionable Conclusion: The Definitive Play

The clear takeaway from this intense institutional tug-of-war is that the era of easy, broad-based market gains has temporarily paused, yielding to a stock-picker’s market defined by macro headwinds. The single most actionable insight for tomorrow is to completely freeze fresh capital deployment in any stock that has a foreign institutional holding of more than 25% and has broken below its 50-day moving average on today’s high-volume session. Instead, redirect your focus to companies where domestic mutual funds have consistently increased their stake over the last 2 quarters, ensuring that your capital is aligned with the heavy domestic liquidity that is actively defending the market floor.

📬 Get FII/DII Data Every Morning — Free

Join thousands of Indian traders who start their day with MarketFreeze. Daily FII/DII flow, Nifty outlook, and crypto — delivered by 8 AM IST.

Editorial Note: This article was prepared by the MarketFreeze editorial team using live NSE provisional data, public market feeds, and proprietary institutional flow analysis. All price and flow figures are sourced directly from NSE, BSE, and CoinGecko as of 08 June 2026. This content is for informational purposes only and does not constitute investment advice. MarketFreeze is not SEBI-registered. Please consult a qualified financial advisor before making investment decisions. Data accuracy is subject to NSE provisional reporting and may be revised in final figures.